PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1755248

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1755248

Fluorinated Coating Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

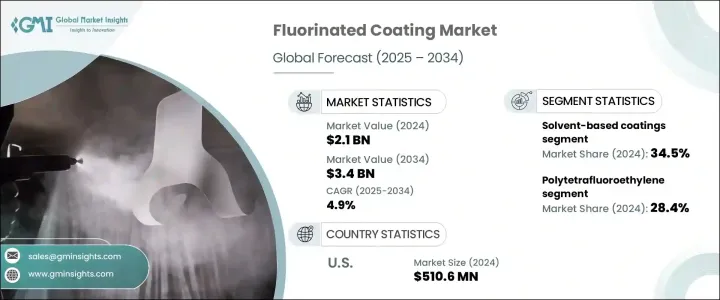

The Global Fluorinated Coating Market was valued at USD 2.1 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 3.4 billion by 2034. These coatings are primarily formulated using fluoropolymer materials that offer outstanding durability, thermal stability, and resistance to chemicals and corrosion. These properties make them vital for industries that demand long-lasting, high-performance coatings across various operational environments. From extreme temperatures to chemically reactive surroundings, fluorinated coatings continue to demonstrate strong performance, particularly in regions prone to high humidity and environmental stress.

As the demand for advanced materials capable of resisting environmental degradation grows, these coatings are seeing increased adoption across sectors that prioritize efficiency and longevity in materials. Moreover, investments in transportation and civil infrastructure have led to greater use of protective coatings designed to increase the service life of key assets while also reducing long-term maintenance costs. Technological innovations, regulatory shifts toward sustainability, and the push for lower environmental impact are encouraging manufacturers to adopt eco-conscious coating solutions, including water-based and UV-curable alternatives.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 Billion |

| Forecast Value | $3.4 Billion |

| CAGR | 4.9% |

In terms of product type, polytetrafluoroethylene (PTFE) accounted for over 28.4% of the global market in 2024. Known for its low surface energy and non-reactive nature, PTFE has become a staple material for applications that require minimal friction, thermal endurance, and strong chemical resistance. Its utility spans a broad spectrum of end-use sectors where exposure to extreme temperatures and corrosive agents is common. PTFE is widely used in manufacturing processes due to its stable behavior under stress, making it ideal for components exposed to mechanical wear or chemical exposure.

When categorized by technology, solvent-based coatings captured nearly 34.5% of the market share in 2024. Their long-standing dominance is attributed to superior adhesion, extended service life, and resilience in tough operating conditions. These coatings perform reliably under aggressive environments, which explains their widespread use in sectors involving high mechanical and thermal loads. Despite regulatory pressure around volatile organic compound (VOC) emissions, solvent-based coatings continue to maintain a solid presence due to their industrial advantages. However, rising interest in eco-friendly solutions is gradually shifting the industry landscape. Waterborne coatings are gaining traction, especially in regions enforcing stricter emission norms, while UV-curable coatings are becoming increasingly viable in precision manufacturing thanks to their rapid curing and low energy requirements.

Based on substrate, metal held the leading position in the global market in 2024. Metals are extensively used in manufacturing, and their exposure to weather, chemicals, and heat makes them suitable candidates for fluorinated coatings. These coatings provide a barrier against corrosion and oxidation, making them essential for extending the life of structural components and equipment. Other substrates such as plastics, composites, and concrete are also witnessing growing demand, particularly in infrastructure projects requiring weather-resistant finishes.

Regarding performance attributes, chemical resistance led the market in 2024. Many industrial sectors handle aggressive chemicals, and equipment used in these settings must be coated to withstand such exposure. Fluorinated coatings are preferred because they prevent surface degradation, equipment failure, and contamination risks. Their ability to act as reliable linings for tanks, pipelines, and processing equipment ensures uninterrupted operation and safety. Properties like thermal stability, electrical insulation, and low-friction surfaces also contribute significantly to their adoption, particularly in high-precision and high-performance applications.

By application, the aerospace and defense segment emerged as the dominant category in 2024. These industries require materials that can endure extreme environments, and fluorinated coatings meet that demand by offering heat resistance, lightweight performance, and long-term protection. Meanwhile, industrial equipment claimed the largest share of the market due to the widespread use of coatings in machinery exposed to corrosive substances and elevated temperatures. The food-related segment also remains strong as demand for non-stick, easy-clean surfaces grows in commercial and residential applications.

In regional analysis, the United States fluorinated coating market surpassed USD 510.6 million in 2024. The country continues to lead in North America, backed by a well-established industrial base, steady technological advancements, and an ongoing focus on product performance. The need for high-quality, durable coatings is further amplified by the continuous development of infrastructure and manufacturing sectors. Consumer trends favoring easy-maintenance materials also support growth in household and outdoor product applications.

The market remains moderately consolidated, with several key players commanding significant shares. Competitive focus revolves around product innovation, regulatory compliance, and customized solutions tailored for specific industries. Leading companies are consistently enhancing surface protection capabilities and expanding their reach across high-growth application areas.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

Note: the above trade statistics will be provided for key countries only.

