PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1766209

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1766209

ELISpot and Fluorospot Assay Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

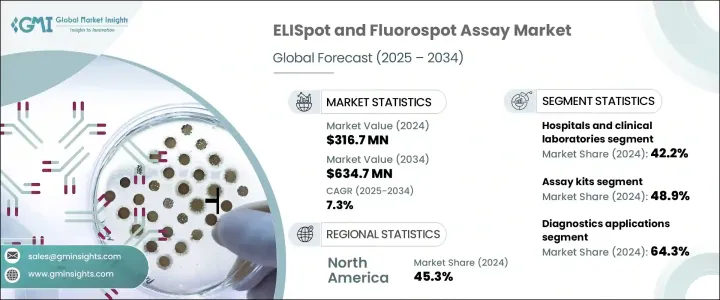

The Global ELISpot and Fluorospot Assay Market was valued at USD 316.7 million in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 634.7 million by 2034. ELISpot is one of the most sensitive techniques available to detect cytokine or antibody secretion at the cellular level, specifically from T or B cells. The Fluorospot assay, an extension of the ELISpot, allows for the simultaneous detection of multiple proteins secreted from a single cell using fluorescent labeling. Both assays are widely used for immune monitoring in clinical research, vaccine development, and clinical studies. The rising prevalence of infectious and immune-related diseases is a significant driver for the increased demand for these assays.

These assays play a crucial role in monitoring immune responses, especially in vaccination efforts targeting infectious diseases, immunotherapies, and vaccine research. The growing incidence of diseases like tuberculosis, cancer, and emerging viral infections has intensified the need for advanced immunological assays. ELISpot and Fluorospot systems stand out for their high sensitivity, single-cell resolution, and multiplexing abilities, which make them invaluable tools in clinical and research immunology.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $316.7 Million |

| Forecast Value | $634.7 Million |

| CAGR | 7.3% |

In 2024, the assay kits segment held the largest share of 48.9%. This dominance can be attributed to the growing adoption of standardized kits that are easy to use, reproducible, and compatible with cell-mediated immunity research frameworks. The convenience of ready-to-use kits makes them a preferred choice in academic, clinical, and pharmaceutical research settings. These kits are particularly popular for their role in infectious disease, cancer immunotherapy, and transplant rejection monitoring. The high demand for cytokine-specific detection has contributed to the growing adoption of these assays. Furthermore, the increasing global burden of diseases continues to drive the need for these assay solutions.

The diagnostics application segment held the largest share 64.3% in 2024. This is primarily due to the increasing use of ELISpot and Fluorospot assays in the diagnosis of various infectious diseases, including tuberculosis, autoimmune disorders, cancer immunotherapy, and other inflammatory conditions. The assays' high accuracy makes them essential in clinical diagnostics, positioning them as key tools in precision medicine. Their ability to identify and monitor the progression of immune-related disorders further propels market growth. This trend highlights the critical role these assays play in both the diagnosis and management of diseases, cementing their importance in clinical settings.

Asia Pacific ELISpot and Fluorospot Assay Market is expected to witness the highest growth, with a CAGR of 8% from 2025 to 2034. The growth is driven by the rising adoption of healthcare technologies, significant investments in immunological research, and the increasing prevalence of infectious diseases such as tuberculosis and viral infections in the region. Countries like China, India, and South Korea are rapidly embracing these technologies, aided by heightened healthcare awareness and favorable regulatory frameworks. The growing biopharmaceutical industry and an increase in clinical trial activity are further contributing to the demand for precise immune surveillance tools like ELISpot and Fluorospot assays.

The market features major participants including Bio-Techne Corporation, BD, Mabtech, Oxford Immunotec, Bio-Connect, Cellular Technology, Abcam Limited, Stemcell Technologies, Autoimmun Diagnostika, Lophius Biosciences, GenScript Biotech, Merck, R&D Systems, U-CyTech. To strengthen their market position, companies in the ELISpot and Fluorospot assay market are focusing on expanding their product offerings by developing innovative and more sensitive assays that provide higher accuracy and resolution. Partnerships and collaborations with academic institutions, healthcare providers, and pharmaceutical companies are becoming a key strategy to promote the widespread adoption of these assays. Additionally, companies are investing in research and development to enhance their existing product lines and create next-generation assays. Efforts to integrate automation, improve ease of use, and offer ready-to-use kits are also crucial in making these assays more accessible to a wider range of research and clinical users. Moreover, strategic regional expansion, particularly in emerging markets like Asia Pacific, is enabling companies to tap into the growing demand for advanced diagnostic solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of chronic and infectious diseases

- 3.2.1.2 Growing awareness of early disease diagnosis

- 3.2.1.3 Increasing healthcare spending and government support

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled personnel

- 3.2.2.2 Stringent regulatory requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Patent Analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Assay kits

- 5.3 Analyzers

- 5.4 Ancillary products

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Research applications

- 6.3 Diagnostics applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinical laboratories

- 7.3 Academic and research institutions

- 7.4 Biopharmaceutical companies

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 BD

- 9.2 Abcam Limited

- 9.3 Autoimmun Diagnostika

- 9.4 Bio-Connect

- 9.5 Bio-Techne Corporation

- 9.6 Cellular Technology

- 9.7 GenScript Biotech

- 9.8 Lophius Biosciences

- 9.9 Mabtech

- 9.10 Merck

- 9.11 Oxford Immunotec

- 9.12 R&D Systems

- 9.13 Stemcell Technologies

- 9.14 U-CyTech