PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1755251

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1755251

Optical Satellite Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

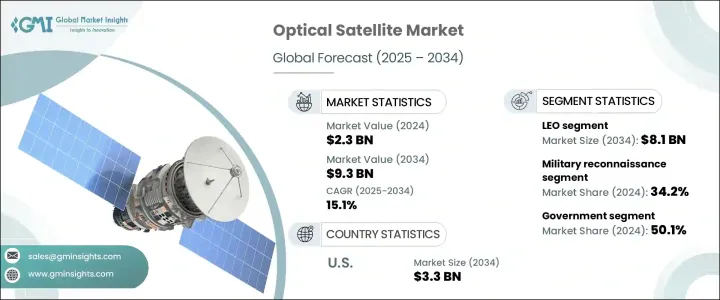

The Global Optical Satellite Market was valued at USD 2.3 billion in 2024 and is estimated to grow at a CAGR of 15.1% to reach USD 9.3 billion by 2034, driven by increasing demand for commercial satellite services, particularly for Earth observation and surveillance applications. As optical satellites become more prevalent in orbit, manufacturers are facing new hurdles tied to escalating production costs. Recent tariff policies have created cost pressures on critical components such as semiconductors, precision optical sensors, and aerospace-grade materials, forcing many manufacturers to pivot toward domestic sourcing. This shift has resulted in rising capital expenditure and extended project timelines, adding strain to companies already managing complex satellite production cycles. Additionally, persistent supply chain disruptions are causing delays and budget overruns, presenting a challenge for consistent output.

Heightened demand for high-resolution Earth Observation (EO) imagery is rapidly transforming the operational landscape of the satellite and space industry. Both commercial and public sectors now rely heavily on high-detail optical imaging for applications like environmental monitoring, infrastructure development, disaster management, and agricultural analysis. Precision farming has especially benefited from these capabilities, with satellites offering actionable insights on soil health, crop growth, and land use through multispectral imaging. These satellites allow for nearly real-time data delivery, improving the accuracy and efficiency of agricultural operations and further fueling adoption across global agritech markets. Enhanced imaging capabilities combined with quick turnaround times for actionable data continue to push the demand for optical satellite deployment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $9.3 Billion |

| CAGR | 15.1% |

The Low Earth Orbit (LEO) segment is poised to reach USD 8.1 billion by 2034. Its proximity to Earth makes LEO a preferred orbit for deploying optical satellites, especially for missions requiring high-resolution surface imaging. Government-backed initiatives integrated with private sector capabilities to support targeted satellite deployments. These collaborations gather detailed imagery for terrain analysis, climate modeling, and strategic intelligence, reinforcing the LEO segment's influence on market expansion.

The crop monitoring application is expected to hit USD 2.3 billion by 2034, backed by the rising importance of accurate agricultural diagnostics. Optical satellites are instrumental in detecting early signs of crop stress using multispectral imaging to prevent yield loss. The growth in precision agriculture, combined with advancements in digital farming, continues to boost demand for EO-enabled solutions that deliver real-time insights and help optimize land management strategies.

UK Optical Satellite Market is anticipated to grow at a CAGR of 14.1% through 2034. Ongoing investment in Earth observation technologies by the UK government has opened new opportunities for satellite-based monitoring. There's increasing national demand for high-quality imaging solutions used for tracking environmental changes, enhancing surveillance systems, and informing policies around climate resilience and sustainability.

Leading players in the Global Optical Satellite Market include Lockheed Martin Corporation, Airbus, Thales Alenia Space, and Maxar Technologies. These companies are implementing strategic measures to maintain and grow their market presence. A major focus lies in expanding satellite fleets and enhancing image resolution capabilities through advanced optics. They invest in collaborative programs with government agencies and private space firms to secure long-term contracts and co-develop next-generation systems. Significant R&D spending, localized sourcing of components, and efforts to streamline manufacturing are helping address rising material costs and production challenges. In addition, many players are enhancing their software platforms to support faster image processing and analytics integration delivering greater value to end-users.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.3 Trump administration tariffs analysis

- 3.3.1 Impact on trade

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.1.3 Impact on the industry

- 3.3.1.3.1 Supply-side impact (raw material)

- 3.3.1.3.1.1 Price volatility

- 3.3.1.3.1.2 Supply chain restructuring

- 3.3.1.3.1.3 Production cost implications

- 3.3.1.3.2 Demand-side impact

- 3.3.1.3.2.1 Price transmission to end markets

- 3.3.1.3.2.2 Market share dynamics

- 3.3.1.3.2.3 Consumer response patterns

- 3.3.1.3.1 Supply-side impact (raw material)

- 3.3.1.4 Key companies impacted

- 3.3.1.5 Strategic industry responses

- 3.3.1.5.1 Supply chain reconfiguration

- 3.3.1.5.2 Pricing and product strategies

- 3.3.1.5.3 Policy engagement

- 3.3.1.5.4 Outlook and future considerations

- 3.3.2 Growth drivers

- 3.3.2.1 Rising demand for high-resolution earth observation data

- 3.3.2.2 Increased investments in national security and surveillance

- 3.3.2.3 Rapid growth of commercial satellite

- 3.3.2.4 Technological advancements in imaging and data processing

- 3.3.2.5 Growing climate change monitoring and environmental protection initiatives

- 3.3.3 Industry pitfalls and challenges

- 3.3.3.1 High capital and operational costs

- 3.3.3.2 Data overload and processing complexity

- 3.3.1 Impact on trade

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Orbit Type, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 LEO

- 5.3 MEO

- 5.4 GEO

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Military reconnaissance

- 6.3 Crop monitoring

- 6.4 Urban planning

- 6.5 Disaster management

- 6.6 Mineral mapping

- 6.7 Environmental monitoring

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Government

- 7.3 Commercial

- 7.4 Academic

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Airbus

- 9.2 China Aerospace Science and Technology Corp.

- 9.3 Elbit Systems

- 9.4 Hanwha Group

- 9.5 Israeli Aerospace Industry

- 9.6 ISRO

- 9.7 Lockheed Martin Corporation

- 9.8 Maxar Technologies

- 9.9 Mitsubishi Electric Corporation

- 9.10 OHB SE

- 9.11 Satellogic

- 9.12 Surrey Satellite Technology Ltd

- 9.13 Thales Alenia Space

- 9.14 Turksat