- 3.4 Impact forces

- 3.4.1 Market drivers

- 3.4.2 Market restraints

- 3.4.3 Market opportunities

- 3.4.4 market challenges

- 3.5 Product overview

- 3.5.1 Fluoropolymer chemistry & structure

- 3.5.2 Performance characteristics

- 3.5.3 Chemical resistance properties

- 3.5.4 Thermal stability

- 3.5.5 Non-stick & low friction properties

- 3.5.6 Weather resistance & durability

- 3.5.7 Comparison with other coating technologies

- 3.6 Manufacturing process analysis

- 3.6.1 Resin production

- 3.6.2 Formulation techniques

- 3.6.3 Application methods

- 3.6.4 Curing processes

- 3.6.5 Quality control procedures

- 3.7 Regulatory landscape

- 3.8 Growth potential analysis

- 3.9 Pricing analysis (USD/Tons) 2021-2034

- 3.10 Sustainability & environmental impact assessment

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Market share analysis

- 4.2 Strategic framework

- 4.2.1 Mergers & acquisitions

- 4.2.2 Joint ventures & collaborations

- 4.2.3 New product developments

- 4.2.4 Expansion strategies

- 4.3 Competitive benchmarking

- 4.4 Vendor landscape

- 4.5 Competitive positioning matrix

- 4.6 Strategic dashboard

- 4.7 Patent analysis & innovation assessment

- 4.8 Market entry strategies for new players

- 4.9 Distribution network analysis

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polytetrafluoroethylene

- 5.2.1 Pure PTFE coatings

- 5.2.2 PTFE-based composite coatings

- 5.2.3 Modified PTFE coatings

- 5.3 Polyvinylidene fluoride

- 5.3.1 PVDF homopolymer coatings

- 5.3.2 PVDF copolymer coatings

- 5.3.3 Modified PVDF coatings

- 5.4 Fluorinated ethylene propylene

- 5.5 Perfluoroalkoxy alkane

- 5.6 Ethylene tetrafluoroethylene

- 5.7 Ethylene chlorotrifluoroethylene

- 5.8 Polychlorotrifluoroethylene

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solvent-based coatings

- 6.3 Water-based coatings

- 6.4 Powder coatings

- 6.5 UV-curable coatings

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Substrate, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Metal

- 7.2.1 Steel

- 7.2.2 Aluminum

- 7.2.3 Others

- 7.3 Plastic & composites

- 7.4 Glass

- 7.5 Concrete & masonry

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Performance Attribute, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Chemical resistance

- 8.3 Weather resistance

- 8.4 Non-stick/low friction

- 8.5 Thermal stability

- 8.6 Electrical insulation

- 8.7 Corrosion protection

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Industrial equipment

- 9.2.1 Chemical processing equipment

- 9.2.2 Oil & gas equipment

- 9.2.3 Food processing equipment

- 9.2.4 Pharmaceutical equipment

- 9.2.5 Others

- 9.3 Building & construction

- 9.3.1 Architectural coatings

- 9.3.2 Roofing materials

- 9.3.3 Facades & cladding

- 9.3.4 Others

- 9.4 Automotive & transportation

- 9.4.1 Exterior components

- 9.4.2 Interior components

- 9.4.3 Under-the-hood applications

- 9.4.4 Others

- 9.5 Cookware & food contact

- 9.5.1 Non-Stick cookware

- 9.5.2 Bakeware

- 9.5.3 Food processing equipment

- 9.5.4 Others

- 9.6 Electronics & electrical

- 9.6.1 PCB coatings

- 9.6.2 Wire & cable coatings

- 9.6.3 Semiconductor applications

- 9.6.4 Others

- 9.7 Aerospace & defense

- 9.8 Marine

- 9.9 Healthcare & medical

- 9.10 Others

Chapter 10 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 Industrial manufacturing

- 10.2.1 Chemical

- 10.2.2 Oil & gas

- 10.2.3 Power generation

- 10.2.4 Others

- 10.3 Building & construction

- 10.4 Automotive & transportation

- 10.5 Consumer goods

- 10.5.1 Cookware & kitchenware

- 10.5.2 Appliances

- 10.5.3 Others

- 10.6 Electronics & semiconductors

- 10.7 Aerospace & defense

- 10.8 Food & beverage

- 10.9 Healthcare & pharmaceutical

- 10.10 Others

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 3M Company

- 12.2 AFT Fluorotec

- 12.3 AGC Chemicals Americas

- 12.4 AGC Inc.

- 12.5 AkzoNobel N.V.

- 12.6 Arkema

- 12.7 Beckers Group

- 12.8 Daikin Industries

- 12.9 Dow

- 12.10 DuPont

- 12.11 Fluorotherm Polymers

- 12.12 Gujarat Fluorochemicals

- 12.13 Jotun A/S

- 12.14 Nippon Paint Holdings

- 12.15 PPG Industries, Inc.

- 12.16 Sherwin-Williams Company

- 12.17 Solvay S.A.

- 12.18 The Chemours Company

- 12.19 Whitford Corporation