PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038343

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038343

Electric Vehicle Reducer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

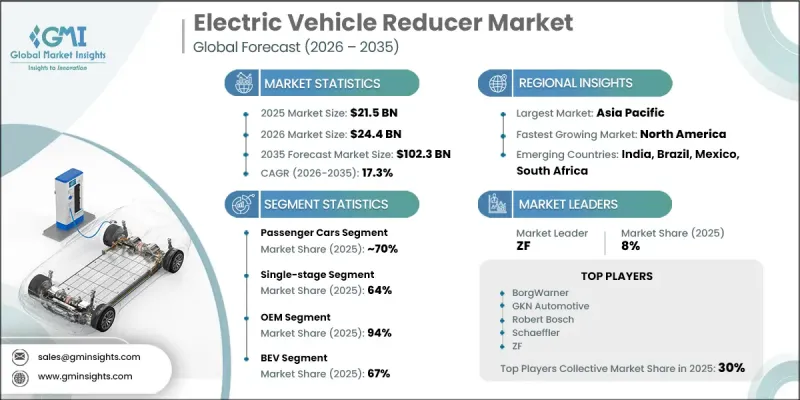

The Global Electric Vehicle Reducer Market was valued at USD 21.5 billion in 2025 and is estimated to grow at a CAGR of 17.3% to reach USD 102.3 billion by 2035.

As electric mobility continues to gain momentum, the need for advanced reducer systems that efficiently convert motor speed into usable torque is becoming increasingly critical. Rising production volumes of electric vehicles are encouraging manufacturers to focus on developing compact, lightweight, and high-performance reducer solutions. Continuous improvements in drivetrain design are further supporting market growth, as companies aim to enhance energy efficiency and optimize vehicle performance. The evolving automotive landscape, supported by advancements in electric powertrain technologies, is creating new opportunities for innovation in reducer systems. Additionally, increased investments in electric vehicle production and infrastructure are reinforcing demand, positioning reducer technologies as a vital component in the transition toward sustainable mobility.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $21.5 Billion |

| Forecast Value | $102.3 Billion |

| CAGR | 17.3% |

The electric vehicle reducer market is further supported by the rapid expansion of electrified transportation across multiple vehicle categories. Growing demand for electric mobility solutions is creating a strong need for robust and efficient reducer systems capable of handling varying operational requirements. Increasing investments in electric vehicle manufacturing and infrastructure development are contributing to higher adoption rates, while efforts to strengthen domestic production capabilities are helping reduce supply chain dependencies and support long-term market growth.

The passenger cars segment accounted for 70% share in 2025 and is expected to grow at a CAGR of over 18% from 2026 to 2035. The rising adoption of electric passenger vehicles is significantly boosting demand for reducer systems that improve performance and energy efficiency. As automakers continue to introduce new electric models, the importance of optimized drivetrain components is becoming more prominent, supporting overall vehicle functionality and driving experience.

The single-stage reducers segment held a 64% share in 2025, and is projected to grow at a CAGR of 17% during 2026-2035. Their simplified design and reduced component complexity make them a cost-effective solution for electric vehicle manufacturers. The focus on affordability and streamlined manufacturing processes is driving their adoption, particularly as the industry works toward making electric vehicles more accessible. Their compatibility with high-speed motor technologies is further contributing to their increasing use.

China Electric Vehicle Reducer Market held a 54% share in 2025, generating USD 5.6 billion. Strong policy support and initiatives promoting electric vehicle adoption have played a key role in expanding both production and demand. Government-driven measures aimed at encouraging domestic manufacturing and accelerating electrification have strengthened the country's position as a major contributor to the global market. The resulting growth in electric vehicle production continues to drive significant demand for reducer systems.

