PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740972

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740972

U.S. Home Remodeling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

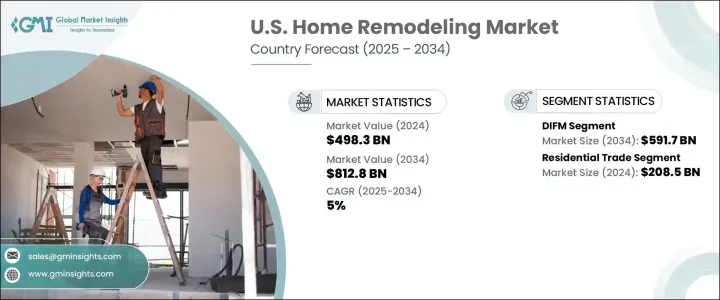

U.S. Home Remodeling Market was valued at USD 498.3 billion in 2024 and is estimated to grow at a CAGR of 5% to reach USD 812.8 billion by 2034. This growth is largely driven by the aging housing stock across the nation, where the median home age has crossed four decades. As properties continue to age, the need for renovations that enhance energy efficiency, modern aesthetics, and functional design becomes increasingly critical. Homeowners are becoming more proactive in addressing issues that arise from years of wear and delayed maintenance, especially repairs that boost long-term durability. These include structural improvements, thermal insulation, upgraded windows, and climate control systems. Periods of economic downturn have often led to postponed maintenance, which now fuels a surge in renovation demand as households catch up on long-overdue updates.

At the same time, evolving lifestyles are prompting people to reevaluate how they use their living spaces. The rise of flexible work arrangements has pushed homeowners to rethink interiors, optimizing space to suit both professional and personal needs. Living areas are being transformed into dual-purpose environments that support work, fitness, and leisure without the need for relocation. Many are prioritizing upgrades that offer better lighting, enhanced acoustics, and smart technology integration that aligns with changing lifestyle expectations. This shift, initially catalyzed by the remote work trend, has now become a long-term behavioral change, driving greater investment in residential improvement projects.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $498.3 Billion |

| Forecast Value | $812.8 Billion |

| CAGR | 5% |

Within the project category, the market is divided into two core segments: DIY (do-it-yourself) and DIFM (do-it-for-me). The DIFM segment dominated the market in 2024 with a value of USD 361.2 billion and is forecasted to reach USD 591.7 billion by 2034. DIFM continues to lead due to growing consumer preference for professionally executed remodeling projects. A combination of factors-including an aging population, increasingly hectic schedules, and the technical complexities involved in modern renovation work-has encouraged homeowners to rely more heavily on experts. This professional dependency ensures code compliance, higher quality outcomes, and efficient project timelines.

Contractors are being increasingly trusted for high-value remodeling efforts across different parts of the home, from structural modifications to aesthetic enhancements. Consumers today are willing to invest more not just for superior results but also for the convenience that comes with professional oversight. The rise in home equity and growing disposable income further contribute to the willingness of homeowners to delegate renovation responsibilities to professionals. This uptick in managed projects also benefits tradespeople and wholesalers, stimulating further activity across the remodeling supply chain.

On the wholesale front, the market is segmented into residential trade, residential showroom, and B2C. In 2024, the residential trade segment held the largest share, valued at USD 208.5 billion. It is expected to grow at a CAGR of 5.2% through the forecast period. The dominance of this segment stems from its strong ties with remodeling contractors, builders, and professional renovation firms, who consistently purchase building materials and fixtures in bulk. Their repeat business supports a reliable demand for a wide range of supplies, from HVAC systems to plumbing and structural materials.

Residential trade remains a cornerstone of the wholesale channel because of its capacity to offer better pricing, favorable credit arrangements, and logistical advantages. Professionals who rely on this channel often handle multiple projects simultaneously, making bulk procurement both practical and cost-effective. This steady flow of materials not only ensures smoother project execution but also strengthens the position of wholesalers in a highly competitive environment.

