PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1755273

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1755273

Aircraft Seals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

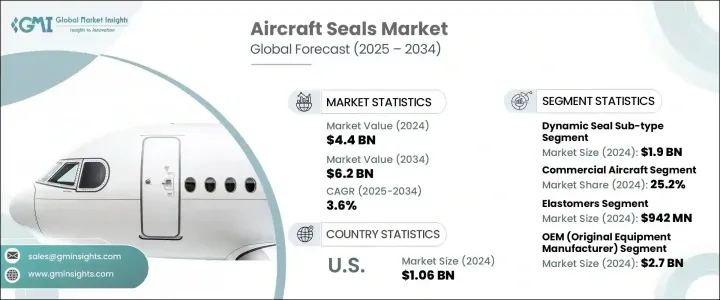

The Global Aircraft Seals Market was valued at USD 4.4 billion in 2024 and is estimated to grow at a CAGR of 3.6% to reach USD 6.2 billion by 2034, driven by the growing global demand for air travel, particularly across emerging aviation markets in Asia-Pacific. This increased air traffic has prompted airline operators to invest in new aircraft, directly boosting demand for advanced sealing technologies. Aircraft manufacturers are under rising pressure to enhance fuel efficiency and reduce carbon emissions, creating a strong need for lightweight, high-performance seals. As a result, manufacturers are shifting toward advanced materials such as high-grade elastomers and composites.

Additionally, changing geopolitical dynamics and tariff regulations have altered supply chain strategies. Rising material costs due to trade tensions have pushed aerospace suppliers to pivot toward localized sourcing and restructure procurement processes to mitigate exposure. These shifts are reinforcing efforts to develop seals that not only meet performance standards but also support sustainability and long-term operational efficiency. Technological advancements in elastomeric materials and the development of seals with enhanced temperature and pressure resistance are further shaping the trajectory of the aircraft seals market across both commercial and defense segments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.4 billion |

| Forecast Value | $6.2 billion |

| CAGR | 3.6% |

Dynamic seals led the market in 2024 with a valuation of USD 1.9 billion. Their critical role in components subject to movement and pressure, such as engine assemblies, flight control systems, and landing gear, makes them indispensable in modern aircraft engineering. The dynamic seal segment holds the largest share due to ongoing innovation in elastomer blends that can endure extreme conditions without compromising functionality.

Among aircraft types, the commercial aircraft segment accounted for a 25.2% share in 2024. This dominance is attributed to a rising number of airline operators expanding their fleets to meet passenger traffic demand and to maintain performance standards during regular maintenance cycles. Seals are essential in critical systems such as engines, environmental controls, and fuselage integration, which require long-lasting and reliable components.

U.S. Aircraft Seals Market was valued at USD 1.06 billion in 2024. The country remains a vital contributor to the global market due to its strong aerospace base. The presence of leading OEMs like Lockheed Martin, Raytheon, and Boeing fuels a consistent and high-volume demand for premium sealing solutions. These firms prioritize precision components that minimize unexpected maintenance and improve aircraft reliability across commercial, defense, and space applications. The advanced R&D ecosystem and stringent regulatory standards in the U.S. also drive innovation in sealing technologies.

Key players leading the Global Aircraft Seals Market include Trelleborg Sealing Solutions, Parker Hannifin Corporation, and SKF Group. Major companies focus on expanding their product portfolios through material innovation and precision manufacturing techniques. Strategic collaborations with aerospace OEMs enable suppliers to co-develop customized sealing solutions tailored to next-gen aircraft designs. Many invest heavily in R&D to enhance seal performance in extreme temperature and pressure environments. Expansion into emerging markets and localization of manufacturing are helping reduce logistical costs and improve customer proximity. Additionally, companies enhance their aftermarket services to capture value across the aircraft lifecycle, ensuring long-term revenue through maintenance and upgrades.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Expansion of global aircraft fleet

- 3.7.1.2 Advancements in aircraft design and materials

- 3.7.1.3 Rise of hybrid and electric propulsion systems

- 3.7.1.4 Technological innovations in sealing solutions

- 3.7.1.5 Stringent regulatory standards and safety requirements

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High material and certification costs

- 3.7.2.2 Complex supply chain and aftermarket constraints

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Seal Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Dynamic seal sub-type

- 5.2.1 Contact seals

- 5.2.2 Clearance seals

- 5.2.3 Others

- 5.3 Static seal sub-type

- 5.3.1 O-Rings & gaskets

- 5.3.2 Other seals

- 5.4 Fire seals

Chapter 6 Market Estimates & Forecast, By Aircraft Type, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Commercial aircraft

- 6.3 Military aircraft

- 6.4 Business jets

- 6.5 Helicopters

- 6.6 UAVs (Unmanned Aerial Vehicles)

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Material, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Elastomers

- 7.3 Thermoplastics

- 7.4 Composite materials

- 7.5 Metal seals

- 7.6 Silicone-based materials

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Fuselage

- 8.3 Wings

- 8.4 Engine & nacelle

- 8.5 Flight control surfaces

- 8.6 Landing gear

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 OEM (Original Equipment Manufacturer)

- 9.3 MRO (Maintenance, Repair, and Overhaul)

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Bal Seal Engineering Inc.

- 11.2 DuPont de Nemours, Inc.

- 11.3 Eagle Industry Co., Ltd.

- 11.4 Eaton Corporation plc

- 11.5 Freudenberg Sealing Technologies

- 11.6 Hutchinson SA

- 11.7 International Seal Company Australia (ISCA) Pty Ltd

- 11.8 Meggitt PLC

- 11.9 Micro Seals

- 11.10 Parker Hannifin Corporation

- 11.11 Performance Sealing Inc.

- 11.12 PPG Industries Inc.

- 11.13 Precision Polymer Engineering

- 11.14 Regal Rexnord Corporation

- 11.15 Saint-Gobain S.A.

- 11.16 SKF Group

- 11.17 Sujan Industries

- 11.18 Technetics Group

- 11.19 Trelleborg Sealing Solutions