PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740766

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740766

Automotive Wireless Module Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

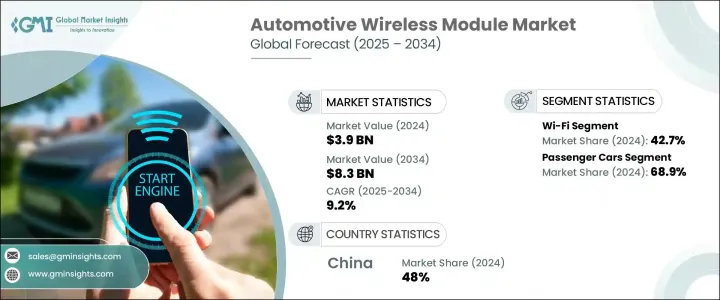

The Global Automotive Wireless Module Market was valued at USD 3.9 billion in 2024 and is estimated to grow at a CAGR of 9.2% to reach USD 8.3 billion by 2034, driven by increasing consumer demand for connected vehicles and the rapid deployment of next-generation wireless technologies like 5G and V2X communication. As the automotive industry experiences a major shift toward digital transformation, wireless modules are becoming essential components in delivering smarter, safer, and more connected driving experiences. From enabling seamless infotainment systems to supporting predictive maintenance and remote diagnostics, these modules are reshaping how vehicles interact with their environment and users.

Automakers are doubling down on wireless connectivity features to enhance convenience, safety, and performance. Today's consumers are not just looking for advanced engines or sleek designs-they expect their vehicles to offer the same level of connectivity as their smartphones. The integration of high-speed wireless technologies is transforming the way drivers and passengers interact with their vehicles, creating new value propositions for automakers. The increasing focus on autonomous driving, electrification, and connected services is fueling the demand for high-bandwidth, low-latency communication systems. Wireless modules are now seen as the backbone of intelligent transportation systems, enabling features like real-time navigation, fleet tracking, remote software updates, and smart city integration.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.9 Billion |

| Forecast Value | $8.3 Billion |

| CAGR | 9.2% |

The shift toward always-connected vehicles is redefining expectations across the automotive landscape. Car buyers today demand more than traditional telematics-they want access to live traffic data, mobile app-based vehicle control, streaming entertainment, and real-time vehicle health updates. These capabilities rely on robust wireless communication modules that ensure uninterrupted interaction between the vehicle, cloud, and other connected infrastructure. The growing rollout of 5G and V2X (vehicle-to-everything) communication is further intensifying the need for advanced wireless solutions. These technologies promise ultra-reliable, low-latency connections between vehicles, infrastructure, pedestrians, and the broader mobility ecosystem. As safety regulations evolve and automation levels rise, the need for consistent, high-speed data transmission will only grow-pushing automakers to prioritize wireless module integration in every model.

Among the many connectivity options available, Wi-Fi continues to lead the automotive wireless module market, commanding a 42.7% share in 2024. This dominance is expected to continue, with strong potential for double-digit growth throughout the forecast period. Wi-Fi remains the go-to technology for data-heavy applications like over-the-air (OTA) updates, video streaming, navigation, and in-vehicle connectivity. Automakers are using Wi-Fi modules to perform real-time diagnostics and deliver software enhancements without requiring physical visits to service centers. In electric and hybrid vehicles, Wi-Fi-enabled systems also help monitor battery usage, optimize performance, and enable seamless communication with charging stations. As the push for smarter, greener vehicles gains momentum, the role of Wi-Fi in managing and analyzing energy systems is becoming increasingly critical.

Passenger vehicles dominate the automotive wireless module market, representing a 68.9% share in 2024. This segment leads the market thanks to the rapid evolution and standardization of connected features across all vehicle classes-from premium sedans to compact hatchbacks. Consumers are now accustomed to having cloud-based infotainment systems, app-based controls, predictive diagnostics, and voice-assisted functions as part of their driving experience. Automakers are embedding wireless modules into vehicle architecture to deliver these features more effectively and boost overall customer satisfaction. As competition intensifies, even entry-level models are being equipped with advanced connectivity solutions, raising the baseline expectations for in-car technology.

The China Automotive Wireless Module Market generated USD 778.6 million in 2024, capturing a 48% share globally. China's dominance stems from its aggressive push toward connected and autonomous mobility, supported by the world's largest automotive manufacturing ecosystem. The country's rising demand for tech-savvy electric vehicles, coupled with generous government incentives and rapid 5G infrastructure rollout, is fueling high adoption of V2X and wireless communication modules. Domestic automakers are leveraging this momentum to integrate smart features and expand their presence in both domestic and international markets. China's continued investment in automotive electronics and its emphasis on digital transformation are expected to further cement its position as a global leader in wireless vehicle connectivity.

Leading companies such as Qualcomm Technologies, Mobileye, VALEO, NVIDIA, Aisin Seiki, Denso, Robert Bosch, Continental, BorgWarner, and ZF Friedrichshafen are accelerating their market presence by focusing on innovation and strategic partnerships. These players are enhancing their wireless platforms to support 5G and V2X applications, integrating AI capabilities, and rolling out scalable, power-efficient modules for EVs and autonomous vehicles. By localizing production and expanding cloud-based service offerings, they aim to stay ahead in a fast-changing market landscape driven by connectivity, automation, and real-time data exchange.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Manufacturers

- 3.2.2 Raw material suppliers

- 3.2.3 Automotive OEM

- 3.2.4 Distribution channel

- 3.2.5 End Use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Pricing analysis

- 3.9.1 Propulsion

- 3.9.2 Region

- 3.10 Impact on forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rising demand for connected vehicles

- 3.10.1.2 Rising adoption of 5G and V2X communication

- 3.10.1.3 Advancements in IoT and smart mobility

- 3.10.1.4 Increased consumer demand for in-car features

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High cost of advanced wireless modules

- 3.10.2.2 Cybersecurity and data privacy concerns

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Connectivity, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Wi-Fi

- 5.3 Bluetooth

- 5.4 Cellular

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedans

- 6.2.2 Hatchback

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light duty

- 6.3.2 Medium duty

- 6.3.3 Heavy duty

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Gasoline

- 7.3 Diesel

- 7.4 Electric

- 7.4.1 PHEV

- 7.4.2 HEV

- 7.4.3 FCEV

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Navigation

- 8.3 Telematics

- 8.4 Infotainment

- 8.5 Vehicle safety and emergency services

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Aisin Seiki

- 11.2 Autotalks

- 11.3 BorgWarner

- 11.4 Continental

- 11.5 Delphi Technologies

- 11.6 Denso

- 11.7 Harman International

- 11.8 Huawei Technologies

- 11.9 Infineon Technologies

- 11.10 Magna International

- 11.11 Mobileye

- 11.12 NVIDIA

- 11.13 NXP Semiconductors

- 11.14 Panasonic

- 11.15 Qualcomm Technologies

- 11.16 Renesas Electronics

- 11.17 Robert Bosch

- 11.18 Skyworks Solutions

- 11.19 VALEO

- 11.20 ZF Friedrichshafen