PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750285

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750285

Geopolymer Cement Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

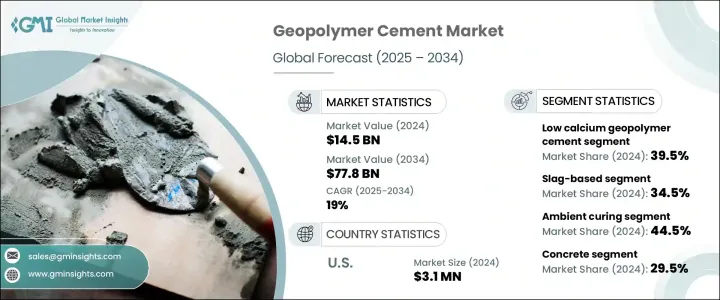

The Global Geopolymer Cement Market was valued at USD 14.5 billion in 2024 and is estimated to grow at a CAGR of 19% to reach USD 77.8 billion by 2034. As the construction industry shifts toward environmentally responsible practices, the appeal of low-emission materials continues to grow. This trend is largely influenced by the increasing urgency to combat climate change and comply with evolving environmental regulations. As governments introduce stricter sustainability mandates, industries are actively seeking cleaner, high-performance alternatives to traditional construction materials. Geopolymer cement stands out in this regard due to its low carbon footprint, generating up to 90% fewer carbon emissions compared to conventional Portland cement. It offers not only a more sustainable solution but also superior mechanical and chemical properties, making it a preferred choice in infrastructure development. The push for decarbonization across sectors is driving demand for innovative materials that support long-term ecological goals, and geopolymer cement fits the bill with its energy efficiency and reduced reliance on virgin raw materials.

In addition to regulatory pressures, rising global urbanization is fueling the need for durable and cost-effective building materials. As development accelerates in various parts of the world, especially in growing economies, investment in transport networks, commercial spaces, and residential projects is surging. Geopolymer cement is gaining market traction as it meets both the technical and environmental demands of modern construction. Its resistance to extreme weather conditions and long-lasting durability make it particularly suitable for high-stress applications. The increasing adoption of sustainable building codes and incentives for green construction is further supporting market expansion. As industries and governments seek reliable alternatives that align with circular economy goals, geopolymer cement is emerging as a frontrunner.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.5 Billion |

| Forecast Value | $77.8 Billion |

| CAGR | 19% |

Cost efficiency plays a crucial role in the material's growing popularity. Geopolymer cement leverages industrial waste products like fly ash and blast furnace slag, which reduces the overall production cost while also minimizing energy consumption during manufacturing. These raw materials are often sourced from other industrial processes, creating a closed-loop system that supports sustainability goals. Alongside its lower production expenses, the material delivers excellent resistance to heat and chemicals, making it an economically and environmentally viable option for a wide range of construction needs.

In 2024, low calcium geopolymer cement captured the highest market share, accounting for 39.5% of global revenue. This type is primarily derived from fly ash and is recognized for its strong thermal resistance, chemical stability, and reduced environmental impact. These attributes make it a preferred choice in applications requiring high performance under extreme conditions. On the raw material front, the combined share of fly ash-based and slag-based segments reached 34.5% of the total market. These materials are not only readily accessible but also deliver excellent compressive strength and long-term durability. Their utilization contributes to reducing landfill waste and greenhouse gas emissions, aligning with global sustainability targets.

Curing techniques significantly influence the performance and applicability of geopolymer cement. In 2024, ambient curing held the dominant position, with a market share of 44.5%. This method is favored for its low energy requirement and simplified process, which makes it ideal for general construction and maintenance work. For time-sensitive or structurally demanding projects, heat curing is preferred as it enhances strength and reduces setting time. Both techniques offer flexibility depending on project specifications, broadening the material's applicability across sectors.

From an application perspective, concrete led the market with a 29.5% share. Geopolymer concrete offers excellent strength, low shrinkage, and high chemical resistance, making it a go-to material for large-scale projects. Its compliance with green building standards adds to its appeal among contractors and developers seeking LEED certifications or similar sustainability credentials. The building and construction sector represented the largest end-use industry in 2024, holding 34.5% of the total market. Its widespread use in residential, commercial, and industrial settings highlights the material's adaptability and growing importance in eco-conscious construction practices.

