PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740830

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740830

Aircraft DC-DC Converter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

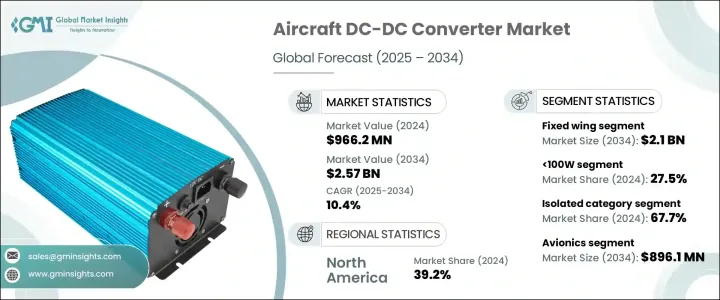

The Global Aircraft DC-DC Converter Market was valued at USD 966.2 million in 2024 and is estimated to grow at a CAGR of 10.4% to reach USD 2.57 billion by 2034. The increasing number of aircraft being produced worldwide is a major factor driving demand for DC-DC converters used in aviation systems. These components are vital for managing voltage levels in increasingly sophisticated aircraft power systems. However, shifts in international trade policies, including tariffs on critical imports such as semiconductors and passive electronic components, have led to rising raw material costs. The uncertainty caused by reciprocal trade restrictions has disrupted global supply chains, creating procurement delays and extending production cycles. Aircraft manufacturers, who rely on consistent integration of electrical components into complex systems, have faced challenges as a result of these trade barriers and delays.

At the same time, modernization efforts in the aviation sector are boosting demand for advanced power management systems. As new-generation aircraft require efficient, stable power delivery for a variety of onboard systems, the role of DC-DC converters becomes increasingly critical. These converters help ensure compatibility between older and newer aircraft electrical infrastructures, supporting the integration of next-gen avionics and electronic systems. Aircraft now require specific voltage levels to support sensitive flight electronics, and DC-DC converters fill the essential role of stabilizing and converting power to meet those needs. As aircraft evolve into more electrically driven platforms, with reduced reliance on pneumatic and hydraulic systems, power conversion technology must also advance to support lighter, more efficient designs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $966.2 Million |

| Forecast Value | $2.57 Billion |

| CAGR | 10.4% |

Based on aircraft type, the market is categorized into fixed wing and rotary wing. The fixed wing segment is anticipated to reach USD 2.1 billion by 2034. The growing transition toward electrically powered systems in fixed wing aircraft is encouraging the adoption of DC-DC converters, which are essential for managing a wide range of voltage requirements. These systems are especially important in newer aircraft models, which increasingly rely on more electric architecture (MEA) to enhance energy efficiency and reduce weight. The rising demand for advanced onboard systems in fixed wing platforms continues to drive the growth of DC-DC converters in this segment.

In terms of output power, the aircraft DC-DC converter market is segmented into 100W, 100W-500W, and above 500W categories. The 100W segment accounted for 27.5% of the market in 2024. This growth is supported by the rising usage of low-power electronics, sensors, and avionics modules within aircraft. These components require stable, low-output voltage, and 100W converters meet this requirement effectively. Additionally, the retrofitting of older aircraft with modern low-power systems further supports the demand for this output category, as it allows for seamless integration with existing power infrastructure.

The market is further divided into isolated and non-isolated converters based on product category. In 2024, isolated converters held the largest share at 67.7%. These are essential in modern aircraft, where electrical isolation is needed to ensure system safety and stability. Isolated converters are designed to handle high-wattage applications, making them ideal for complex electrical operations in newer aircraft designs. They are used extensively in propulsion systems and to provide clean, stable power to onboard electronics, which is crucial for maintaining performance and electrical safety across various aircraft subsystems.

By application, the market includes avionics, power distribution, lighting systems, radar and electronic warfare systems, in-flight entertainment, and others. Among these, the avionics segment is projected to generate USD 896.1 million by 2034. As the complexity and sophistication of avionics systems continue to rise, the need for stable, interference-free power grows in parallel. DC-DC converters help provide reliable voltage for mission-critical electronics such as engine control units, cockpit displays, and flight navigation systems. As aircraft continue to adopt digital avionics technologies, the demand for efficient power management through advanced converters also increases.

Regionally, North America led the market in 2024 with a 39.2% share. This leadership position is attributed to the expansion of commercial aviation and the modernization of aircraft fleets in the region. Airlines and manufacturers are increasingly adopting advanced electronic flight systems, which rely heavily on high-performance DC-DC converters for power stability. Moreover, the growing focus on implementing MEA systems in regional fleets is creating further demand for next-gen power conversion solutions.

The aircraft DC-DC converter market is highly competitive, with major players such as Honeywell International Inc., Murata Manufacturing Co., TDK-Lambda Corporation, Ltd., Advanced Energy, and Vicor Corporation collectively accounting for over 30% of the total market share. These companies are actively investing in the development of compact, energy-efficient, and thermally optimized converter solutions that meet rigorous aviation certification standards. To support evolving aircraft technologies, key manufacturers are also introducing advanced product architectures such as gallium nitride (GaN)-based designs, modular solutions, and resonant topologies. Their innovations aim to address the growing demand from both commercial and defense aviation sectors for power converters that are reliable, scalable, and capable of handling varied voltage and wattage requirements.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw material)

- 3.2.2.1.1 Price volatility

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw material)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising production of aircraft

- 3.3.1.2 Increasing integration of advanced avionics and electronic systems

- 3.3.1.3 Demand for lightweight and high-efficiency power solutions

- 3.3.1.4 Increased focus on fuel efficiency and emission reduction

- 3.3.1.5 Growing focus towards advanced air mobility

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High regulatory and certification barriers

- 3.3.2.2 Design complexity and integration constraints

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Aircraft Type, 2021-2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 Fixed wing

- 5.3 Rotary wing

Chapter 6 Market Estimates & Forecast, By Output Power, 2021-2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 <100W

- 6.3 100W–500W

- 6.4 >500W

Chapter 7 Market Estimates & Forecast, By Category, 2021-2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 Isolated

- 7.3 Non-isolated

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 Avionics

- 8.3 Power distribution

- 8.4 Lighting systems

- 8.5 Radar & electronic warfare systems

- 8.6 In-flight entertainment (IFE)

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Technologies

- 10.2 Advanced Energy

- 10.3 AJ's Power Source Inc.

- 10.4 BrightLoop

- 10.5 Crane Aerospace & Electronics

- 10.6 Helios Power Solutions

- 10.7 Honeywell International Inc.

- 10.8 KGS Electronics

- 10.9 Meggitt PLC.

- 10.10 Murata Manufacturing Co., Ltd.

- 10.11 Pico Electronics

- 10.12 SynQor, Inc.

- 10.13 Tame-Power

- 10.14 TDK-Lambda Corporation

- 10.15 Texas Instruments Incorporated

- 10.16 Vicor Corporation

- 10.17 VPT, Inc.

- 10.18 XP Power