PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750418

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750418

AI Training Dataset Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

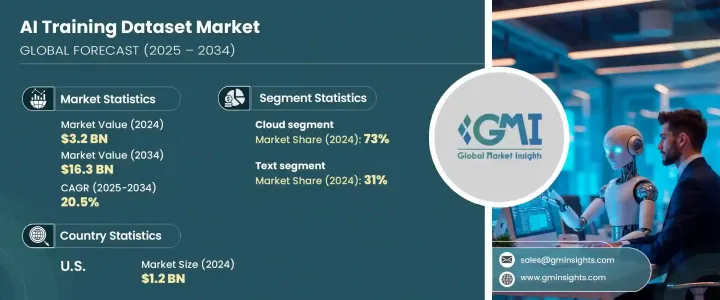

The Global AI Training Dataset Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 20.5% to reach USD 16.3 billion by 2034, fueled by the increasing reliance on artificial intelligence across multiple sectors. As AI applications become more advanced, the need for precise and high-quality labeled datasets becomes increasingly critical. From robotics and healthcare to finance and automation, businesses are integrating AI to streamline operations and reduce human dependency. This shift intensifies the need for accurate training data to build models capable of navigating real-world environments, especially in high-stakes applications like biomedical research and industrial automation.

The demand for tailored datasets continues to rise, as industries strive to enhance operational efficiency and predictive capabilities. Customized, domain-specific data is becoming essential for training AI systems that must operate with precision in highly specialized environments. Whether it's optimizing supply chain logistics, enabling smarter healthcare diagnostics, or improving autonomous navigation, organizations require datasets that are not only large but also accurately labeled and contextually relevant. As AI models become more complex, the need for high-quality, structured, and unbiased data grows even more critical. Tailored datasets help reduce model training time, increase accuracy, and ensure AI solutions are adaptable to real-world conditions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $16.3 Billion |

| CAGR | 20.5% |

In 2024, datasets based on textual content led the market with a 31% share and are expected to grow at a CAGR of 21% through 2034. The dominance of this segment stems from the wide adoption of natural language processing in business intelligence, communication tools, and customer interaction platforms. The boom in digital communications has created an abundance of raw textual content, which organizations are now converting into structured formats suitable for training language-based AI models. The growth of advanced language models has only amplified the requirement for high-quality, multilingual text datasets.

The cloud-based deployment segment held a 73% share in 2024, attributed to its flexibility, scalability, and cost-efficiency. Cloud solutions offer extensive resources for storing, managing, and labeling enormous data volumes while enabling remote collaboration and seamless integration with advanced tools for data processing. These features are essential for organizations to build sophisticated AI systems while maintaining agile operations. Moreover, the security, accessibility, and adaptability provided by cloud services continue to make them the preferred choice for handling training datasets.

United States AI Training Dataset Market held 88% share in 2024, generating USD 1.23 billion. The country's strong technological infrastructure, early AI adoption, and substantial private and public sector investment have created an environment conducive to innovation in data training. Federal funding and collaborative efforts between academia and industry help foster market growth.

Key players in the market include TELUS International, IBM, Amazon Web Services, Lionbridge AI, CloudFactory, Google, Microsoft, NVIDIA, Appen, and iMerit. To enhance their competitive edge, companies in the AI training dataset market focus on several core strategies. Many are investing heavily in automation tools for data labeling and synthetic data generation to cut costs and improve efficiency. Strategic collaborations with academic institutions and research labs are helping expand access to diverse and specialized datasets. Firms are also adopting vertical-specific data solutions to meet the rising demand in sectors such as healthcare, automotive, and retail.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Data originators/collectors

- 3.2.2 Data aggregators & marketplaces

- 3.2.3 Data annotation & labeling service providers

- 3.2.4 Technology & infrastructure providers

- 3.2.5 End-users

- 3.3 Profit margin analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures by other countries

- 3.4.2 Impact on the industry

- 3.4.2.1 Price Volatility in key materials

- 3.4.2.2 Supply chain restructuring

- 3.4.2.3 Data Modality cost implications

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and Data Modality strategies

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising adoption of AI and machine learning across industries

- 3.9.1.2 Growth of computer vision and natural language processing (NLP) applications

- 3.9.1.3 Surge in data annotation outsourcing

- 3.9.1.4 Advancements in autonomous vehicles and robotics

- 3.9.1.5 Increasing investment in AI startups and infrastructure

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High cost and time-intensive nature of data labeling

- 3.9.2.2 Data privacy and security concerns

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Data Modality, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Text

- 5.3 Image

- 5.4 Audio & speech

- 5.5 Video

- 5.6 Multimodal

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud

Chapter 7 Market Estimates & Forecast, By Data Type, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Structured data

- 7.3 Unstructured data

- 7.4 Semi-structured data

Chapter 8 Market Estimates & Forecast, By Data Collection Method, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Public datasets

- 8.3 Private datasets

- 8.4 Synthetic data

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Healthcare

- 9.3 Automotive

- 9.4 BFSI

- 9.5 Retail & e-commerce

- 9.6 IT and telecom

- 9.7 Government and defense

- 9.8 Manufacturing

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Amazon Web Services

- 11.2 Appen

- 11.3 Clickworker

- 11.4 CloudFactory

- 11.5 Cogito Tech

- 11.6 DataLoop

- 11.7 Dataturks

- 11.8 Google

- 11.9 IBM

- 11.10 iMerit

- 11.11 Innodata

- 11.12 Lionbridge AI

- 11.13 LXT

- 11.14 Microsoft

- 11.15 NVIDIA

- 11.16 Sama

- 11.17 Scale AI

- 11.18 TELUS International

- 11.19 TransPerfect

- 11.20 Trillium Data