Several well-established companies continue to shape the U.S. home remodeling landscape. Notable players include Andersen, ABC Supply, Builders FirstSource, Enterprise Wholesale, Ferguson, Harvey Building Products, JELD-WEN, Kohler, LU Kitchen & Bath, Masco, National Wholesale Supply, Pella, Robert Bowden, The Home Depot, and The Sherwin-Williams. These companies have been proactive in adjusting to shifts in consumer expectations and economic conditions. Their strategies focus on integrating sustainable construction technologies and energy-efficient solutions while enhancing customer engagement and automating project workflows. These efforts not only support innovation and service quality but also ensure that businesses stay competitive as market demands continue to evolve.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast parameters

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.1.7 Retailers

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the Industry

- 3.2.2.1 Supply-Side impact (Raw Materials)

- 3.2.2.2 Price volatility in key materials

- 3.2.2.3 Supply chain restructuring

- 3.2.2.4 Production cost implications

- 3.2.2.5 Demand-Side impact (Selling price)

- 3.2.2.6 Price transmission to end markets

- 3.2.2.7 Market share dynamics

- 3.2.2.8 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Aging housing stock and need for upgrades

- 3.3.1.2 Rise in remote work and home functionality needs

- 3.3.1.3 Home equity and financing availability

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 Rising material and labor costs impacting project affordability

- 3.3.2.2 Regulatory complexities and permit delays slowing renovation timelines

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Raw Material analysis

- 3.6 Regulatory landscape

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Consumer behavior analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Project, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 DIY

- 5.3 DIFM

Chapter 6 Market Estimates & Forecast, By Wholesale, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Residential trade

- 6.3 Residential showroom

- 6.4 B2C

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Windows & doors

- 7.3 Kitchen additions & improvements

- 7.4 Bathroom additions & improvements

- 7.5 Landscaping

- 7.6 Flooring

- 7.7 Roofing

- 7.8 HVAC

- 7.9 Pools/Hot tubs

- 7.10 Electrical construction

- 7.11 Other room additions & alterations

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 Direct selling through online

- 8.3 Direct selling to consumers

- 8.4 Wholesale to retailer

- 8.5 Wholesale to consumer

- 8.6 Wholesalers selling online

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Billion)

- 9.1 Key trends

- 9.2 Northeast U.S.

- 9.2.1 Pennsylvania

- 9.2.2 New York

- 9.2.3 Vermont

- 9.2.4 New Hampshire

- 9.2.5 Massachusetts

- 9.2.6 Maine

- 9.2.7 Rhode Island

- 9.2.8 Connecticut

- 9.2.9 New Jersey

- 9.2.10 Delaware

- 9.2.11 Maryland

- 9.3 Southeast U.S.

- 9.3.1 Arkansas

- 9.3.2 Louisiana

- 9.3.3 Mississippi

- 9.3.4 Alabama

- 9.3.5 Georgia

- 9.3.6 Florida

- 9.3.7 South Carolina

- 9.3.8 Tennessee

- 9.3.9 North Carolina

- 9.3.10 Virginia

- 9.3.11 West Virginia

- 9.3.12 Kentucky

- 9.4 Midwest U.S

- 9.4.1 North Dakota

- 9.4.2 South Dakota

- 9.4.3 Nebraska

- 9.4.4 Kansas

- 9.4.5 Minnesota

- 9.4.6 lowa

- 9.4.7 Missouri

- 9.4.8 Wisconsin

- 9.4.9 Illinois

- 9.4.10 Michigan

- 9.4.11 Indiana

- 9.4.12 Ohio

- 9.5 Northwest U.S.

- 9.5.1 Washington

- 9.5.2 Oregon

- 9.5.3 California

- 9.5.4 Nevada

- 9.5.5 Idaho

- 9.5.6 Montana

- 9.5.7 Wyoming

- 9.5.8 Alaska

- 9.5.9 Utah

- 9.5.10 Colorado

- 9.6 Southwest U.S.

- 9.6.1 Arizona

- 9.6.2 New Mexico

- 9.6.3 Texas

- 9.6.4 Hawaii

- 9.6.5 Oklahoma

Chapter 10 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 1.1 ABC Supply

- 1.2 Andersen

- 1.3 Builders FirstSource

- 1.4 Enterprise Wholesale

- 1.5 Ferguson

- 1.6 Harvey Building Products

- 1.7 JELD-WEN

- 1.8 Kohler

- 1.9 LU Kitchen & Bath

- 1.10 Masco

- 1.11 National Wholesale Supply

- 1.12 Pella

- 1.13 Robert Bowden

- 1.14 The Home Depot

- 1.15 The Sherwin-Williams