PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750452

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750452

Military Robot Dogs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

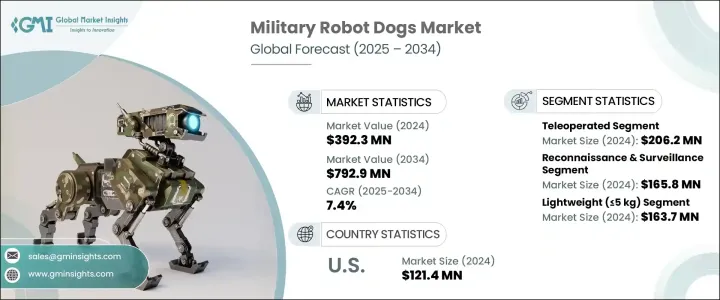

The Global Military Robot Dogs Market was valued at USD 392.3 million in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 792.9 million by 2034, driven by the increasing defense budgets worldwide and the growing demand for technologies that enhance soldier safety and force protection. The development of military robot dogs has gained significant attention, as these robots can perform critical tasks such as reconnaissance, surveillance, and explosive ordnance disposal (EOD) operations. Their ability to operate in hazardous environments, including urban ruins or chemical-biological-radiological-nuclear (CBRN) zones, offers substantial benefits to military personnel.

The market is also influenced by geopolitical factors such as trade tensions, which have led to higher production costs for certain components sourced from overseas. These disruptions have prompted manufacturers to consider reshoring production and adjusting procurement strategies. As defense contractors are under pressure to enhance their technological capabilities, military robot dog developers are focusing on autonomous solutions and mission-specific designs to meet the evolving demands of modern warfare. The growing interest in network-centric warfare has further propelled the adoption of robot dogs that can be integrated into larger military systems, allowing for real-time communication and coordination on the battlefield.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $392.3 Million |

| Forecast Value | $792.9 Million |

| CAGR | 7.4% |

Teleoperated control systems dominate the military robot dogs market, valued at USD 206.2 million in 2024. These systems provide manual control, enabling operators to remotely manage robot dogs in high-risk situations like bomb detection, hostage rescue, and other hazardous missions. This capability reduces the potential for human casualties, ensuring soldiers' safety during critical tasks. Additionally, teleoperated robot dogs are quicker and more affordable to develop compared to their fully autonomous counterparts, making them a practical solution for defense forces looking for cost-effective and reliable options. Their ability to be swiftly deployed and used in real-time operations is one of the main reasons they remain the preferred choice for military applications, particularly in environments where rapid response is essential.

In terms of functionality, the reconnaissance and surveillance segment in military robot dogs generated USD 165.8 million in 2024. These robots are equipped with cutting-edge technologies, including LiDAR, night vision, and AI-powered optics, that enhance their ability to detect and analyze potential threats in real time. Military robot dogs can spot enemy movements, IEDs, or snipers, making them invaluable in tactical operations. Their stealthy nature, due to their low noise and visual signature, makes them perfect for covert operations, where avoiding detection is paramount.

Germany Military Robot Dogs Market generated USD 22.2 million in 2024. Germany's defense modernization strategy, in line with NATO's objectives and European defense collaborations, is significantly driving the adoption of robotic systems. Military robot dogs are increasingly being used for border surveillance, cross-border operations, and rapid-response missions, as they offer enhanced mobility and versatility in challenging terrains. Germany's commitment to technological innovation and defense cooperation under programs like PESCO and the European Defence Fund (EDF) has created a favorable environment for the integration of robotic solutions in its defense operations.

Key players in the Global Military Robot Dogs Industry include Boston Dynamics, Unitree Robotics, Addverb Technologies, Ghost Robotics, and Deep Robotics. These companies are focusing on enhancing robot capabilities, integrating cutting-edge sensors, and improving reliability and durability in harsh environments. Additionally, many manufacturers are emphasizing autonomous mission-specific systems that can provide force multiplication, improve EOD operations, and support logistics tasks. By investing in R&D and collaborating with defense organizations, companies like AeroArc and Xian Supersonic Aviation Technology are strengthening their positions in the market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising military expenditures globally

- 3.3.1.2 Integration of AI and machine vision

- 3.3.1.3 Growing demand for soldier safety and force protection

- 3.3.1.4 Growth in urban warfare scenarios

- 3.3.1.5 Enhanced tactical mobility

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Cybersecurity and hacking risks

- 3.3.2.2 Battery life and endurance limitations

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Control Mode, 2021 – 2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 Teleoperated

- 5.3 Fully autonomous

- 5.4 Semi-autonomous

Chapter 6 Market Estimates and Forecast, By Payload Capacity, 2021 – 2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 Lightweight (≤5 kg)

- 6.3 Medium weight (5–10 kg)

- 6.4 Heavy duty (>10 kg)

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 Reconnaissance and surveillance

- 7.2.1 Night-time patrols

- 7.2.2 Forward observation

- 7.2.3 Stealth surveillance in hostile terrain

- 7.3 Combat Support

- 7.4 Search and rescue

- 7.5 Explosive ordnance disposal (EOD)

- 7.5.1 Mine detection

- 7.5.2 CBRN environment assessment

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Addverb Technologies

- 9.2 AeroArc

- 9.3 Boston Dynamics

- 9.4 Deep Robotics

- 9.5 Edith Defense Systems

- 9.6 Ghost Robotics

- 9.7 Svaya Robotics

- 9.8 Unitree Robotics

- 9.9 Xian Supersonic Aviation Technology