PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740775

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740775

Power Module Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

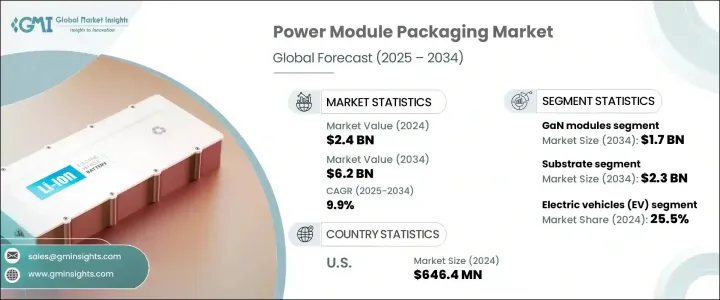

The Global Power Module Packaging Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 9.9% to reach USD 6.2 billion by 2034, driven by the rapid adoption of electric vehicles (EVs) and substantial investments in smart grid infrastructure. As global industries move toward electrification and sustainable energy solutions, the demand for high-performance power module packaging continues to accelerate. The market is benefiting from rising energy consumption across various sectors, including automotive, industrial, and consumer electronics, where efficient energy conversion and robust thermal management are critical.

Technological advancements in semiconductor materials, coupled with the need for compact, reliable, and efficient modules, are reshaping the competitive landscape. Power module packaging is evolving to meet the stringent requirements of emerging applications, from autonomous vehicles to next-generation renewable energy plants. Manufacturers are under growing pressure to deliver innovative designs that support miniaturization without compromising performance, while end users are increasingly seeking solutions that ensure durability, energy savings, and reduced maintenance costs. The market is also seeing heightened focus on sustainability, with players exploring recyclable and environmentally friendly packaging materials to align with global green energy goals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $6.2 Billion |

| CAGR | 9.9% |

As electric vehicles become more mainstream, the need for power module packaging solutions that guarantee efficient energy conversion and effective thermal management in EV powertrains is rising sharply. Moreover, the expansion of the renewable energy sector plays a crucial role in driving market growth. As the shift toward cleaner energy sources like wind, solar, and hydropower intensifies, the demand for efficient power electronics to manage energy conversion, storage, and distribution grows. Power module packaging ensures systems operate reliably and efficiently, especially as large-scale renewable energy installations become more common. High-efficiency power modules are critical for handling variable power inputs from renewables and ensuring stable grid integration. Power modules with advanced packaging significantly enhance power conversion efficiency and minimize energy losses, which is becoming increasingly important as data centers expand to meet the global demand for cloud computing and big data analytics.

The power module packaging market includes GaN modules, SiC modules, FET modules, IGBT modules, and others, with GaN modules expected to lead. By 2034, the GaN module segment is projected to hit USD 1.7 billion, driven by advantages such as high switching frequencies, compact design, and minimal energy losses, making them ideal for fast charging systems, EVs, and data centers. The baseplate segment, accounting for a 24% market share, is gaining traction as demand surges for advanced materials like copper and aluminum silicon carbide (AlSiC), which offer superior heat dissipation and mechanical stability in high-power, high-frequency applications.

The U.S. power module packaging market was valued at USD 646.4 million in 2024, fueled by rapid automotive electrification, renewable energy adoption, and the boom in data centers. However, tariffs on Chinese imports have disrupted supply chains and raised production costs. Key players like Amkor Technology, Fuji Electric, Hitachi, Infineon Technologies, and Kyocera are investing heavily in innovative designs, advanced materials, and strategic collaborations to stay ahead in this dynamic and fast-evolving market.

Key companies in the Global Power Module Packaging Market include Amkor Technology, Fuji Electric, Hitachi, Infineon Technologies, and Kyocera. To strengthen their position in the market, companies are focusing on continuous innovation in materials and designs to meet the growing demand for energy-efficient solutions. They are investing in advanced manufacturing techniques and exploring new materials that improve the thermal management and reliability of power modules. Companies are also enhancing their R&D efforts to create customized packaging solutions that cater to the specific needs of industries like electric vehicles and renewable energy. Strategic collaborations and partnerships with industry leaders allow companies to expand their capabilities and leverage new technologies, ensuring they remain competitive in a rapidly evolving market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.1.3 Impact on the industry

- 3.2.1.3.1 Supply-Side impact (Raw Materials)

- 3.2.1.3.1.1 Price volatility in key materials

- 3.2.1.3.1.2 Supply chain restructuring

- 3.2.1.3.1.3 Production cost implications

- 3.2.1.3.2 Demand-Side impact (Selling Price)

- 3.2.1.3.2.1 Price transmission to end markets

- 3.2.1.3.2.2 market share dynamics

- 3.2.1.3.2.3 Consumer response patterns

- 3.2.1.3.3 Key companies impacted

- 3.2.1.3.4 Strategic industry responses

- 3.2.1.3.4.1 Supply chain reconfiguration

- 3.2.1.3.4.2 Pricing and product strategies

- 3.2.1.3.4.3 Policy engagement

- 3.2.1.3.5 Outlook and future considerations

- 3.2.1.3.1 Supply-Side impact (Raw Materials)

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Growing adoption of electric vehicles (EVs)

- 3.3.1.2 Increasing demand for renewable energy systems

- 3.3.1.3 Rising need for high-efficiency power electronics

- 3.3.1.4 Growth in industrial automation and robotics

- 3.3.1.5 Increasing investments in smart grid infrastructure

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High initial investment and manufacturing costs

- 3.3.2.2 Complex design and thermal management challenges

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 GaN module

- 5.3 SiC module

- 5.4 FET module

- 5.5 IGBT module

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Component, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Substrate

- 6.3 Baseplate

- 6.4 Die attach

- 6.5 Substrate attach

- 6.6 Encapsulations

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Electric vehicles (EV)

- 7.3 Motors

- 7.4 Rail tractions

- 7.5 Wind turbines

- 7.6 Photovoltaic equipment

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 ANZ

- 8.4.7 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of MEA

Chapter 9 Company Profiles

- 9.1 Amkor Technology

- 9.2 Fuji Electric

- 9.3 Hitachi

- 9.4 Infineon Technologies

- 9.5 Kyocera

- 9.6 MacMic Science and Technology

- 9.7 Microchip

- 9.8 Mitsubishi Electric

- 9.9 ON Semiconductor (onsemi)

- 9.10 Renesas Electronics

- 9.11 ROHM Semiconductor

- 9.12 Semikron Danfoss

- 9.13 Starpower Semiconductor

- 9.14 Texas Instruments

- 9.15 Toshiba