PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1755401

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1755401

Medium Voltage Drives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

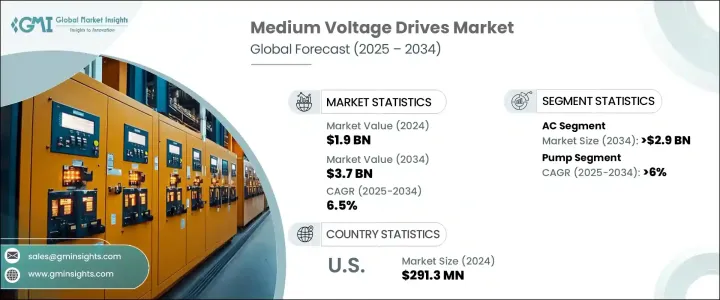

The Global Medium Voltage Drives Market was valued at USD 1.9 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 3.7 billion by 2034. Growth in the industry is largely influenced by increasing industrial demand for high-efficiency energy solutions and the need for sophisticated motor control systems. These drives play a crucial role in optimizing motor performance by adjusting speed and torque, leading to considerable energy savings, reduced operational expenses, and lower emissions. This growing focus on sustainability and cost-effectiveness is encouraging more widespread deployment of these systems across different industries.

Rising capital inflow into sectors that require heavy-duty machinery and energy optimization is shaping the future of the market. Medium voltage drives are becoming essential components in various operations involving large-scale mechanical systems. The development of new industrial infrastructure, particularly those incorporating large HVAC networks and automated systems, is providing a solid foundation for market acceleration. Additionally, the increased focus on automation and smart technologies in manufacturing and utilities is further propelling demand. As companies aim to streamline production and boost efficiency, the adoption of medium voltage drive technologies is becoming a strategic priority.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.9 Billion |

| Forecast Value | $3.7 Billion |

| CAGR | 6.5% |

The AC medium voltage drive segment is expected to dominate the market landscape and is forecasted to exceed USD 2.9 billion by 2034. This segment is experiencing notable growth due to its compatibility with emerging digital technologies. The integration of intelligent systems and real-time analytics is making AC drives increasingly attractive for modern industrial applications. The incorporation of smart features allows for better system responsiveness, predictive maintenance, and operational flexibility, which are critical in today's fast-evolving industrial environments. Growing interest in digital transformation, especially in automated manufacturing, is reinforcing the demand for AC-based systems.

By application, the medium voltage drives market is segmented into pump, fan, conveyor, compressor, extruder, and others. Among these, the pump application is poised to secure the largest market share and is projected to expand at a CAGR of over 6% through 2034. Drives used in pump applications contribute significantly to improving system output and operational efficiency. Enhanced control mechanisms allow precise speed regulation, leading to better performance and reduced energy use. This capability also supports system longevity by minimizing wear and tear and lowering maintenance requirements. The adoption of medium voltage drives in pump operations is gaining traction due to their versatility and performance benefits across diverse industrial sectors.

In the United States, the medium voltage drives market continues to witness strong momentum. The market was assessed at USD 262 million in 2022, followed by USD 276.1 million in 2023 and USD 291.3 million in 2024. Ongoing investments aimed at modernizing infrastructure and enhancing energy efficiency are playing a pivotal role in this upward trend. Demand is further supported by the need for reliable motor control solutions and an increasing push from regulatory bodies for the adoption of energy-efficient technologies. Technological upgrades and federal incentives targeting energy conservation are also making an impact on purchasing decisions and system upgrades in various sectors.

Leading manufacturers in the medium voltage drive market maintain their competitive edge through consistent innovation and robust global operations. Their expertise in delivering integrated power systems and energy solutions tailored for industrial settings positions them as key players. These companies continue to adapt to evolving customer requirements by offering advanced and customized drive systems that are compatible with automated processes and smart manufacturing environments.

Strategic collaborations and partnerships with OEMs, utilities, and industrial end-users are becoming essential for market players. By focusing on technological enhancements and aligning their offerings with modern automation trends, manufacturers are addressing market demands more efficiently. They are also expanding their reach and improving product availability by working closely with stakeholders across the supply chain. Through targeted R&D investments, they are delivering next-generation drives that meet the rising expectations for energy performance and seamless integration into digital industrial ecosystems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic initiative

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Power Range, 2021 - 2034, (USD Million, Units)

- 5.1 Key trends

- 5.2 ≤ 1 MW

- 5.3 1 MW - 3 MW

- 5.4 3 MW - 7 MW

- 5.5 > 7 MW

Chapter 6 Market Size and Forecast, By Drive, 2021 - 2034, (USD Million, Units)

- 6.1 Key trends

- 6.2 AC

- 6.3 DC

- 6.4 Servo

Chapter 7 Market Size and Forecast, By Sales Channel, 2021 - 2034, (USD Million, Units)

- 7.1 Key trends

- 7.2 Direct to end use

- 7.3 Direct to machine builder

- 7.4 Direct to systems integrator

- 7.5 Distribution/partner

Chapter 8 Market Size and Forecast, By Application, 2021 - 2034, (USD Million, Units)

- 8.1 Key trends

- 8.2 Pump

- 8.3 Fan

- 8.4 Cranes & hoists

- 8.5 Conveyor

- 8.6 Compressor

- 8.7 Extruder

- 8.8 Others

Chapter 9 Market Size and Forecast, By End use, 2021 - 2034, (USD Million, Units)

- 9.1 Key trends

- 9.2 Oil & gas

- 9.3 Power generation

- 9.4 Mining & metals

- 9.5 Pulp and paper

- 9.6 Marine

- 9.7 Others

Chapter 10 Market Size and Forecast, By Region, 2021 - 2034, (USD Million, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Thailand

- 10.4.7 Singapore

- 10.4.8 Malaysia

- 10.4.9 Vietnam

- 10.4.10 Indonesia

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 South Africa

- 10.5.4 Egypt

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 CG Power & Industrial Solutions

- 11.3 Danfoss

- 11.4 Delta Electronics

- 11.5 Eaton

- 11.6 Fuji Electric

- 11.7 General Electric

- 11.8 Hitachi Hi-Rel Power Electronics

- 11.9 Ingeteam Power Technology

- 11.10 Johnson Controls

- 11.11 Nidec Industrial Solutions

- 11.12 Rockwell Automation

- 11.13 Schneider Electric

- 11.14 Siemens

- 11.15 TECO-Westinghouse

- 11.16 TMEIC

- 11.17 WEG

- 11.18 Yaskawa Electric