Key companies operating in the Global Electric Vehicle Reducer Market include Magna International, BorgWarner, ZF, Dana, Nidec, Robert Bosch, Valeo, Schaeffler, GKN Automotive, and Vitesco Technologies. Companies in the Global Electric Vehicle Reducer Market are strengthening their competitive position by focusing on innovation, efficiency, and strategic expansion. They are investing in advanced engineering to develop high-performance, compact, and lightweight reducer systems that meet evolving electric vehicle requirements. Many players are forming strategic partnerships with automotive manufacturers to secure long-term supply agreements and expand their market reach. In addition, companies are enhancing manufacturing capabilities and optimizing supply chains to improve production efficiency and reduce costs. Continuous research and development efforts, combined with a focus on scalable and energy-efficient solutions, are enabling companies to remain competitive while addressing the growing demand for electric mobility components.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.2 Sources, by region

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Reducer

- 2.2.4 EV

- 2.2.5 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global EV adoption

- 3.2.1.2 Advancements in e-axle and integrated drivetrain systems

- 3.2.1.3 Demand for high torque density and efficiency

- 3.2.1.4 Growth in high-performance and premium EVs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High precision manufacturing requirements

- 3.2.2.2 Noise, vibration, and harshness (NVH) issues

- 3.2.2.3 Raw material price volatility

- 3.2.2.4 Limited standardization across EV platforms

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of electric commercial vehicles

- 3.2.3.2 Emergence of multi-speed reducers

- 3.2.3.3 Growth in emerging markets

- 3.2.3.4 Lightweight material innovation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Environmental Protection Agency (EPA)

- 3.4.1.2 National Highway Traffic Safety Administration (NHTSA) - FMVSS 500

- 3.4.1.3 Occupational Safety and Health Administration (OSHA)

- 3.4.1.4 Canadian Motor Vehicle Safety Standards (CMVSS)

- 3.4.1.5 State-level road use regulations

- 3.4.2 Europe

- 3.4.2.1 EU Machinery Directive

- 3.4.2.2 CE marking compliance

- 3.4.2.3 Low voltage directive (LVD)

- 3.4.2.4 Electromagnetic compatibility (EMC) directive

- 3.4.2.5 National road homologation requirements

- 3.4.3 Asia Pacific

- 3.4.3.1 Chinese EV & LSV regulatory framework

- 3.4.3.2 Indian Central Motor Vehicle Rules (CMVR)

- 3.4.3.3 Japanese Road Transport Vehicle Act

- 3.4.3.4 ASEAN EV policy harmonization efforts

- 3.4.3.5 Australian Design Rules (ADR)

- 3.4.4 Latin America

- 3.4.4.1 Brazilian National Traffic Council (CONTRAN) regulations

- 3.4.4.2 Mexican NOM standards

- 3.4.4.3 Regional urban mobility & EV incentive programs

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC vehicle compliance & type approval regulations

- 3.4.5.2 South African National Road Traffic Act (NRTA)

- 3.4.5.3 Tourism & free-zone operational standards

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9 Trade data analysis (Driven by Paid Research)

- 3.9.1 Import/export volume & value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis (Driven by Primary Research)

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Impact of AI & generative AI on the market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Capacity & production landscape (Driven by Primary Research)

- 3.14.1 Installed capacity by region & key producer

- 3.14.2 Capacity utilization rates & expansion pipelines

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Sedan

- 5.2.2 SUV

- 5.2.3 Hatchback

- 5.3 Commercial vehicle

- 5.3.1 LCV

- 5.3.2 MCV

- 5.3.3 HCV

- 5.4 Off highway vehicle

- 5.5 Two and three wheeler

Chapter 6 Market Estimates & Forecast, By Reducer, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Single-stage

- 6.3 Multi-stage

Chapter 7 Market Estimates & Forecast, By EV, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 BEV

- 7.3 PHEV

- 7.4 FCEV

- 7.5 HEV

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Southeast Asia

- 9.4.6 ANZ

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Argentina

- 9.5.3 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 BorgWarner

- 10.1.2 Bosch

- 10.1.3 Dana

- 10.1.4 GKN Automotive

- 10.1.5 Nidec

- 10.1.6 Valeo

- 10.1.7 Vitesco Technologies

- 10.1.8 ZF Friedrichshafen

- 10.2 Regional Players

- 10.2.1 HL Mando

- 10.2.2 Hyundai Mobis

- 10.2.3 Hyundai Wia

- 10.2.4 Jatco

- 10.2.5 LG Magna e-Powertrain

- 10.2.6 Punch Powertrain

- 10.2.7 Ricardo

- 10.2.8 TATA AutoComp

- 10.2.9 Zhejiang Wanliyang

- 10.3 Emerging Players

- 10.3.1 SAMHYUN

- 10.3.2 OOKSAN IMT

- 10.3.3 Youngjin Mobility

- 10.3.4 RSB Global