PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750515

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1750515

Transcatheter Embolization And Occlusion Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

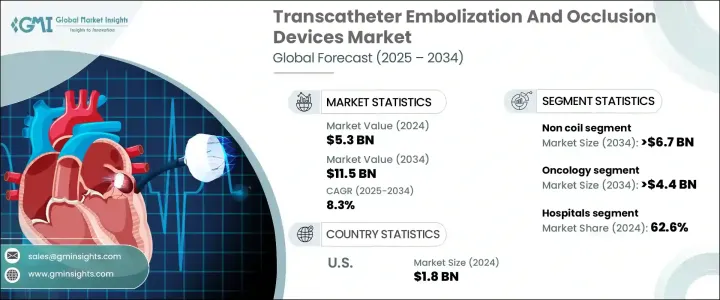

The Global Transcatheter Embolization And Occlusion Devices Market was valued at USD 5.3 billion in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 11.5 billion by 2034, driven by several factors, including the increasing prevalence of chronic diseases such as cancer, complicated pregnancies, vascular malformations, and hemorrhagic disorders like hemophilia, all of which require specialized medical attention. Additionally, the aging global population is leading to a higher demand for quality-of-life procedures that reduce the invasiveness of surgery and shorten hospital stays, making TEO devices favorable to both physicians and patients.

The rise in cases of liver cancer and hepatocellular carcinoma, particularly in the Asia Pacific region, has led to an increased use of embolization therapies like transarterial chemoembolization (TACE). Advancements in catheter technology, medical imaging, and biocompatible materials have improved the safety and accuracy of these procedures, encouraging more widespread adoption. Additionally, the rising awareness about minimally invasive treatment options has made uterine fibroid embolization (UFE) a popular choice among women seeking alternatives to traditional surgical procedures. Unlike hysterectomy, UFE preserves the uterus, reduces recovery time, and minimizes hospital stays, making it a more attractive and patient-friendly solution. This shift in patient preference is encouraging more gynecologists and interventional radiologists to recommend embolization techniques, which is, in turn, boosting the adoption of transcatheter embolization devices.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.3 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 8.3% |

The market is segmented by device type into non-coil and coil categories. The non-coil segment is expected to grow at a CAGR of 8.6%, reaching USD 6.7 billion by 2034, attributed to the adoption of new embolic agents like microspheres and liquid embolics, along with plugs that offer superior control during occlusion compared to traditional coil-based devices. Non-coil solutions are particularly preferred in targeted embolization procedures used in treating liver cancer, arteriovenous malformations, gastrointestinal bleeding, and uterine fibroids. Their ability to navigate complex vascular anatomies with consistent results has made them increasingly favored by interventional radiologists.

In terms of application, the oncology segment is expected to drive business growth, expanding at a CAGR of 8.8%, reaching USD 4.4 billion by 2034, fueled by the increasing global burden of cancer, especially liver, kidney, and lung cancers, which often require more localized and less invasive treatment options. There has been significant growth in the adoption of transarterial chemoembolization (TACE) and radioembolization as vital interventional oncology procedures. The growing caseload of hepatocellular carcinoma, predominantly in the Asia Pacific and Latin America regions, is witnessing greater use of embolization therapies.

U.S. Transcatheter Embolization And Occlusion Devices Market accounted for USD 1.8 billion in 2024 and is anticipated to grow at a CAGR of 7.4% between 2025 to 2034. Demand for embolization therapeutic devices is greatly influenced by widespread health issues such as cancer, gastrointestinal bleeding, aneurysms, and uterine fibroids, which are optimally treated using minimally invasive embolization therapies. The country's dominant healthcare spending, along with its sophisticated healthcare infrastructure, facilitates the adoption of new TEO procedures. Furthermore, the increasing availability of leading market manufacturers and a surge in FDA approvals for new and efficient embolic agents and delivery systems fuel market growth.

Prominent players operating in the Global Transcatheter Embolization And Occlusion Devices Industry include Abbott, Acandis, Balt, Boston Scientific, COOK MEDICAL, Edwards Lifesciences, Johnson & Johnson, LEPU MEDICAL, Medtronic, Merit Medical, MicroVention, Penumbra, Shape Memory Medical, SIRTEX, Stryker, and TERUMO. To strengthen their market position, companies in the transcatheter embolization and occlusion devices market are focusing on several key strategies. These include investing in research and development to create innovative products that meet the evolving needs of healthcare providers and patients. Strategic partnerships and collaborations with hospitals and healthcare institutions are being pursued to enhance product adoption and expand market reach. Additionally, companies are focusing on expanding their product portfolios to cater to a wider range of medical conditions and applications.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shift toward minimally invasive procedures

- 3.2.1.2 Increasing interventional radiology capabilities

- 3.2.1.3 Rising prevalence of chronic diseases

- 3.2.1.4 Technological advancements in embolic materials

- 3.2.1.5 Increased incidence of traumatic injuries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices and procedures

- 3.2.2.2 Risk of non-target embolization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise Response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technology landscape

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Device Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Non coil

- 5.2.1 Flow diverting devices

- 5.2.2 Embolization particles

- 5.2.3 Liquid embolics

- 5.2.4 Other non-coil device types

- 5.3 Coils

- 5.3.1 Pushable coils

- 5.3.2 Detachable coils

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oncology

- 6.3 Peripheral vascular disease

- 6.4 Neurology

- 6.5 Urology

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 acandis

- 9.3 balt

- 9.4 Boston Scientific

- 9.5 COOK MEDICAL

- 9.6 Edwards Lifesciences

- 9.7 Johnson & Johnson

- 9.8 LEPU MEDICAL

- 9.9 Medtronic

- 9.10 Merit Medical

- 9.11 MicroVention

- 9.12 Penumbra

- 9.13 shape memory medical

- 9.14 SIRTEX

- 9.15 stryker

- 9.16 TERUMO