PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740791

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740791

Nitrification and Urease Inhibitors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

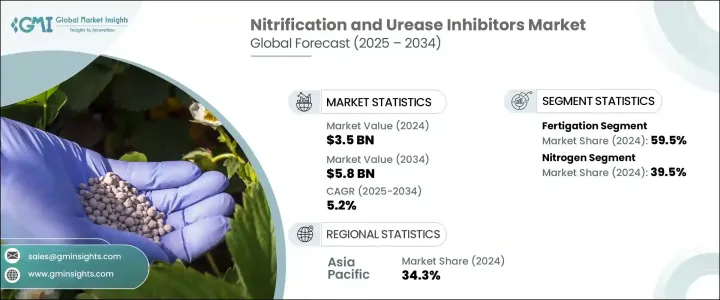

The Global Nitrification and Urease Inhibitors Market was valued at USD 3.5 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 5.8 billion by 2034, driven by the growing urgency to enhance nitrogen use efficiency in agriculture and the increasing shift toward sustainable farming practices. This market is witnessing strong momentum as both environmental and economic pressures compel the agricultural sector to adopt more efficient nutrient management strategies. As the global population rises and arable land becomes scarcer, farmers are looking for innovative tools to optimize input usage without compromising crop yields. Nitrification and urease inhibitors are emerging as critical solutions, offering enhanced fertilizer performance and helping prevent nitrogen loss through leaching and volatilization. These inhibitors are gaining traction not only for their ability to support soil health and water quality but also for their role in improving profitability by reducing waste and boosting yield per acre. Moreover, global concerns over greenhouse gas emissions and water pollution have further propelled demand, making these products essential in modern precision agriculture systems. As the industry continues to invest in smarter, climate-resilient technologies, the market is set to benefit from the convergence of sustainability goals and economic viability, creating opportunities for both agribusinesses and small-scale farmers.

Over the years, farmers have faced significant challenges with nitrogen loss caused by volatilization and leaching, which not only reduce fertilizer efficiency but also harm the environment. In response, the agriculture sector is rapidly adopting inhibitors that improve nutrient retention and reduce harmful emissions. Governments in major agricultural regions like North America and Asia Pacific are actively supporting this shift through subsidies and sustainability initiatives that promote the use of nitrogen stabilizers. These efforts aim to create a more resilient and environmentally responsible agricultural system.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.5 Billion |

| Forecast Value | $5.8 Billion |

| CAGR | 5.2% |

For cost-conscious farmers, the ability to maximize crop yield without inflating input costs makes these inhibitors a highly attractive investment. The growing competition for fertile farmland, coupled with rising concerns about soil degradation and water contamination, has elevated the importance of reliable nitrogen management solutions. In addition to environmental benefits, these products align with evolving agronomic practices such as customized fertilizer blends and advanced delivery methods like foliar sprays and fertigation, encouraging widespread adoption across diverse farming environments.

In 2024, the fertigation segment accounted for a dominant 59.5% share of the market, reflecting its popularity as a preferred application method. This approach integrates fertilizer delivery with irrigation, allowing for precise and consistent nutrient distribution. Fertigation is especially popular in automated farming systems and among growers of high-value crops, where efficiency and consistency are critical. Inhibitors designed for fertigation are becoming increasingly water-soluble, stable, and responsive to varying pH levels and temperatures, making them ideal for precision agriculture applications.

Among the different nutrient types, nitrogen inhibitors captured the largest market share in 2024, holding 39.5% of the total. This strong performance underscores the critical importance of optimizing nitrogen use and curbing nutrient losses to the environment. By keeping nitrogen available in the soil for longer periods, these inhibitors help crops absorb nutrients more efficiently, boosting productivity while reducing negative impacts on water bodies and ecosystems. As a result, nitrogen inhibitors are now a central element in sustainable nutrient management strategies around the world.

The Asia Pacific region led the global market in 2024, securing a 34.3% share, thanks to its high agricultural activity, proactive government policies, and increasing demand for advanced farming practices. Countries across the region are pushing for technologies that minimize nitrogen runoff and improve crop performance, backed by strong policy frameworks and incentives. Meanwhile, markets in North America and Europe continue to demonstrate solid growth, driven by strict environmental regulations and widespread adoption of precision farming technologies.

Leading industry players such as Solvay S.A., BASF SE, Dow, Koch Fertilizers LLC, and DuPont are actively expanding their market reach by developing customized solutions tailored to regional agricultural needs. These companies are forging partnerships with fertilizer manufacturers and agri-tech firms, investing in long-lasting, bio-based technologies, and supporting farmer education programs. Through innovation and collaboration, they are playing a crucial role in shaping the future of sustainable agriculture.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.1.7 Impact on trade

- 3.1.8 Trade volume disruptions

- 3.2 Retaliatory measures

- 3.3 Impact on the industry

- 3.3.1 Supply-Side impact (Raw Materials)

- 3.3.1.1 Price volatility in key materials

- 3.3.1.2 Supply chain restructuring

- 3.3.1.3 Production cost implications

- 3.3.1 Supply-Side impact (Raw Materials)

- 3.4 Demand-Side impact (Selling Price)

- 3.4.1 Price transmission to end markets

- 3.4.2 Market share dynamics

- 3.4.3 Consumer response patterns

- 3.5 Key companies impacted

- 3.6 Strategic industry responses

- 3.6.1 Supply chain reconfiguration

- 3.6.2 Pricing and product strategies

- 3.6.3 Policy engagement

- 3.7 Outlook and Future considerations

- 3.8 Supplier landscape

- 3.9 Profit margin analysis

- 3.10 Key news & initiatives

- 3.11 Regulatory landscape

- 3.12 Impact forces

- 3.12.1 Growth drivers

- 3.12.1.1 Integration of inhibitors with advanced fertilizer technologies

- 3.12.1.2 Rising demand for sustainable and eco-friendly agriculture

- 3.12.1.3 Innovation in bio-based and dual-function formulations

- 3.12.2 Industry pitfalls & challenges

- 3.12.2.1 Limited awareness and adoption among farmers

- 3.12.2.2 High product cost and limited accessibility

- 3.12.1 Growth drivers

- 3.13 Growth potential analysis

- 3.14 Porter's analysis

- 3.15 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Method, 2021 – 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Fertigation

- 5.3 Foliar

Chapter 6 Market Estimates and Forecast, By Nutrient, 2021 – 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Nitrogen

- 6.3 Ammonia

- 6.4 Nitrate

- 6.5 Urea

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Crop Type, 2021 – 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food crop

- 7.3 Cash crop

- 7.4 Horticulture

- 7.5 Fibre crop

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 Dow

- 9.3 DuPont

- 9.4 Solvay S.A

- 9.5 Koch Fertilizers LLC

- 9.6 Evonik

- 9.7 National Fertilizers Limited

- 9.8 Nico Orgo Manures

- 9.9 Compo Expert GmbH

- 9.10 Eco Agro