PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750344

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750344

Slag Cement (GGBFS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

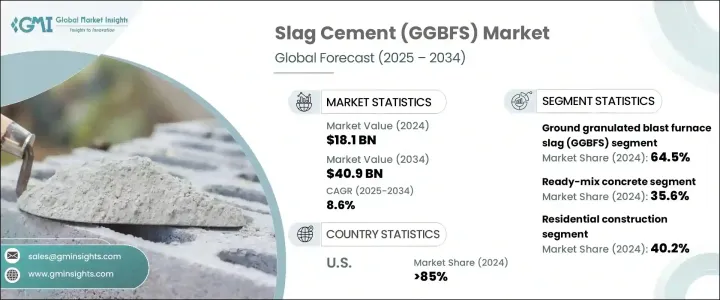

The Global Slag Cement Market was valued at USD 18.1 billion in 2024 and is estimated to grow at a CAGR of 8.6% to reach USD 40.9 billion by 2034, driven by increasing investments in infrastructure, a growing demand for sustainable construction materials, and regulatory support for alternatives with a low carbon footprint.

Slag cement, especially ground granulated blast furnace slag (GGBFS), is increasingly preferred in modern construction due to its exceptional performance characteristics. It not only delivers enhanced compressive strength and reduced permeability but also significantly improves resistance to chemical attacks, making it ideal for aggressive environmental conditions. These attributes contribute to longer-lasting infrastructure, reducing the frequency and expense of repairs over time. Additionally, GGBFS reduces the heat of hydration, which helps prevent thermal cracking in large concrete pours, thereby increasing structural integrity. Its use in concrete mixtures also improves workability and finish quality, benefiting both the construction process and the result. As sustainability becomes a priority in building practices, the low-carbon footprint of slag cement further amplifies its value in residential and large-scale infrastructure projects.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.1 Billion |

| Forecast Value | $40.9 Billion |

| CAGR | 8.6% |

The GGBFS segment accounted for 64.5% of the market share in 2024. Its superior strength, decreased permeability, and increased durability make it ideal for critical infrastructure projects, including bridges, tunnels, and marine structures. Additionally, GGBFS contributes to reducing the carbon footprint of concrete, promoting its use in sustainable building practices.

The residential construction segment held a 40.2% market share in 2024. As demand for housing increases, there is a need for durable, long-lasting building materials. Slag cement is gaining popularity in residential projects due to its superior strength, reduced shrinkage, and fire resistance, aligning with the trend towards sustainable housing.

North America Slag Cement Market held 85% share and was valued at USD 1.8 million in 2024, attributed to expanding infrastructure investments and a strong interest in sustainable construction. Policies like the Infrastructure Investment and Jobs Act (IIJA) have driven high demand for high-performance building materials like slag cement. Furthermore, the construction industry's push for carbon reduction is accelerating the adoption of slag cement, reducing the overall carbon footprint of concrete finishes.

Key players in the Global Slag Cement Market include JSW Cement, CEMEX S.A.B. de C.V., Ecocem Materials, Holcim Group, and Heidelberg Materials. These companies are adopting various strategies to strengthen their market presence. They are investing in research and development to improve the performance characteristics of slag cement, such as enhancing its durability and reducing production costs. Additionally, they are expanding their production capacities to meet the growing demand in emerging markets. Strategic partnerships and collaborations are also being pursued to access new markets and leverage local expertise. Furthermore, these companies focus on sustainability initiatives, aligning their operations with environmental regulations and consumer preferences for eco-friendly products.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research methodology

- 1.2 Research objectives

- 1.3 Market definition and scope

- 1.4 Market segmentation

- 1.5 Data sources

- 1.5.1 Primary research

- 1.5.2 Secondary research

- 1.6 Market estimation approach

- 1.7 Research assumptions and limitations

- 1.8 Base year and forecast period

Chapter 2 Executive Summary

- 2.1 Market overview

- 2.2 Market dynamics snapshot

- 2.3 Key market trends

- 2.4 Regional insights

- 2.5 Competitive landscape snapshot

- 2.6 Future market outlook

- 2.7 Investment highlights

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Manufacturers

- 3.1.3 Distributors

- 3.1.4 End use

- 3.1.5 Profit margin analysis

- 3.1.6 Value chain disruptions due to covid-19

- 3.2 Impact of trump administration tariffs - structured overview

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1.1 Supply-side impact (raw materials)

- 3.2.2.1.2 Price volatility in key materials

- 3.2.2.1.3 Supply chain restructuring

- 3.2.2.1.4 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code) Note: the above trade statistics will be provided for key countries only.

