PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750471

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750471

HVAC Valve Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

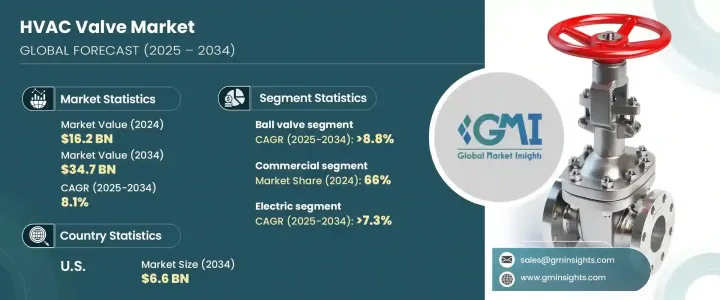

The Global HVAC Valve Market was valued at USD 16.2 billion in 2024 and is estimated to grow at a CAGR of 8.1% to reach USD 34.7 billion by 2034 driven by the surge in construction activities worldwide, leading to increased demand for heating, ventilation, and air conditioning (HVAC) systems across residential, commercial, and industrial sectors. Valves play a crucial role in these systems by regulating fluid flow, pressure, and temperature, ensuring optimal performance and energy efficiency.

The trend toward energy-efficient and smart buildings is propelling the HVAC valve market. New constructions incorporate advanced HVAC systems with intelligent valves featuring sensors, connectivity, and analytics for real-time monitoring and control. These smart valves enable facility managers to optimize energy consumption, detect faults early, and perform predictive maintenance, reducing operational costs and extending equipment lifespan. Integrating Internet of Things (IoT) technology into HVAC systems accelerates the demand for automated and intelligent valve solutions. These smart valves offer real-time monitoring, remote access, and advanced control capabilities, allowing facility managers to optimize energy usage and improve system responsiveness. As commercial and industrial buildings increasingly adopt smart building frameworks, the need for valves that seamlessly communicate with Building Management Systems (BMS) is rising.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.2 Billion |

| Forecast Value | $34.7 Billion |

| CAGR | 8.1% |

In 2024, ball valves held a significant share of the HVAC valve market, accounting for 4.3%. Their popularity is attributed to their simple structure, tight shut-off action, and suitability for airflow and fluid flow management in HVAC systems. Ball valves are widely used in new installations and retrofitting projects due to their low torque operation, close seal, and high durability, which contribute to the efficiency and asepsis of heating and cooling applications. Additionally, ball valves support automation technologies, making them compatible with smart HVAC systems.

The commercial sector dominated the HVAC valve market in 2024, representing a 66% share. Commercial buildings such as offices, shopping malls, hospitals, hotels, data centers, and schools require complex HVAC systems to regulate fluid and air flow accurately. The adoption of smart and energy-efficient HVAC systems in these buildings is driven by the need to comply with government standards, reduce costs, and achieve green certifications like LEED. This trend fuels the demand for advanced HVAC valves that offer precise control and integration with building management systems.

United States HVAC Valve Market held a 67% share in 2024 and is projected to generate USD 6.6 billion by 2034, driven by stringent energy efficiency regulations and sustainability initiatives, such as the Energy Star program and Canada's Energy Efficiency Regulations. These regulations are encouraging the adoption of efficient HVAC systems, including intelligent and IoT-based valves, to conserve energy and comply with environmental standards. The focus on smart buildings and automation in the region further supports the demand for Building Management System (BMS)-compatible HVAC valves. Additionally, the retrofitting of existing HVAC systems in older buildings is contributing to the increased demand for advanced valve solutions.

Key players in the Global HVAC Valve Industry include Honeywell, Johnson Controls, Schneider Electric, Siemens, Belimo, Danfoss, Pentair, AVK, Flowserve, Mueller Industries, Samson, Taco, Bray, Nexus, and IDC. These companies focus on product innovation, strategic partnerships, and mergers and acquisitions to strengthen their market presence. Developing advanced HVAC valves with smart features and enhanced performance is a key focus area for leading manufacturers. Additionally, companies are investing in research and development to develop eco-friendly and energy-efficient solutions to meet the growing demand for sustainable HVAC systems.

To strengthen their market presence, companies in the HVAC valve industry are adopting several key strategies. These include expanding their product portfolios through innovation and technological advancements, such as introducing new valve designs and features to cater to the evolving needs of customers. Integrating smart technologies, such as IoT and automation, is a significant trend in the market, enabling manufacturers to offer advanced solutions with real-time monitoring and control capabilities. Strategic partnerships and collaborations with technology providers, HVAC system manufacturers, and distributors enable companies to enhance their product offerings and reach a broader customer base. Additionally, mergers and acquisitions are common strategies for market consolidation and gaining access to new markets and technologies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Manufacturers

- 3.2.2 Raw material suppliers

- 3.2.3 Distribution channel

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact on forces

- 3.8.1 Growth drivers

- 3.8.1.1 Growing construction industry

- 3.8.1.2 Urbanization and smart city initiatives

- 3.8.1.3 Climate change and weather extremes

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High initial costs

- 3.8.2.2 Limited awareness in emerging markets

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Industry structure and concentration

- 4.2.1 Competitive intensity assessment

- 4.2.2 Company market share analysis

- 4.2.3 Competitive positioning matrix

- 4.3 Product positioning

- 4.3.1 Price-performance positioning

- 4.3.2 Geographic presence

- 4.3.3 Innovation capabilities

- 4.4 Strategic dashboard

- 4.5 Competitive benchmarking

- 4.5.1 Manufacturing capabilities

- 4.5.2 Product portfolio strength

- 4.5.3 Distribution network

- 4.5.4 R&D investments

- 4.6 Strategic initiatives assessment

- 4.7 SWOT analysis of key players

- 4.8 Future competitive outlook

Chapter 5 Market Estimates & Forecast, By Valve Type, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Ball valves

- 5.3 Globe valves

- 5.4 Butterfly valves

- 5.5 Check valves

- 5.6 Gate valves

- 5.7 Pressure relief valves

- 5.8 Control valves

- 5.9 Solenoid valves

- 5.10 Others

Chapter 6 Market Estimates & Forecast, By Operation Type, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Pneumatic

- 6.4 Hydraulic

- 6.5 Electric

- 6.6 Smart/connected

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Heating systems

- 7.3 Cooling systems

- 7.4 Ventilation systems

- 7.5 district cooling

- 7.6 Refrigeration

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Office buildings

- 8.3.2 Retail

- 8.3.3 hospitality

- 8.3.4 Healthcare

- 8.3.5 Educational institute

- 8.3.6 Others

- 8.4 Industrial

- 8.4.1 Oil and gas

- 8.4.2 Manufacturing

- 8.4.3 Food and beverage

- 8.4.4 Pharmaceuticals

- 8.4.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 AVK

- 10.2 Belimo

- 10.3 Bray

- 10.4 Danfoss

- 10.5 Flowserve

- 10.6 Honeywell

- 10.7 IDC

- 10.8 Johnson Controls

- 10.9 Mueller Industries

- 10.10 Nexus

- 10.11 Pentair

- 10.12 Samson

- 10.13 Schneider Electric

- 10.14 Siemens