PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1766187

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1766187

Automotive Edge Computing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

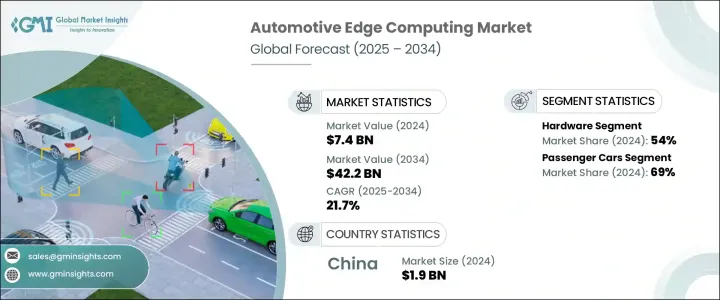

The Global Automotive Edge Computing Market was valued at USD 7.4 billion in 2024 and is estimated to grow at a CAGR of 21.7% to reach USD 42.2 billion by 2034. As the automotive industry rapidly evolves, vehicles are increasingly becoming intelligent platforms capable of processing vast amounts of data in real time. This transformation is being driven by the surge in autonomous driving technologies and connected mobility solutions. As a result, there is a significant shift away from traditional centralized computing models to edge-based data processing, which places computational power closer to the source-inside the vehicle itself.

Automotive edge computing is playing a pivotal role in supporting this shift by delivering the low latency and high bandwidth required to manage complex in-vehicle functions. It enhances real-time decision-making capabilities critical to the safe and efficient operation of modern vehicles. The proliferation of connected features and the growing use of advanced in-vehicle sensors are contributing to an explosion of data, creating a pressing need for on-board analytics and instant response systems. Rather than routing data to distant cloud centers, edge computing empowers vehicles to analyze and act on information at the source, reducing network congestion and response time while enhancing performance, safety, and reliability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.4 Billion |

| Forecast Value | $42.2 Billion |

| CAGR | 21.7% |

This is becoming essential for applications such as driver assistance, predictive maintenance, and intelligent route planning. As manufacturers transition toward software-centric vehicle architectures, the integration of advanced edge platforms becomes vital for creating scalable, secure, and efficient transportation systems built for the next generation of mobility.

In terms of components, the market is categorized into hardware, software, and services. Hardware emerged as the leading segment in 2024, contributing nearly 54% of the global market share, and is anticipated to grow at a CAGR exceeding 22% throughout the forecast period. The rising deployment of high-performance computing units, AI-optimized processors, and automotive-grade modules underscores the growing importance of edge hardware in handling complex data streams. These components are engineered to endure extreme vehicle environments while ensuring continuous processing power for applications like real-time monitoring and autonomous navigation.

By vehicle type, the market is divided into passenger cars and commercial vehicles. Passenger cars held a dominant position in 2024, accounting for approximately 69% of the total market revenue. This segment is set to expand at a CAGR of over 23% between 2025 and 2034. The increasing demand for integrated digital features, personalized driver experiences, and advanced driver-assist systems in passenger vehicles is driving the uptake of edge computing technologies. These vehicles require robust processing capabilities to manage data inputs from various embedded systems, enabling real-time decisions that improve both user experience and vehicle safety.

Based on deployment mode, the industry is segmented into cloud-based and on-premises solutions. Cloud-based deployment continues to command a significant share of the market due to its flexibility, scalability, and ability to support a wide range of connected vehicle functions. These platforms allow seamless software integration, remote updates, and centralized coordination, which are critical for emerging use cases in autonomous driving and fleet management. Their widespread adoption is being propelled by the increasing reliance on vehicle-to-cloud infrastructure that supports services like dynamic route optimization, infotainment delivery, and predictive diagnostics.

Regionally, China led the global automotive edge computing market in 2024, generating around USD 1.9 billion in revenue and capturing roughly 63% of the Asia Pacific market. The country's rapid expansion in smart mobility initiatives, coupled with its position as the world's largest automotive producer, has positioned it at the forefront of edge technology adoption. Strong governmental support, fast-paced development in electric vehicles, and massive deployment of connected vehicle systems continue to bolster market growth in the region.

The automotive edge computing landscape is undergoing a structural transformation as automakers and technology providers prioritize faster, more intelligent, and decentralized processing systems. Growing requirements for instantaneous data interpretation, especially in safety-sensitive driving conditions, are prompting a fundamental rethinking of how information is handled within vehicles. Companies are now focused on integrating AI capabilities, lightweight data processing frameworks, and robust security protocols directly into in-vehicle environments. These advancements are designed to transform raw sensor outputs into meaningful insights that can be acted upon in real time, thus enabling safer, more adaptive, and more efficient transportation systems.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 – 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Deployment mode

- 2.2.5 Enterprise size

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for autonomous and connected vehicles

- 3.2.1.2 Increasing data volume from in-vehicle sensors

- 3.2.1.3 Enhanced infotainment and in-vehicle experience

- 3.2.1.4 Government regulations for road safety and data localization

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial infrastructure cost

- 3.2.2.2 Data privacy & compliance complexities

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with AI and ML for decision-making

- 3.2.3.2. Smart city & V2 X ecosystem expansion

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.8.1 Software development & licensing cost

- 3.8.2 Deployment & integration cost

- 3.8.3 Maintenance & support cost

- 3.8.4 Cybersecurity & compliance cost

- 3.8.5 Training & change management cost

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Use cases

- 3.12 Best-case scenario

- 3.13 Consumer behaviour & adoption trends

- 3.14 User experience & interface trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Edge nodes

- 5.2.2 Gateways

- 5.2.3 Edge servers

- 5.3 Software

- 5.3.1 Edge device management

- 5.3.2 Analytics & processing software

- 5.3.3 Security software

- 5.4 Services

- 5.4.1 Professional

- 5.4.1.1 System integration & deployment

- 5.4.1.2 Consulting & strategy

- 5.4.1.3 Training & support

- 5.4.2 Managed

- 5.4.2.1 Remote monitoring & management

- 5.4.2.2 Maintenance & updates

- 5.4.2.3 Security management

- 5.4.1 Professional

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedans

- 6.2.2 Hatchbacks

- 6.2.3 SUVs

- 6.3 Commercial vehicles

- 6.3.1 Light duty

- 6.3.2 Medium duty

- 6.3.3 Heavy duty

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Cloud-based

- 7.3 On-premises

Chapter 8 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 SME

- 8.3 Large enterprises

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 Autonomous and connected driving

- 9.3 In-vehicle experience & infotainment

- 9.4 Predictive maintenance & diagnostics

- 9.5 Fleet & traffic management

- 9.6 Cybersecurity & data protection

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Amazon

- 11.2 Arteris IP

- 11.3 Autotalks

- 11.4 Bosch Group

- 11.5 Cisco

- 11.6 ETAS GmbH

- 11.7 FogHorn Systems

- 11.8 GreenWave Systems

- 11.9 Hewlett Packard Enterprise (HPE)

- 11.10 Huawei

- 11.11 IBM

- 11.12 Infineon Technologies

- 11.13 Intel

- 11.14 Microsoft

- 11.15 Mobileye

- 11.16 NVIDIA

- 11.17 NXP Semiconductors

- 11.18 Qualcomm Technologies

- 11.19 Siemens

- 11.20 Teradata