PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750510

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750510

Intelligent Process Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

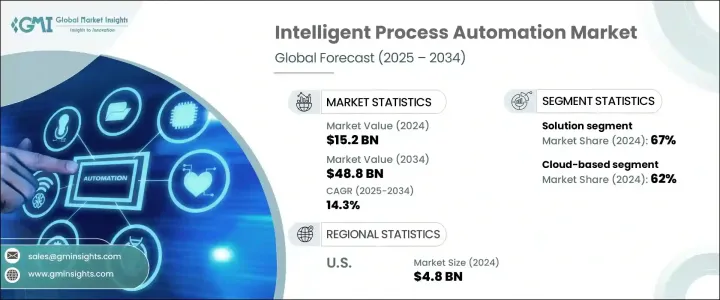

The Global Intelligent Process Automation (IPA) Market was valued at USD 15.2 billion in 2024 and is estimated to grow at a CAGR of 14.3% to reach USD 48.8 billion by 2034. This rapid growth is largely fueled by the increasing adoption of digital transformation across industries and the rising need for advanced technologies like artificial intelligence and machine learning to optimize business operations. Companies are under pressure to enhance operational efficiency, cut costs, and deliver better customer experiences-all of which are accelerating the shift toward intelligent automation. IPA solutions are enabling organizations to eliminate manual, repetitive tasks and improve decision-making through data-driven insights. As more businesses embrace automation, the demand for scalable and adaptive technologies continues to surge. The market is benefiting from the convergence of various cognitive technologies, allowing businesses to rethink their workflows for greater agility, innovation, and performance. Increasing deployment of IPA tools across sectors highlights a broader trend where automation is no longer viewed solely as a cost-cutting mechanism but as a key enabler of competitive advantage and digital resilience.

One of the major growth drivers for IPA is the integration of artificial intelligence components that support real-time data processing, pattern recognition, and continuous learning. With AI capabilities, IPA platforms can adapt to changing business needs, analyze unstructured data, and make predictive decisions. Organizations are turning to these tools to increase transparency, reduce human error, and streamline high-volume operations. The push toward automation is also being bolstered by the growing availability of cloud-based solutions and low-code/no-code development platforms, making IPA more accessible and easier to implement across diverse business environments. These innovations are helping companies break down silos and address challenges associated with legacy systems and fragmented data landscapes. As a result, intelligent automation is becoming increasingly embedded in core business functions, supporting everything from compliance monitoring to customer engagement, all while contributing to sustainability efforts by reducing paper usage and energy consumption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.2 Billion |

| Forecast Value | $48.8 Billion |

| CAGR | 14.3% |

In terms of components, the IPA market is segmented into solutions and services. The solutions segment held a dominant share of approximately 67% in 2024 and is anticipated to grow at a CAGR exceeding 15% throughout the forecast period. These platforms appeal to a wide range of industries due to their balance of advanced features and ease of deployment. By incorporating AI, machine learning, and robotic process automation, IPA solutions can automate both back-office and front-end workflows efficiently. Their ability to enhance compliance, scale across functions, and reduce dependency on manual processes makes them a preferred choice for enterprises seeking stable, intelligent automation systems. From document processing to customer interaction management, these solutions enable error reduction, improve data accuracy, and support continuous process improvement.

Based on deployment, the market is categorized into cloud-based and on-premises models. Cloud-based IPA held the majority share of 62% in 2024 and is projected to expand at a CAGR of over 14.9% from 2025 to 2034. These platforms offer key advantages such as faster implementation, better integration capabilities, and remote accessibility, making them ideal for businesses undergoing digital transformation. Their centralized infrastructure and compatibility with SaaS applications allow companies to automate processes seamlessly across different departments and geographies. Both small and large organizations are increasingly opting for cloud deployment to speed up automation efforts in areas like compliance, onboarding, and transactional processing.

By technology, the market is segmented into machine learning (ML), natural language processing (NLP), robotic process automation (RPA), computer vision, virtual agents, and others. Machine learning leads the segment due to its transformative role in enhancing the adaptability and intelligence of automation platforms. ML allows systems to learn from data, detect trends, and make decisions without manual programming. It is widely used for applications that require predictive insights and the ability to manage complex or unstructured datasets. The growing reliance on machine learning underscores its importance in driving the evolution of IPA from static rule-based systems to dynamic, learning-enabled solutions that support strategic business goals.

Regionally, the United States dominated the North American market in 2024, capturing around 84.4% of the regional revenue and generating close to USD 4.8 billion. The country's leadership in digital innovation, combined with strong enterprise adoption of AI-powered technologies, continues to position it at the forefront of intelligent automation. The U.S. market benefits from a mature IT infrastructure, substantial investment in automation technologies, and a high concentration of major software vendors. With digital transformation being a top priority across industries, the demand for agile, intelligent, and scalable automation platforms is expected to remain strong throughout the forecast period.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Technology providers

- 3.2.2 System integrators

- 3.2.3 Cloud and infrastructure providers

- 3.2.4 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Use cases

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rapid digital transformation

- 3.10.1.2 Integration of AI and machine learning in business processes

- 3.10.1.3 Growing adoption of Robotic Process Automation (RPA)

- 3.10.1.4 Cloud adoption and SaaS expansion

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High implementation costs

- 3.10.2.2 Data privacy and security concerns

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Solution

- 5.3 Services

- 5.3.1 Professional services

- 5.3.2 Managed services

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Cloud-based

- 6.3 On-premises

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Machine Learning (ML)

- 7.3 Natural Language Processing (NLP)

- 7.4 Robotic Process Automation (RPA)

- 7.5 Computer vision

- 7.6 Virtual agents

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Large enterprise

- 8.3 SME

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 Business process automation

- 9.3 IT operations

- 9.4 Application management

- 9.5 Content management

- 9.6 Security management

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 BFSI

- 10.3 Healthcare

- 10.4 Retail

- 10.5 IT & telecom

- 10.6 Communication and media & education

- 10.7 Manufacturing

- 10.8 Logistics, energy & utilities

- 10.9 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 AntWorks

- 12.2 Appian

- 12.3 Automation Anywhere

- 12.4 Blue Prism

- 12.5 Cognizant Technology Solutions

- 12.6 HCLTech

- 12.7 HelpSystems

- 12.8 IBM

- 12.9 Infosys

- 12.10 Kofax

- 12.11 Microsoft

- 12.12 NICE

- 12.13 Oracle Corporation

- 12.14 Pegasystems

- 12.15 Salesforce

- 12.16 SAP SE

- 12.17 Tata Consultancy Services (TCS)

- 12.18 UiPath

- 12.19 Wipro

- 12.20 WorkFusion