PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740841

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740841

Refrigerated Trailer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

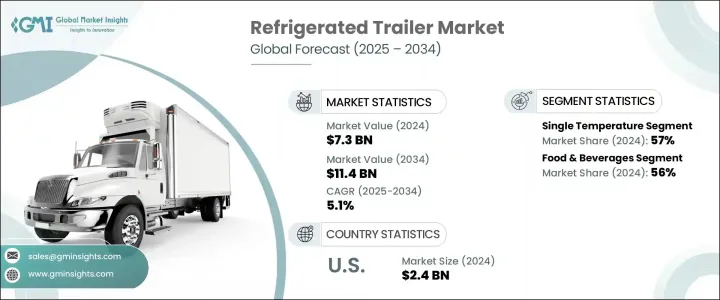

The Global Refrigerated Trailer Market was valued at USD 7.3 billion in 2024 and is estimated to expand at a CAGR of 5.1% to reach USD 11.4 billion by 2034. This growth is largely fueled by the increasing globalization of supply chains and the rising need for efficient transportation of perishable products across long distances. As consumer preferences shift toward fresh, high-quality, and out-of-season items from around the world, the demand for reliable cold chain logistics has surged. This trend is particularly evident in sectors that depend on maintaining specific temperature ranges to preserve the integrity and quality of transported goods. With more international shipments requiring strict temperature control, refrigerated trailers have become a vital component of modern logistics. The evolution of global food and pharmaceutical networks, combined with growing urbanization and lifestyle changes, has further intensified the need for temperature-controlled transportation systems. These trailers play a key role in ensuring that temperature-sensitive goods arrive safely, meeting both consumer expectations and regulatory standards.

In addition to food distribution, the pharmaceutical and healthcare industries are playing an increasingly important role in driving market expansion. Many medical items now require precise temperature conditions to remain effective throughout transit. The growing use of biologics and temperature-sensitive therapeutics has heightened the need for dependable cold chain infrastructure. Refrigerated trailers provide a solution that safeguards product efficacy, supports compliance with strict industry guidelines, and enhances patient safety. As health systems and pharmaceutical companies expand their reach, the demand for advanced temperature-controlled logistics solutions is expected to grow significantly.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.3 Billion |

| Forecast Value | $11.4 Billion |

| CAGR | 5.1% |

By temperature type, the refrigerated trailer market is segmented into single temperature, multi-temperature, and cryogenic categories. In 2024, the single temperature segment accounted for approximately 57% of the global market and is projected to register a CAGR of over 5% through 2034. Single temperature trailers are widely preferred due to their efficiency in transporting uniform product types under consistent thermal conditions. This segment's popularity stems from its straightforward design, ease of operation, and lower operational costs compared to more complex configurations. Fleet managers often favor single-temperature units for long-distance hauls, as they offer higher payload capacity and demand less maintenance. Their simplicity also aligns with numerous global transportation guidelines, which require specific temperature ranges to be maintained without fluctuation.

When analyzed by application, the market is categorized into food and beverages, pharmaceuticals, chemicals, and others. In 2024, the food and beverages segment dominated with a 56% market share and is expected to grow at a CAGR exceeding 5.4% from 2025 to 2034. This segment continues to lead due to the consistent need for cold storage during transport to prevent spoilage of perishable goods. Shifting dietary patterns, the rise in frozen food consumption, and the expansion of grocery delivery services have made refrigerated trailers indispensable in this field. Regulatory compliance surrounding food safety and storage also reinforces the critical role of temperature-controlled logistics. Enhanced demand from international supply chains and evolving retail formats has made efficient cold transport a top priority.

From a materials standpoint, aluminum holds the leading position in the market due to its favorable attributes, such as lightweight construction, strength, and resistance to environmental wear. Aluminum-based trailers are projected to maintain dominance due to their ability to improve fuel efficiency and increase load capacity. In 2024, aluminum was the preferred choice among manufacturers and end-users alike. Its excellent thermal conductivity ensures that internal temperatures remain stable, which is essential for preserving temperature-sensitive goods. Its long service life and low maintenance requirements also contribute to reduced operating costs. Furthermore, its recyclable nature appeals to companies prioritizing environmentally sustainable transport options.

Regionally, the United States led the refrigerated trailer market in North America in 2024, accounting for nearly 86% of the regional share and generating around USD 2.4 billion in revenue. The country's strong position is driven by its extensive logistics networks, large-scale distribution of temperature-sensitive products, and the implementation of strict transportation standards. Advancements in trailer technologies, including energy-efficient systems and smart monitoring features, have made cold chain operations more efficient and reliable. As a result, operators are investing in new fleet technologies and real-time tracking to ensure temperature compliance and reduce spoilage risks.

Key market participants include companies that are investing heavily in sustainable technologies, advanced insulation, and smart telematics to meet environmental targets and operational needs. These companies are also developing electric and hybrid refrigeration units, offering better energy efficiency and lower emissions. Product innovation is a core focus, with firms prioritizing lighter materials, modular designs, and customizable features to serve diverse industry requirements. Strategic collaborations and geographic expansion remain essential tactics for reinforcing their market presence and enhancing customer service capabilities across regions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component manufacturers

- 3.2.3 Trailer manufacturers

- 3.2.4 Dealers and distributors

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures by other countries

- 3.4.2 Impact on the industry

- 3.4.2.1 Price volatility in key materials

- 3.4.2.2 Supply chain restructuring

- 3.4.2.3 Production cost implications

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Price trends

- 3.6.1 Region

- 3.7 Cost breakdown analysis

- 3.8 Patent analysis

- 3.9 Key news & initiatives

- 3.10 Regulatory landscape

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Increasing globalization of food trade and demand for perishable goods

- 3.11.1.2 Rising demand for processed and frozen foods

- 3.11.1.3 Growth in the pharmaceutical and healthcare sectors

- 3.11.1.4 Technological advancements in refrigeration units

- 3.11.1.5 Stringent food safety and regulatory standards

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High initial and operational costs

- 3.11.2.2 Stringent temperature control requirements

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Temperature, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Single temperature

- 5.3 Multi-temperature

- 5.4 Cryogenic

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Food & beverages

- 6.3 Pharmaceuticals

- 6.4 Chemicals

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Aluminum

- 7.3 Steel

- 7.4 Composite

- 7.5 Plastic

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Transportation

- 8.3 Storage

- 8.4 Distribution

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Carrier Transicold

- 10.2 Faymonville

- 10.3 Fruehauf Trailers

- 10.4 Gray & Adams

- 10.5 Great Dane Trailers

- 10.6 Hwasung Thermo

- 10.7 Hyundai Translead

- 10.8 Kidron

- 10.9 Kogel Trailer

- 10.10 Krone Trailer

- 10.11 Lamberet

- 10.12 Manac

- 10.13 MaxiTRANS

- 10.14 Montracon

- 10.15 Schmitz Cargobull

- 10.16 Singamas Container

- 10.17 Sinotruk

- 10.18 Thermo King

- 10.19 Utility Trailer Manufacturing Company

- 10.20 Wabash National