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.5.1 Technology landscape

- 3.5.2 Traditional manufacturing technologies

- 3.5.3 Advanced manufacturing technologies

- 3.5.4 Emerging technologies

- 3.5.5 Patent analysis

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Market dynamics

- 3.7.1 Market drivers

- 3.7.1.1 Environmental regulations and sustainability initiatives

- 3.7.1.2 Growing infrastructure development

- 3.7.1.3 Cost advantages over traditional cement

- 3.7.1.4 Superior technical properties and performance benefits

- 3.7.2 Market restraints

- 3.7.2.1 Limited availability of high-quality blast furnace slag

- 3.7.2.2 Declining blast furnace operations due to decarbonization efforts

- 3.7.2.3 Technical limitations in certain applications

- 3.7.2.4 Lack of awareness and technical knowledge

- 3.7.3 Market opportunities

- 3.7.3.1 Increasing focus on green building materials

- 3.7.3.2 Rising demand for durable infrastructure

- 3.7.3.3 Technological advancements in slag processing

- 3.7.3.4 Government incentives for sustainable construction

- 3.7.4 Market challenges

- 3.7.4.1 Competition from other supplementary cementitious materials

- 3.7.4.2 Supply chain disruptions

- 3.7.4.3 Regional availability constraints

- 3.7.4.4 Standardization and quality control issues

- 3.7.5 Regulatory framework analysis

- 3.7.5.1 International standards (ASTM c989/c989m, EN 197-1)

- 3.7.5.2 Regional regulations and standards

- 3.7.5.3 Environmental compliance requirements

- 3.7.5.4 Quality certification systems

- 3.7.6 Technology landscape

- 3.7.6.1 Current technological trends

- 3.7.6.2 Emerging technologies in slag cement production

- 3.7.6.3 Digitalization and industry 4.0 impact

- 3.7.6.4 R&D initiatives and innovation pipeline

- 3.7.7 Pricing analysis

- 3.7.7.1 Price trend analysis

- 3.7.7.2 Cost structure analysis

- 3.7.7.3 Factors affecting pricing

- 3.7.7.4 Regional price variations

- 3.7.8 Pestle analysis

- 3.7.1 Market drivers

Chapter 4 Competitive Landscape, 2024

- 4.1 Market share analysis, 2024

- 4.2 Strategic dashboard

- 4.3 Key stakeholders and market positioning

- 4.4 Competitive benchmarking

- 4.5 Competitive positioning matrix

- 4.6 Competitive strategies

- 4.6.1 New product developments

- 4.6.2 Mergers and acquisitions

- 4.6.3 Partnerships and collaborations

- 4.6.4 Capacity expansions

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Ground granulated blast furnace slag (GGBFS)

- 5.2.1 Grade 80

- 5.2.2 Grade 100

- 5.2.3 Grade 120

- 5.3 Portland slag cement (PSC)

- 5.3.1 Low slag content (25-35%)

- 5.3.2 Medium slag content (36-50%)

- 5.3.3 High slag content (51-65%)

- 5.4 Supersulfated cement

- 5.5 Other slag-based cements

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Ready-mix concrete

- 6.3 Precast concrete

- 6.4 High-performance concrete

- 6.5 Mass concrete applications

- 6.6 Shotcrete

- 6.7 Concrete blocks and pavers

- 6.8 Mortars and grouts

- 6.9 Soil stabilization

- 6.10 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Residential construction

- 7.2.1 Single-family housing

- 7.2.2 Multi-family housing

- 7.3 Commercial construction

- 7.3.1 Office buildings

- 7.3.2 Retail and hospitality

- 7.3.3 Educational institutions

- 7.3.4 Healthcare facilities

- 7.4 Infrastructure development

- 7.4.1 Roads and highways

- 7.4.2 Bridges and tunnels

- 7.4.3 Dams and hydroelectric projects

- 7.4.4 Railways and transit systems

- 7.4.5 Airports

- 7.4.6 Ports and marine structures

- 7.5 Industrial construction

- 7.5.1 Manufacturing facilities

- 7.5.2 Power plants

- 7.5.3 Oil and gas facilities

- 7.5.4 Water and wastewater treatment plants

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Ambuja Cements Ltd

- 9.2 Boral Limited

- 9.3 Buzzi Unicem

- 9.4 CEMEX S.A.B. de C.V.

- 9.5 Ecocem Materials

- 9.6 Heidelberg Materials

- 9.7 Holcim Group

- 9.8 JFE Mineral & Alloy

- 9.9 JSW Cement

- 9.10 Lafarge

- 9.11 Nippon Steel Corporation

- 9.12 Royal White Cement

- 9.13 Tarmac (CRH)

- 9.14 Texas Lehigh Cement Company LP

- 9.15 Titan America

- 9.16 UltraTech Cement Ltd