PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740771

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740771

Camshaft Lifters Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

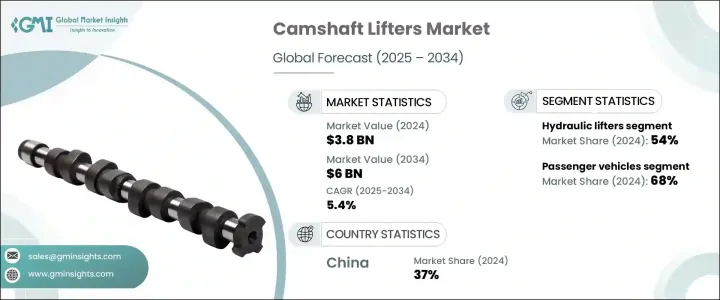

The Global Camshaft Lifters Market was valued at USD 3.8 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 6 billion by 2034. This growth is driven by a rising focus on engine optimization and improving fuel economy, with manufacturers striving to create components that deliver smoother engine operations while adhering to stricter emission regulations. Camshaft lifters play a critical role in enhancing valve timing, reducing internal friction, and improving combustion efficiency, which translates into better fuel economy and reduced emissions. As automakers continue innovating to meet the growing demand for high-performance, eco-friendly vehicles, camshaft lifters are becoming essential in modern internal combustion engine designs. In addition, the growing vehicle production across the globe, particularly in fuel-conscious markets, further accelerates the demand for advanced lifter technologies.

The market is also being shaped by technological advancements in lifter designs, such as roller lifters, hydraulic lifters, and variable valve timing (VVT) systems. These innovations improve engine durability, performance, and compatibility with next-generation engines, extending component life and enabling smoother engine operation. With the rise in high-performance and hybrid vehicles, camshaft lifters are adapting to meet the requirements of both performance enthusiasts and eco-conscious consumers. Furthermore, hybrid vehicles are opening new avenues for lifter integration, ensuring their relevance in evolving powertrain systems. The growing shift toward fuel-efficient and environmentally friendly vehicles continues to push the adoption of camshaft lifters, as they remain a crucial component for enhancing engine efficiency and meeting emission targets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.8 Billion |

| Forecast Value | $6 Billion |

| CAGR | 5.4% |

In 2024, hydraulic lifters dominated the market, holding a 54% share. These lifters are valued for their low maintenance needs, self-adjusting valve clearances, and quiet engine operation. They also contribute to smoother functioning and longer engine life, making them highly attractive to both mainstream and premium vehicle segments. Hydraulic lifters are compatible with a wide range of vehicles, from everyday cars to high-performance models, ensuring their widespread adoption and increasing demand in the automotive market.

Passenger vehicles represented the largest portion of the camshaft lifters market in 2024, accounting for a 68% share. The demand for camshaft lifters in this segment is fueled by the large volume of passenger vehicles produced and sold globally. As consumers seek more fuel-efficient and low-emission cars, automakers are increasingly incorporating camshaft lifters-particularly hydraulic and roller lifters-into their engine designs to enhance performance and fuel economy. Additionally, the aftermarket demand for camshaft lifters remains strong, as vehicles require regular servicing and replacement throughout their life cycle.

China's camshaft lifters market generated USD 618.1 million in 2024, accounting for a 37% share. The country's robust automotive manufacturing sector and the government's push for energy-efficient vehicles have contributed to the rising adoption of camshaft lifters. Despite the long-term challenge posed by the growth of electric vehicles (EVs), which do not require camshaft-based systems, China's dominance in global automotive production and its focus on sustainable vehicle technologies will continue to support camshaft lifter demand in the near term.

Leading industry players include Schrick GmbH, Rane Engine Valve, Shivam Autotech, Comp Cams, Hyundai Kefico, Aisin Seiki, Eaton, Tenneco, Elgin Industries, and BorgWarner. To maintain their competitive edge, these companies are investing heavily in advanced lifter technologies, expanding product compatibility with hybrid and fuel-efficient vehicles, and enhancing production capabilities. They are also forming strategic global partnerships, prioritizing R&D, and collaborating with automakers for early integration of new lifter technologies, ensuring their presence in both OEM and aftermarket segments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component manufacturers

- 3.2.3 Camshaft lifter manufacturers

- 3.2.4 Original Equipment Manufacturers (OEM)

- 3.2.5 Aftermarket distributors and retailers

- 3.3 Profit margin analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures by other countries

- 3.4.2 Impact on the industry

- 3.4.2.1 Price volatility in key materials

- 3.4.2.2 Supply chain restructuring

- 3.4.2.3 Production cost implications

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Price trends

- 3.7 Patent analysis

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rising demand for fuel efficiency and engine performance

- 3.10.1.2 Technological advancements in lifter designs

- 3.10.1.3 Growth in hybrid and electric vehicle segments

- 3.10.1.4 Growing preference for high-performance vehicles

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High production costs

- 3.10.2.2 Technological complexity

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hydraulic lifters

- 5.3 Mechanical (solid) lifters

- 5.4 Roller lifters

- 5.5 Flat tappet lifters

Chapter 6 Market Estimates & Forecast, By Engine, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Petrol (gasoline) engines

- 6.3 Diesel engines

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light Commercial Vehicles (LCV)

- 7.3.2 Medium Commercial Vehicles (MCV)

- 7.3.3 Heavy Commercial Vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM (Original Equipment Manufacturers)

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Aisin Seiki

- 10.2 BorgWarner

- 10.3 Cam Motion

- 10.4 Competition Cams

- 10.5 Crower Cams & Equipment Company

- 10.6 Eaton

- 10.7 Elgin Industries

- 10.8 Hyundai Kefico

- 10.9 Jinan Haiyu Power Machinery Equipment

- 10.10 Johnson Lifters

- 10.11 Lunati Cams

- 10.12 Otics

- 10.13 Rane Engine Valve

- 10.14 Schrick

- 10.15 Sealed Power

- 10.16 Shivam Autotech

- 10.17 SM Motorenteile

- 10.18 Tenneco

- 10.19 TRW Automotive Holdings

- 10.20 Wuxi Xizhou Machinery