Regionally, the United States emerged as the leading market, valued at USD 3.1 million in 2024 and accounting for over 80% of the global share. The country's strong position is supported by rising infrastructure investment, strict environmental guidelines, and a growing commitment to sustainable development. Easy access to raw materials such as fly ash and slag also supports domestic production and adoption, reducing supply chain challenges and lowering carbon impact. The US market continues to grow due to favorable policies and technological advancements in sustainable building materials.

Leading companies in the geopolymer cement market are investing heavily in research and development to refine formulations and improve product performance. By focusing on proprietary technologies and next-generation manufacturing methods, these players aim to deliver consistent quality and enhance application flexibility. Their efforts to innovate while expanding distribution networks are enabling them to address varied customer needs and maintain a competitive edge in an evolving global landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research Methodology

- 1.2 Research Objectives

- 1.3 Market Definition and Scope

- 1.4 Market Segmentation

- 1.5 Data Sources

- 1.5.1 Primary Research

- 1.5.2 Secondary Research

- 1.6 Market Estimation Approach

- 1.7 Research Assumptions and Limitations

- 1.8 Base Year and Forecast Period

Chapter 2 Executive Summary

- 2.1 Market Snapshot

- 2.2 Segment Highlights

- 2.3 Competitive Landscape Snapshot

- 2.4 Regional Market Outlook

- 2.5 Key Market Trends

- 2.6 Future Market Outlook

Chapter 3 Industry Insights

- 3.1 Market Introduction

- 3.2 Impact of trump administration tariffs – structured overview

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1.1 Supply-side impact (raw materials)

- 3.2.2.1.2 Price volatility in key materials

- 3.2.2.1.3 Supply chain restructuring

- 3.2.2.1.4 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets.

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code) Note: the above trade statistics will be provided for key countries only.

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

- 3.4 Industry value chain analysis

- 3.5 Profit margin analysis

- 3.6 Product overview

- 3.6.1 Geopolymer chemistry & formation

- 3.6.2 Comparison with Portland cement

- 3.6.3 Environmental benefits & carbon footprint

- 3.6.4 Mechanical properties & performance characteristics

- 3.6.5 Durability & resistance properties

- 3.6.6 Setting time & workability

- 3.6.7 Limitations & challenges

- 3.7 Market dynamics

- 3.7.1 Market drivers

- 3.7.1.1 Environmental regulations and sustainability initiatives.

- 3.7.1.2 Growing infrastructure development, particularly in emerging economies.

- 3.7.1.3 Cost advantages over traditional cement, including reduced CO2 emissions and energy consumption.

- 3.7.2 Market restraints

- 3.7.2.1 Declining operations in key industries like coal and steel.

- 3.7.2.2 Technical limitations in certain applications, restricting wider use.

- 3.7.2.3 Lack of awareness and technical knowledge among contractors and builders.

- 3.7.3 Market opportunities

- 3.7.3.1 Increasing focus on green building materials.

- 3.7.3.2 Rising demand for durable and high-performance infrastructure solutions.

- 3.7.3.3 Technological advancements in geopolymer formulations.

- 3.7.4 Market challenges

- 3.7.4.1 Standardization and certification issues.

- 3.7.4.2 Competition from established cement types.

- 3.7.4.3 Cost competitiveness with conventional cement.

- 3.7.1 Market drivers

- 3.8 Industry impact forces

- 3.8.1 Growth potential analysis

- 3.8.2 Industry pitfalls & challenges

- 3.9 Regulatory framework & standards

- 3.9.1 Building codes & construction standards

- 3.9.2 Environmental regulations

- 3.9.3 Carbon Pricing & Emissions Trading

- 3.9.4 Green building certifications

- 3.9.5 Waste material utilization policies

- 3.10 Manufacturing process analysis

- 3.10.1 Raw material preparation

- 3.10.2 Alkaline activator production

- 3.10.3 Mixing & formulation

- 3.10.4 Curing methods

- 3.10.5 Quality control procedures

- 3.11 Raw material analysis & procurement strategies

- 3.12 Pricing analysis

- 3.13 Sustainability & environmental impact assessment

- 3.14 Pestle analysis

- 3.15 Porter's five forces analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Market share analysis

