PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740975

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740975

Construction Repair Composites Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

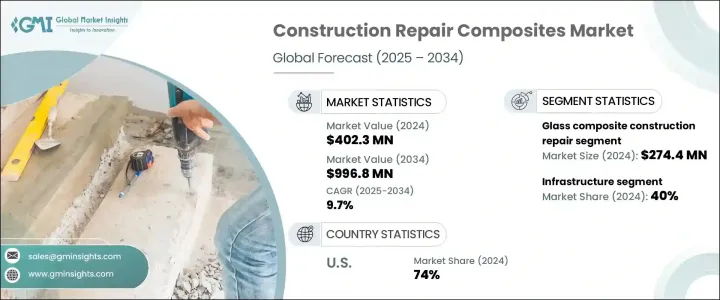

The Global Construction Repair Composites Market was valued at USD 402.3 million in 2024 and is estimated to grow at a CAGR of 9.7% to reach USD 996.8 million by 2034, driven by several key factors shaping global construction trends. The market is witnessing strong momentum due to growing investments in sustainable construction materials, technological progress in composite manufacturing, and increasing efforts to rehabilitate aging infrastructure. As urban development accelerates and sustainability becomes a top priority, composite materials are emerging as a preferred solution for repair applications in the built environment.

The rising need for durable and cost-efficient solutions has positioned composites as a valuable alternative to traditional construction materials. Their superior performance in terms of strength, corrosion resistance, and longevity is increasingly recognized across the construction industry. In many regions with aging infrastructure, there is a clear shift toward the use of composite materials to repair and reinforce deteriorating structures. Rapid urban expansion in developing countries also contributes to market demand, as it creates pressure to not only build new infrastructure but also upgrade existing ones. Additionally, the shift toward smart city development has made advanced materials a priority, with composites playing a vital role in modern repair applications aimed at reducing long-term maintenance costs and improving sustainability. Government investments in public infrastructure renewal are further fueling the adoption of composites, especially in sectors that require long-term performance under challenging environmental conditions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $402.3 Million |

| Forecast Value | $996.8 Million |

| CAGR | 9.7% |

By fiber type, the construction repair composites market is segmented into carbon fiber, glass fiber, and others. In 2024, the glass fiber segment dominated the market, accounting for USD 274.4 million in revenue, and is projected to grow at a CAGR of around 9.9% through 2034. Glass fiber composites continue to gain traction because they offer a combination of affordability, durability, and mechanical strength. These composites are commonly used to reinforce and repair a wide range of construction components, providing extended service life and reduced maintenance compared to conventional options.

Glass fiber composites are widely applied in repairing structural elements such as beams, columns, and foundations, where their strength and resilience offer a practical advantage. Advancements in fabrication techniques, including resin infusion and pultrusion, have improved the structural performance of these materials, making them more reliable and adaptable to diverse construction repair needs. Their lightweight nature also simplifies installation, cutting down labor costs and project timeframes. This makes glass fiber a compelling choice for both commercial and residential repair applications, particularly when structural integrity and long-term durability are critical.

In terms of application, the construction repair composites market is divided into residential buildings, commercial buildings, industrial facilities, and infrastructure. Among these, the infrastructure segment held a substantial share of around 40% in 2024. Repair and strengthening of critical infrastructure are primary drivers of composite adoption in this category. Composite materials are increasingly integrated into repair projects to enhance structural resilience and extend the operational lifespan of aging systems.

In regions with mature infrastructure networks, the need to rehabilitate old structures without compromising their integrity is pushing the use of high-performance composites. Carbon fiber composites, in particular, are experiencing rising demand in projects requiring high tensile strength and minimal weight. These characteristics make them ideal for reinforcing components that must bear substantial loads while remaining structurally efficient. Their non-corrosive properties also make them suitable for environments where exposure to moisture or chemicals is common.

North America remains a leading region in the construction repair composites market, with the United States accounting for roughly 74% of the regional market share in 2024 and generating about USD 103 million in revenue. The U.S. market is benefiting from strong federal support for infrastructure modernization through policy initiatives focused on rehabilitation and sustainability. Legislative efforts aimed at infrastructure revitalization are translating into heightened demand for advanced repair materials that deliver both strength and durability.

Composite materials are being embraced for their ability to meet the technical requirements of infrastructure renewal while also aligning with environmental goals. From transportation networks to public utilities, there is a growing preference for solutions that minimize downtime and extend structure lifespans. This growing preference is fueling innovation and wider adoption of fiber-reinforced composites across the country.

Key players operating in the global construction repair composites market include Chomarat, BASF, Creative Composites, Dow, Fosroc, Dextra, Henkel, Mapei, Owens Corning, Rockwool, Master Builders Solutions, Saint-Gobain, Simpson Strong-Tie, Sika, and Sireg Geotech. These companies are focusing on material innovation, expanding product lines, and forging strategic partnerships to strengthen their position in a market that is becoming increasingly competitive and quality-driven.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations.

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain.

- 3.1.2 Profit margin analysis.

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufactures

- 3.1.6 Distributors

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Aging infrastructure and need for renovation

- 3.6.1.2 Urbanization and rapid infrastructure development

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Performance variability in extreme conditions

- 3.6.2.2 Competition from traditional materials

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Fiber Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Glass fiber

- 5.3 Carbon fiber

- 5.4 Others (aramid fiber etc.)

Chapter 6 Market Estimates & Forecast, By Resin Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Thermoset resins

- 6.2.1 Polyester

- 6.2.2 Epoxy

- 6.2.3 Vinyl ester

- 6.2.4 Polyurethane

- 6.2.5 Others (phenolic etc.)

- 6.3 Thermoplastic resins

- 6.3.1 Polypropylene

- 6.3.2 Polyamide

- 6.3.3 Polycarbonate

- 6.3.4 Others (polyetheretherketone etc.)

Chapter 7 Market Estimates & Forecast, By Product Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Textile/fabric

- 7.3 Plate

- 7.4 Rebar

- 7.5 Mesh

- 7.6 Others (adhesive etc.)

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Residential buildings

- 8.3 Commercial buildings

- 8.4 Industrial facilities

- 8.5 Infrastructure

- 8.5.1 Bridges

- 8.5.2 Roads and highways

- 8.5.3 Tunnels

- 8.5.4 Pipes and water systems

- 8.5.5 Others (marine Infrastructure etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 BASF

- 11.2 Chomarat

- 11.3 Creative Composites

- 11.4 Dextra

- 11.5 Dow

- 11.6 Fosroc

- 11.7 Henkel

- 11.8 Mapei

- 11.9 Master Builders Solutions

- 11.10 Owens Corning

- 11.11 Rockwool

- 11.12 Saint-Gobain

- 11.13 Sika

- 11.14 Simpson Strong-Tie

- 11.15 Sireg Geotech