PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750437

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750437

Mobile C-arm Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

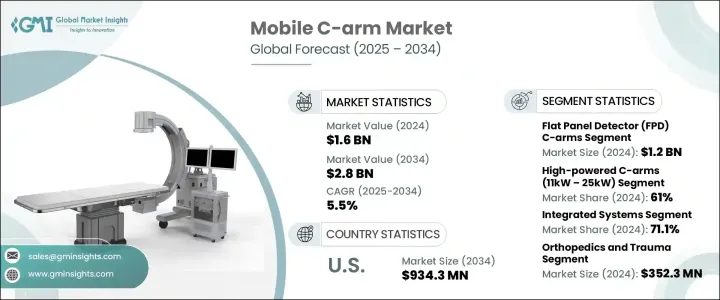

The Global Mobile C-Arm Market was valued at USD 1.6 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 2.8 billion by 2034. Mobile C-arm systems are advanced, portable imaging tools designed to deliver real-time X-ray visualization during diagnostic and surgical procedures. Their ability to provide immediate imaging feedback plays a vital role in supporting clinical decisions, improving surgical accuracy, and enhancing patient outcomes. The rising global burden of chronic illnesses such as cardiovascular conditions, cancer, and neurological disorders is a key driver of market expansion, as these conditions often require precise imaging for diagnosis and treatment. Increasing demand for minimally invasive surgeries, coupled with advancements in imaging technology, is further boosting the need for high-performance mobile C-arm units in both developed and developing regions. Hospitals and healthcare facilities are continuously investing in these systems to ensure faster diagnostics and improved surgical efficiency, particularly in emergency settings. As healthcare infrastructure continues to modernize globally, especially in emerging markets, mobile C-arms are becoming integral to modern surgical workflows due to their portability, precision, and ease of use.

In terms of detector type, the market is segmented into image intensifier C-arms and flat panel detector (FPD) C-arms. Flat panel detector C-arms offer improved image quality, higher contrast resolution, and enhanced anatomical visualization. This makes them ideal for intricate procedures such as spinal surgeries, orthopedic trauma, and cardiovascular interventions. These detectors also offer better radiation efficiency, producing clearer images at lower doses, which enhances patient and operator safety. FPD-based systems further reduce workflow interruptions by providing a broader and more stable imaging field, limiting the need for repositioning during procedures. The shift toward flat panel detector technology is playing a crucial role in improving surgical precision and streamlining imaging processes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $2.8 Billion |

| CAGR | 5.5% |

Based on power output, the market is divided into high-powered C-arms (11kW-25kW) and low-powered C-arms (2kW-10kW). The high-powered C-arm segment accounted for USD 989.8 million in 2024, capturing 61% of the market. These high-capacity systems are preferred for complex procedures requiring deep tissue imaging and extended imaging durations. Their ability to deliver high-resolution results during demanding interventions, such as neurovascular, orthopedic, and cardiovascular surgeries, has made them essential equipment in operating rooms. Their performance under high workloads also makes them well-suited for use in larger anatomical regions, ensuring clearer visualizations during intricate procedures.

Design-wise, the market is categorized into integrated systems and separate configuration systems. Integrated mobile C-arms dominated with a 71.1% share in 2024. These systems combine all imaging components into a single compact unit, making them especially valuable in crowded or space-constrained clinical environments. Their all-in-one design simplifies operation, reduces setup time, and improves workflow efficiency. The convenience of integrated systems is especially useful in high-pressure medical environments such as emergency departments and ICUs, where rapid imaging access is essential.

By application, the mobile C-arm market covers orthopedics and trauma, neurology, cardiology, gastroenterology, dental, oncology, and other uses. The orthopedics and trauma segment led the market in 2024 with USD 352.3 million in revenue. The increasing volume of accident-related injuries and age-related bone disorders has elevated the demand for real-time intraoperative imaging. Mobile C-arms offer accurate visualization of bone alignment and implant placement, significantly enhancing surgical outcomes and minimizing complications. Technological advancements, such as real-time 3D imaging and radiation dose control, are further supporting the use of these systems in orthopedic care.

Based on end use, the market is segmented into hospitals, diagnostic centers, and other healthcare settings. Hospitals led the market with USD 818.7 million in revenue in 2024. Their wide service offerings and high patient throughput necessitate reliable, high-performance imaging systems. Mobile C-arms in hospitals are used across various specialties including orthopedics, urology, and cardiovascular care. The growing number of hospitals, especially in urban areas, directly contributes to increasing equipment demand. Additionally, the availability of trained professionals in hospitals enhances the safe and effective use of mobile C-arm systems, encouraging higher adoption rates.

Regionally, North America dominated the market with USD 563.7 million in 2024 and is projected to reach USD 934.3 million by 2034. The United States contributed the majority share, recording USD 497.5 million in 2024. The growing incidence of chronic conditions requiring surgical interventions is pushing hospitals and clinics in the region to invest in state-of-the-art imaging technology. The strong presence of key industry players and the availability of advanced healthcare infrastructure further drive market growth in the region.

The mobile C-arm market is highly competitive, with the top four players accounting for nearly 45% of the global share. Key companies include GE HealthCare Technologies, Siemens Healthineers, Koninklijke Philips, and Ziehm Imaging. These firms maintain market dominance through continuous innovation, strong global distribution, and strategic regulatory planning. Collaborations with research institutions and public health organizations also support their efforts in bringing next-generation imaging solutions to the market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing number of surgical procedures

- 3.2.1.2 Rising prevalence of chronic diseases

- 3.2.1.3 Technological advancements of mobile C-arm machines

- 3.2.1.4 Rising demand for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with mobile C-arm machines

- 3.2.2.2 Dearth of skilled healthcare professionals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of Manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to Consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of Manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Detector Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Flat panel detector (FPD) C-arms

- 5.2.1 Type

- 5.2.1.1 Amorphous silicon (a-Si) detectors

- 5.2.1.2 Indium gallium zinc oxide (IGZO) detectors

- 5.2.1.3 Complementary metal-oxide semiconductor (CMOS) detectors

- 5.2.2 Size

- 5.2.2.1 20 cm × 20 cm

- 5.2.2.2 26 cm × 26 cm

- 5.2.2.3 30 cm x 30 cm

- 5.2.2.4 Other sizes

- 5.2.1 Type

- 5.3 Image intensifier C-arms

Chapter 6 Market Estimates and Forecast, By Power Output, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Low-powered C-arms (2kW - 10kW)

- 6.3 High-powered C-arms (11kW – 25kW)

Chapter 7 Market Estimates and Forecast, By Design Configuration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Integrated systems

- 7.3 Separate configuration systems

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Orthopedics and trauma

- 8.3 Cardiology

- 8.4 Neurology

- 8.5 Gastroenterology

- 8.6 Oncology

- 8.7 Dental

- 8.8 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Diagnostic centers

- 9.4 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Fujifilm Holdings Corporation

- 11.2 GE HealthCare Technologies

- 11.3 Genoray Co

- 11.4 Hologic

- 11.5 Koninklijke Philips

- 11.6 Nanjing Perlove Medical Equipment Co

- 11.7 Shimadzu Corporation

- 11.8 Siemens Healthineers

- 11.9 SternMed

- 11.10 Stephanix

- 11.11 Turner Imaging Systems

- 11.12 Ziehm Imaging