- 4.2 Strategic framework

- 4.2.1 Mergers & acquisitions

- 4.2.2 Joint ventures & collaborations

- 4.2.3 New product developments

- 4.2.4 Expansion strategies

- 4.3 Competitive benchmarking

- 4.4 Vendor landscape

- 4.5 Competitive positioning matrix

- 4.6 Strategic dashboard

- 4.7 Patent analysis & innovation assessment

- 4.8 Market entry strategies for new players

- 4.9 Research & development intensity analysis

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Low calcium geopolymer cement

- 5.3 High calcium geopolymer cement

- 5.4 Phosphate-based geopolymer cement

- 5.5 Silicate-based geopolymer cement

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Raw Material Source, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Fly Ash-Based

- 6.2.1 Class F fly ash

- 6.2.2 Class C fly ash

- 6.2.3 Other fly ash types

- 6.3 Slag-Based

- 6.3.1 Ground granulated blast furnace slag (GGBFS)

- 6.3.2 Other slag types

- 6.4 Metakaolin-based

- 6.5 Natural aluminosilicate-based

- 6.6 Red mud-based

- 6.7 Hybrid & blended systems

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Curing Method, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Ambient curing

- 7.3 Heat curing

- 7.4 Steam curing

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Concrete

- 8.2.1 Ready-mix concrete

- 8.2.2 Precast concrete

- 8.2.3 Other concrete applications

- 8.3 Mortar & grouts

- 8.4 Precast elements

- 8.4.1 Blocks & bricks

- 8.4.2 Panels & slabs

- 8.4.3 Pipes & columns

- 8.4.4 Other precast elements

- 8.5 Pavements & overlays

- 8.6 Repair & rehabilitation

- 8.7 Waste encapsulation & immobilization

- 8.8 Other applications

Chapter 9 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Building & construction

- 9.2.1 Residential

- 9.2.2 Commercial

- 9.2.3 Industrial

- 9.3 Infrastructure

- 9.3.1 Roads & bridges

- 9.3.2 Dams & water management

- 9.3.3 Airports & ports

- 9.3.4 Other infrastructure

- 9.4 Oil & gas

- 9.5 Mining

- 9.6 Marine & underwater construction

- 9.7 Nuclear & waste management

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By Performance Attribute, 2021 - 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 High strength

- 10.3 Chemical resistance

- 10.4 Fire resistance

- 10.5 Low shrinkage

- 10.6 Rapid setting

- 10.7 Other performance attributes

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.2.3 Mexico

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 Alchemy Geopolymer Solutions, LLC

- 12.2 Banah UK Ltd.

- 12.3 BASF SE

- 12.4 CEMEX S.A.B. de C.V.

- 12.5 Ceratech Inc.

- 12.6 Concrete Canvas Ltd.

- 12.7 Dow Chemical Company

- 12.8 GCP Applied Technologies Inc.

- 12.9 Geobeton Pty Ltd.

- 12.10 Geopolymer Products

- 12.11 Geopolymer Solutions, LLC

- 12.12 Halliburton

- 12.13 Imerys S.A.

- 12.14 Kiran Global Chems Limited

- 12.15 LafargeHolcim Ltd.

- 12.16 Metna Co.

- 12.17 Milliken Infrastructure Solutions, LLC

- 12.18 Nu-Core

- 12.19 PCI Augsburg GmbH

- 12.20 Pyromeral Systems

- 12.21 Reno Refractories, Inc.

- 12.22 Rocla Pty Limited

- 12.23 Schlumberger Limited

- 12.24 Sika AG

- 12.25 Siloxo Pty Ltd.

- 12.26 Tech-Crete Processors Ltd.

- 12.27 Uretek Worldwide

- 12.28 Wagners

- 12.29 Wollner GmbH

- 12.30 Zeobond Pty Ltd.