PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1766232

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1766232

Pastry and Cakes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

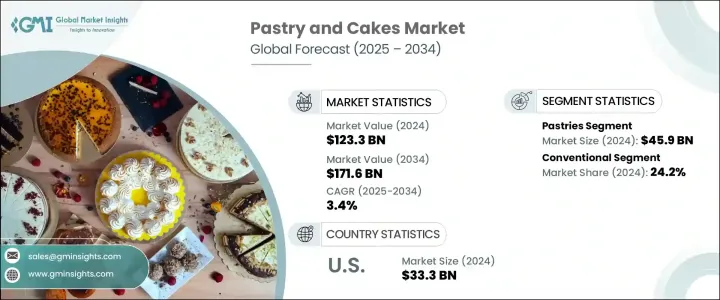

The Global Pastry and Cakes Market was valued at USD 123.3 billion in 2024 and is estimated to grow at a CAGR of 3.4% to reach USD 171.6 billion by 2034. The rising culture of celebration across regions and income brackets continues to play a significant role in driving this market. As consumers increasingly lean toward indulgent food items to commemorate daily moments and special occasions alike, pastries and cakes have become a preferred choice for both emotional and social consumption. The shift in spending priorities, driven by a desire for everyday luxuries, has fueled this trend further. With baked goods being a consistent part of global dietary habits, particularly during events and gatherings, their significance goes beyond simple nourishment and enters the territory of social expression and gifting.

In both established and developing economies, baked goods continue to witness widespread adoption. The convenience factor-combined with evolving lifestyles and increasing urbanization-is leading to consistent changes in how and when people consume sweet snacks. Compact, ready-to-eat baked items are enjoying growing popularity, especially as consumers seek out products that match their fast-paced lives. This shift is also mirrored in the rising performance of food retailers, supermarkets, hypermarkets, and specialty outlets that now feature an expanded array of pastry and cake products. Moreover, commercial sectors such as cafes, hotels, and restaurants are contributing notably to market revenues by offering these items across formats, time slots, and customer segments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $123.3 Billion |

| Forecast Value | $171.6 Billion |

| CAGR | 3.4% |

A significant portion of market growth is also tied to the growing global middle class and its exposure to international food influences. As awareness around diverse culinary experiences rises, so does the demand for variety across the pastry and cake category, whether it's in terms of product design, ingredients, or formats. A move toward innovation is visible, with increasing interest in diet-specific variants such as organic, gluten-free, vegan, and low-sugar options. These offerings are gaining favor among health-conscious consumers while still delivering on flavor and satisfaction. The demand is being fueled by both residential customers buying for home consumption and commercial buyers looking to update their menus with healthier yet indulgent choices.

While brick-and-mortar stores continue to dominate in terms of market reach and penetration, the digital landscape is emerging as a key enabler. Online retail channels are becoming increasingly crucial in expanding access to consumers across diverse geographies. With direct-to-consumer delivery models and enhanced e-commerce capabilities, brands are unlocking new demographic opportunities and increasing their customer base beyond traditional urban markets.

The pastry segment alone was valued at USD 45.9 billion in 2024 and is projected to register a CAGR of 2.7% from 2025 to 2034. This segment holds the largest share of the overall market, driven by its universal appeal and adaptability across various consumption scenarios-from quick snacks to celebratory treats. Easy availability through both traditional retail and foodservice outlets contributes to its widespread appeal. Additionally, portability and portion control make pastries a convenient choice for consumers seeking both indulgence and ease of consumption.

In terms of ingredients, the conventional segment led the market with a value of USD 29.8 billion in 2024, accounting for 24.2% of the total share. It is expected to grow at a CAGR of 3.3% over the forecast period. The dominance of conventional ingredients stems from their versatility, ease of procurement, and consumer familiarity. These products enable manufacturers to maintain consistency in quality and taste while benefiting from economies of scale. Their wide acceptance in both advanced and growing markets also provides them with a competitive edge, allowing for deeper market penetration and streamlined distribution strategies.

The United States stood out as a key contributor to the global market, with the pastry and cakes sector valued at USD 33.3 billion in 2024. It is anticipated to expand at a CAGR of 3.3% from 2025 through 2034. The country's strong consumer spending on baked goods, coupled with a robust presence of retail bakeries, specialty stores, and quick-service restaurants, keeps demand levels consistently high. Product innovation, frequent seasonal campaigns, and the inclusion of functional ingredients are strategies being used to maintain consumer interest. The convenience of digital platforms and app-based ordering has further strengthened accessibility, particularly in suburban and urban areas.

The competitive landscape of the global market is shaped by numerous leading players focused on product development, branding, and expanding their consumer reach. Competition is increasingly centered around health-forward formulations aimed at high-income consumers, leading brands to shift their offerings toward wellness-driven product lines.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1.1 Regional

- 2.2.1.2 Product type

- 2.2.1.3 Ingredient

- 2.2.1.4 Distribution channel

- 2.2.1.5 End use

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.5 Executive decision points

- 2.6 Critical success factors

- 2.7 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for premium and artisanal products

- 3.2.1.2 Increasing consumption of convenience foods

- 3.2.1.3 Rising disposable income and urbanization

- 3.2.1.4 Expanding cafe culture and bakery chains

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Health and dietary concerns

- 3.2.2.2 Fluctuating raw material prices

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Cakes

- 5.2.1 Layer cakes

- 5.2.2 Cupcakes

- 5.2.3 Sheet cakes

- 5.2.4 Cheesecakes

- 5.2.5 Celebration cakes

- 5.2.6 Others

- 5.3 Pastries

- 5.3.1 Danish pastries

- 5.3.2 Croissants

- 5.3.3 Puff pastries

- 5.3.4 Eclairs

- 5.3.5 Tarts

- 5.3.6 Others

- 5.4 Sweet pies

- 5.4.1 Fruit pies

- 5.4.2 Cream pies

- 5.4.3 Others

- 5.5 Dessert bars and brownies

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Ingredient, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Conventional

- 6.3 Organic

- 6.4 Gluten-free

- 6.5 Sugar-free / reduced sugar

- 6.6 Vegan

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Retail bakeries

- 7.2.1 Artisanal bakeries

- 7.2.2 Chain bakeries

- 7.3 Supermarkets and hypermarkets

- 7.4 Convenience stores

- 7.5 Specialty food stores

- 7.6 Online retail

- 7.6.1 E-commerce platform

- 7.6.2 Direct-to-consumer websites

- 7.7 Food service sector

- 7.7.1 Cafes and restaurants

- 7.7.2 Hotels

- 7.7.3 Catering services

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Cafes and bakery chains

- 8.3.2 Restaurants and hotels

- 8.3.3 Catering services

- 8.3.4 Event management companies

- 8.3.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AAK AB

- 10.2 Archer Daniels Midland Company

- 10.3 Associated British Foods plc

- 10.4 Bakels Group

- 10.5 BASF SE

- 10.6 Cargill, Incorporated

- 10.7 Corbion N.V.

- 10.8 Dawn Food Products, Inc.

- 10.9 DuPont de Nemours, Inc.

- 10.10 Flowers Foods, Inc.

- 10.11 General Mills, Inc.

- 10.12 Grupo Bimbo, S.A.B. de C.V.

- 10.13 Ingredion Incorporated

- 10.14 Kerry Group plc

- 10.15 Koninklijke DSM N.V.

- 10.16 Lesaffre Group

- 10.17 Mondel?z International, Inc.

- 10.18 Puratos Group

- 10.19 DSM-Firmenich AG

- 10.20 Tate & Lyle PLC