PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740938

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740938

Commercial Vehicle Crankshaft Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

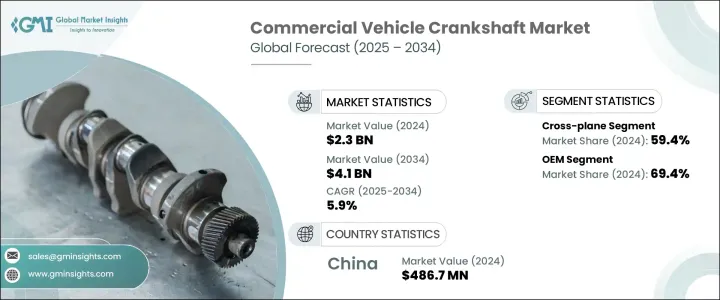

The Global Commercial Vehicle Crankshaft Market was valued at USD 2.3 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 4.1 billion by 2034, driven by rising commercial vehicle production and the rapid expansion of global transportation and logistics sectors. As industries worldwide race toward zero-emission targets, the need for more efficient, cleaner vehicle technologies is creating significant momentum across the crankshaft industry. The growing demand for hybrid, electric, and transitional powertrains is reshaping material requirements and performance expectations, pushing manufacturers to innovate lighter, more durable crankshaft solutions. Fleet operators are increasingly investing in next-generation commercial vehicles that bridge traditional internal combustion systems with electrified platforms, boosting the need for high-performance components that deliver both efficiency and reliability. Evolving supply chain dynamics, stricter emissions regulations, and a heightened focus on fuel economy are compelling OEMs and suppliers to reimagine traditional crankshaft designs. Companies are now channeling resources into smarter predictive maintenance technologies, lightweight alloys, and precision manufacturing techniques to meet the rising standards of global fleets. The growing adoption of vehicle-to-grid (V2G) systems, particularly in heavy-duty segments like logistics trucks and buses, further highlights the ongoing need for advanced crankshaft designs that support sustainability while maximizing engine performance.

Increased integration of commercial fleets into smart grid systems is also influencing crankshaft design requirements. Vehicles participating in V2G networks still depend heavily on internal combustion or hybrid engines during this transitional phase, making it crucial for crankshafts to support lower emissions and enhanced fuel efficiency. This trend ties directly into the broader automotive shift toward blending legacy systems with future-forward mobility solutions. Across the value chain, OEMs and component manufacturers are prioritizing the development of lightweight, high-strength crankshafts with better heat resistance and vibration control. At the same time, regulatory incentives across North America, Europe, and Asia targeting emissions reduction are accelerating investments in high-performance crankshaft technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $4.1 Billion |

| CAGR | 5.9% |

In 2024, the cross-plane crankshaft segment dominated with a 59.4% market share, largely because of its superior vibration damping, torque consistency, and dynamic balance. These features are vital for long-haul trucks, industrial buses, and other heavy-duty vehicles that operate under extreme load conditions across diverse terrains. Cross-plane crankshafts also enhance compatibility with large displacement and hybrid engines, ensuring smooth torque delivery critical for optimal fuel efficiency and drivability.

From a sales channel standpoint, OEMs accounted for a commanding 69.4% share in 2024 and are projected to grow at a CAGR of 6.8% through 2034. OEMs are increasingly collaborating with crankshaft manufacturers to co-develop application-specific forged designs that prioritize strength, fatigue resistance, and thermal efficiency.

China Commercial Vehicle Crankshaft Market led globally with a 54.2% share, generating USD 486.7 million in 2024. The country's dominance stems from its massive commercial vehicle production scale and vertically integrated supply chain. Cities like Chongqing, Jinan, and Guangzhou have emerged as key manufacturing hubs, supported by government initiatives, skilled labor pools, and strong OEM partnerships. Investments in automated forging lines, robotic machining, and stringent quality control are reinforcing China's leadership position.

Key players in the global market include Bharat Forge, thyssenkrupp, MAHLE, Rheinmetall, Kellogg Crankshaft Company, Crower Cams & Equipment, NSI Crankshaft, ZF Friedrichshafen, Nippon Steel, and Tianrun Industrial Technology. Industry leaders are prioritizing R&D for high-strength, low-weight materials, enhancing CNC automation, forging deeper OEM collaborations, and advancing digital integration to track maintenance and optimize emissions performance, keeping pace with the evolving landscape of commercial mobility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Manufacturers

- 3.2.2 Raw material suppliers

- 3.2.3 Automotive OEM

- 3.2.4 Distribution channel

- 3.2.5 End-use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Pricing analysis

- 3.9.1 Propulsion

- 3.9.2 Region

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rising demand for commercial vehicles

- 3.10.1.2 Expansion of transportation and logistics sector

- 3.10.1.3 Adoption of lightweight and high-strength materials

- 3.10.1.4 Ongoing technological advancements in commercial vehicle crankshaft

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High manufacturing cost

- 3.10.2.2 Supply chain disruption

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Crankshaft, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Flat plane

- 5.3 Cross plane

- 5.4 Modular

Chapter 6 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Forged steel

- 6.3 Cast iron/steel

- 6.4 Machined billet

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Diesel

- 7.3 Natural gas

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Light Commercial Vehicles (LCV)

- 8.3 Medium Commercial Vehicles (MCV)

- 8.4 Heavy Commercial Vehicles (HCV)

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEMs

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Aichi Steel

- 11.2 Atlas Industries

- 11.3 Bharat Forge

- 11.4 Bharat gears

- 11.5 Bryan Tools & Engineering

- 11.6 China Zhongwang Holdings

- 11.7 CIE Automotive

- 11.8 Crower Cams & Equipment Company

- 11.9 Indian Crankshaft Manufacturing Company (ICM)

- 11.10 Kellogg Crankshaft Company

- 11.11 MAHLE

- 11.12 Metalurgica Riosulense S/A

- 11.13 Molnar Technologies

- 11.14 Nippon Steel

- 11.15 NSI Crankshaft

- 11.16 Rheinmetall

- 11.17 Teksid

- 11.18 thyssenkrupp

- 11.19 Tianrun Crankshaft

- 11.20 ZF Friedrichshafen