PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740922

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740922

Automotive Fuel Gauge Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

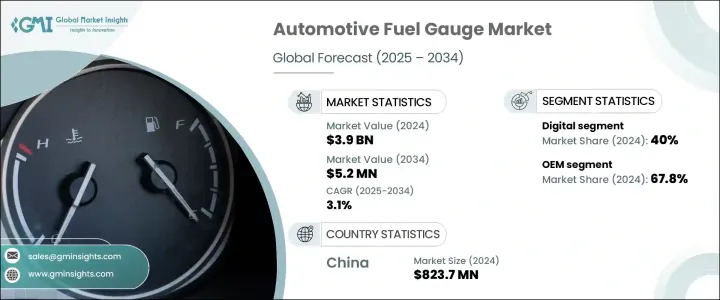

The Global Automotive Fuel Gauge Market was valued at USD 3.9 billion in 2024 and is estimated to grow at a CAGR of 3.1% to reach USD 5.2 billion by 2034, driven by the vehicles and fleet digitalization, with the demand for advanced fuel gauge systems integrated with telematics. Fleet managers need continuous access to real-time fuel data to optimize costs, schedule maintenance, and monitor driver behavior. These smart gauges, linked through telematics, can provide instant fuel level updates, identify issues such as fuel theft or leaks, and send alerts for refueling needs. This integration supports predictive maintenance and reduces operational downtime, making the systems crucial in logistics, public transportation, and shared mobility services.

Technological advancements in sensor design have greatly improved the performance of automotive fuel gauges. Modern sensors, including capacitive, ultrasonic, and resistive types, offer better accuracy, faster response times, and greater durability under various operating conditions. These sensors adapt to different tank sizes and fuel types, including biofuels and ethanol blends. This increased precision reduces false readings and ensures reliable fuel data, which is critical for both personal and fleet vehicle operations. Additionally, sensor miniaturization has improved integration in compact vehicle designs, enhancing overall functionality.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.9 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 3.1% |

The automotive fuel gauge market is segmented by technology, including analog, hybrid display, head-up display, and digital options. In 2024, the digital segment took the lead with a 40% market share, expected to grow at a 3.7% CAGR through 2034. This growth is fueled by the increasing electrification of vehicles, the demand for smart dashboard integration, and consumers' preference for accurate and real-time monitoring of fuel or energy usage. Digital fuel gauges are essential for modern vehicles, including electric and hybrid models, providing detailed information on battery range, charge status, and energy flow.

In terms of sales channels, the OEM segment held 67.8% share in 2024 and is expected to grow at a CAGR of 2.8% from 2025 to 2034. The OEM sector remains dominant due to the incorporation of fuel gauges as standard components in newly manufactured vehicles. These gauges are integrated into digital instrument clusters and vehicle diagnostic systems, ensuring compatibility with modern engine management and emissions technologies. Key gauge manufacturers collaborate directly with automotive producers to design custom solutions that fit specific vehicle architectures and dashboard layouts.

China Automotive Fuel Gauge Market held 54% share in 2024 and generated USD 823.7 million, driven by passenger and commercial vehicle production, which has bolstered its position in the fuel gauge market. China benefits from a vertically integrated supply chain, enabling local manufacturers to meet OEM demand efficiently and cost-effectively. The growing volume of vehicle production in the region, coupled with China's significant investment in electric vehicles (EVs) and smart automotive technology, has further contributed to the rising demand for advanced automotive components like fuel gauges.

Key players in the automotive fuel gauge industry include Aptiv, BorgWarner, Bosch, Continental, and Denso. To strengthen their market position, companies in the automotive fuel gauge market focus on strategic collaborations with automotive manufacturers to develop tailored fuel gauge solutions. They invest heavily in technological advancements, particularly sensor design and telematics integration, to enhance accuracy and offer real-time monitoring features. Additionally, companies focus on expanding their presence in emerging markets like Asia Pacific, leveraging local manufacturing capabilities to reduce costs and cater to increasing demand for advanced fuel management systems. By focusing on the electrification of vehicles and increasing use of connected technologies, these companies are positioning themselves to lead in a rapidly evolving automotive market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Manufacturers

- 3.2.2 Raw material suppliers

- 3.2.3 OEM

- 3.2.4 Distribution channel

- 3.2.5 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Cost breakdown analysis

- 3.9 Price analysis

- 3.9.1 By region

- 3.9.2 By propulsion

- 3.10 Regulatory landscape

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Rise in vehicle electrification

- 3.11.1.2 Stricter emission and fuel efficiency regulations

- 3.11.1.3 Advancement in sensor technologies

- 3.11.1.4 Growth in fleet and telematics integration

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 Sensor calibration and accuracy issues

- 3.11.2.2 Integration complexity

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Analog

- 5.3 Digital

- 5.3.1 LCD

- 5.3.2 OLED

- 5.4 Hybrid display

- 5.5 Head-up display

Chapter 6 Market Estimates & Forecast, By Sensor, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Resistive

- 6.3 Capacitive

- 6.4 Ultrasonic

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric vehicles

- 7.3.1 Battery Electric Vehicles (BEV)

- 7.3.2 Plug-in Hybrid Electric Vehicles (PHEV)

- 7.3.3 Hybrid Electric Vehicles (HEV)

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Passenger vehicles

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUV

- 8.3 Commercial vehicles

- 8.3.1 Light Commercial Vehicles (LCV)

- 8.3.2 Medium Commercial Vehicles (MCV)

- 8.3.3 Heavy Commercial Vehicles (HCV)

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Aptiv

- 11.2 Auto Meter Products

- 11.3 AUTOGAUGE

- 11.4 Continental

- 11.5 DENSO

- 11.6 DunkTeam

- 11.7 Equus Products

- 11.8 Faria Beede Instruments

- 11.9 Gee Kay Equipments

- 11.10 GlowShift Gauges

- 11.11 Iontra

- 11.12 KUS USA

- 11.13 Marshall Instruments

- 11.14 Minda

- 11.15 Pricol

- 11.16 Robert Bosch

- 11.17 Sierra Instruments

- 11.18 Stoneridge

- 11.19 Wonfly

- 11.20 Yazaki