PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740792

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740792

Wireless Cardiac Monitoring Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

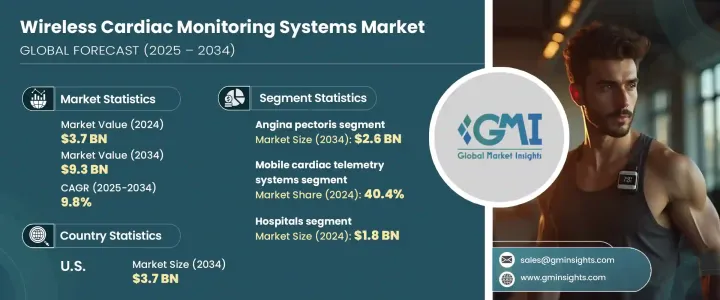

The Global Wireless Cardiac Monitoring Systems Market was valued at USD 3.7 billion in 2024 and is estimated to grow at a CAGR of 9.8% to reach USD 9.3 billion by 2034, driven by the rising demand for real-time, remote cardiac care and the increasing prevalence of cardiovascular diseases worldwide. Wireless cardiac monitoring systems are transforming how healthcare professionals monitor heart health, allowing continuous tracking and wireless data transmission. These systems play a critical role in the early identification of heart-related conditions such as atrial fibrillation, heart failure, and arrhythmias by providing near real-time insights that enable faster and more precise clinical responses. As demand for continuous monitoring rises in aging populations and patients with chronic conditions, the appeal of wireless cardiac monitoring becomes more pronounced.

Technological innovation remains a key catalyst behind this market's momentum. New-generation devices now offer advanced features such as real-time ECG transmission, AI-enabled analytics, and integration with cloud platforms, empowering clinicians to interpret cardiac data more effectively and act promptly. These tools significantly enhance the accuracy of diagnosis and improve patient care outcomes, especially in outpatient or remote settings. The increasing shift toward decentralized care and home-based monitoring further fuels this market expansion, making these systems an essential component of modern cardiac care.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $9.3 Billion |

| CAGR | 9.8% |

In terms of product segmentation, the market is categorized into implantable cardiac monitors (ICMs), mobile cardiac telemetry (MCT) systems, and other wireless cardiac monitoring products. As of 2023, the global market was valued at USD 3.4 billion, with mobile cardiac telemetry systems accounting for 40.4% of the revenue share in 2024. MCT devices enable real-time, continuous monitoring of cardiac rhythms and autonomously transmit alerts using Bluetooth or cellular connectivity. This functionality ensures immediate detection and reporting of abnormal heart activity, offering a proactive approach to diagnosing transient arrhythmias that traditional short-term monitoring may overlook. The consistent growth of this segment is further supported by broader adoption in outpatient settings and an increasing preference for portable, cost-efficient monitoring solutions. These benefits are particularly significant for patients requiring long-term care and for healthcare systems focused on reducing hospital readmissions and in-patient costs.

Wireless cardiac monitoring systems also play a vital role in managing conditions like angina pectoris, which often require ongoing observation to identify ischemic events or irregularities that can precede serious cardiac episodes. Real-time monitoring facilitates better evaluation of symptom patterns and triggers, allowing for more personalized and timely interventions. When symptoms occur unpredictably or present atypically, continuous monitoring provides critical insights that static testing methods might miss, thereby supporting risk management and preventive care strategies.

From an end-use perspective, the market is segmented into hospitals, specialty clinics, diagnostic centers, homecare settings, and others. In 2024, the hospital segment alone reached USD 1.8 billion. Hospitals equipped with advanced cardiology departments and specialized staff are leading adopters of wireless cardiac technologies, using them to improve diagnostic precision and optimize patient care pathways. Investments in technologies that support cloud integration and AI-driven data management have also become increasingly common in these facilities, enabling real-time analysis and faster medical decisions. Additionally, hospitals are actively adopting cutting-edge systems, including wearable ECG sensors and implantable devices, to deliver high-quality care and streamline operations.

The United States wireless cardiac monitoring systems market is projected to surpass USD 3.7 billion by 2034, driven by robust healthcare infrastructure and rising incidence of cardiovascular disease. The country benefits from the rapid adoption of medical innovations and consistent support from both regulatory bodies and investors. Domestic companies and research institutes are also playing a pivotal role in developing next-generation monitoring solutions, further advancing the market. The rise in heart-related health concerns and demand for advanced diagnostic tools are pushing adoption rates higher across clinical and home settings.

This industry remains highly competitive, with key players like Medtronic, Abbott Laboratories, Boston Scientific, iRhythm Technologies, and Koninklijke Philips N.V. collectively accounting for around 40% of the global market share. These companies continue to focus on breakthroughs in remote monitoring, AI-assisted diagnostics, and seamless data transmission technologies to stay ahead in this fast-evolving market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased prevalence of cardiovascular diseases (CVDs)

- 3.2.1.2 Technological advancements in wireless cardiac monitoring technologies

- 3.2.1.3 Rising emphasis on preventive healthcare

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited availability in rural and underdeveloped areas

- 3.2.2.2 Stringent regulatory requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Implantable cardiac monitors (ICM)

- 5.3 Mobile cardiac telemetry systems

- 5.3.1 Lead-based

- 5.3.2 Patch-based

- 5.4 Other products

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Coronary artery disease

- 6.3 Angina pectoris

- 6.4 Atherosclerosis

- 6.5 Heart failure

- 6.6 Stroke

- 6.7 Other indications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Specialty clinics

- 7.4 Diagnostic centers

- 7.5 Home care settings

- 7.6 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 AliveCor

- 9.3 Baxter International

- 9.4 Biotronik

- 9.5 Boston Scientific

- 9.6 InfoBionic

- 9.7 iRhythm Technologies

- 9.8 Koninklijke Philips N.V.

- 9.9 Medtronic

- 9.10 Nihon Kohden

- 9.11 SmartCardia

- 9.12 Vital Connect