PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1766261

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1766261

Polymeric Microcapsules Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

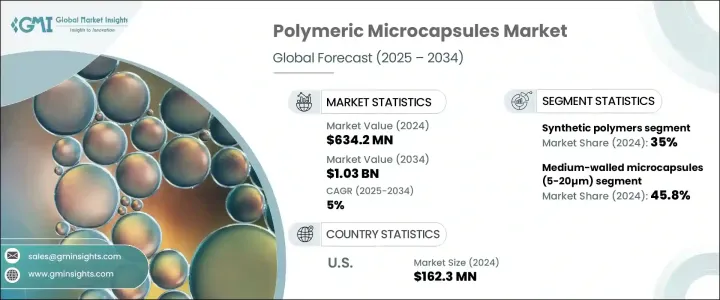

The Global Polymeric Microcapsules Market was valued at USD 634.2 million in 2024 and is estimated to grow at a CAGR of 5% to reach USD 1.03 billion by 2034. The increasing demand for controlled-release technologies across various industries is the main driver for this market growth. Microencapsulation techniques are particularly in demand in the pharmaceutical and healthcare sectors, where controlled release is essential for improving drug efficacy, minimizing side effects, and enhancing patient compliance. These technologies ensure precise timing and location for the release of active ingredients, which is vital for managing chronic conditions and advancing personalized medicine. In addition to pharmaceuticals, the use of polymeric microcapsules is expanding into sectors like personal care, textiles, and food products.

For instance, encapsulation is increasingly used in beauty products and self-care items, protecting sensitive ingredients and enhancing product performance. In the food industry, these microcapsules help improve shelf life by protecting probiotics in products like fermented beverages. The growing adoption of microencapsulation in functional foods and health supplements is further boosting market growth. As consumers demand longer-lasting, safer, and more effective products, polymeric microcapsules are becoming essential in a wide range of applications, fueling innovation across the market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $634.2 Million |

| Forecast Value | $1.03 Billion |

| CAGR | 5% |

The synthetic polymers segment held a 35% share in 2024, primarily due to their cost-effectiveness, versatility, and compatibility with various active ingredients. These polymers enable the controlled release of substances and are widely used in pharmaceutical and agrochemical products. Additionally, they are gaining traction in the food and cosmetics sectors, owing to their superior barrier properties, tunable degradation rates, and high stability. The scalability of synthetic polymers, coupled with the ease of their production, makes them more favorable than natural or hybrid alternatives, which are less suitable for mass production.

Medium-walled microcapsules segment, which measure between 5 and 20 micrometers, accounted for 45.8% share in 2024. These microcapsules are favored for their structural integrity and ability to release active ingredients efficiently over time, making them ideal for use in drug delivery systems, agriculture, and food products. Their size offers the necessary control over the release rate, which is essential in applications where precise timing and dosage are critical. The

U.S. Polymeric Microcapsules Market was valued at USD 162.3 million in 2024, reflecting the country's leading role in driving innovation in microencapsulation technologies. The well-established healthcare system and regulatory environment in the U.S. provide a stable foundation for the growth of controlled-release technologies. U.S. consumers are increasingly demanding products that offer enhanced performance, safety, and user-friendly features, which polymeric microcapsules help deliver by improving shelf life, flavor masking, and controlled ingredient delivery.

Key players in the Global Polymeric Microcapsules Market, such as BASF, Evonik, Givaudan, IFF, and Lonza, continue to focus on expanding their market presence through innovations and product development. These companies adopt strategies that include investing in R&D to advance microencapsulation technologies, forming strategic partnerships to improve market penetration, and expanding their portfolios to meet the growing demand from industries like food, healthcare, and cosmetics. By offering customizable solutions, enhancing product performance, and ensuring regulatory compliance, these companies strengthen their foothold in the market. Additionally, they are increasingly focusing on offering solutions that improve sustainability and address consumer demands for cleaner, safer products.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries. Note: the above trade statistics will be provided for key countries only

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Technological advancements and innovations

- 3.7 Regulatory landscape

- 3.7.1 Global

- 3.7.1.1 FDA regulations (U.S.)

- 3.7.1.2 EMA regulations (Europe)

- 3.7.1.3 CFDA regulations (China)

- 3.7.1.4 Other regional regulatory bodies

- 3.7.2 Environmental regulations

- 3.7.2.1 Microplastics regulations

- 3.7.2.2 Biodegradability standards

- 3.7.2.3 Sustainability requirements

- 3.7.1 Global

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Growing demand for controlled release technologies

- 3.8.1.2 Technological advancements in encapsulation techniques

- 3.8.1.3 Increasing applications in pharmaceutical and healthcare sectors

- 3.8.1.4 Growing focus on sustainable and biodegradable materials

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High production costs and complex manufacturing processes

- 3.8.2.2 Competition from alternative technologies

- 3.8.2.3 Environmental concerns related to non-biodegradable polymers

- 3.8.3 Market opportunities

- 3.8.3.1 Emerging applications in self-healing materials

- 3.8.3.2 Growing demand in cosmetics and personal care

- 3.8.3.3 Expansion in agricultural applications

- 3.8.3.4 Potential in textile industry for functional fabrics

- 3.8.3.5 Opportunities in thermal energy storage systems

- 3.8.1 Growth drivers

- 3.9 Raw materials analysis

- 3.9.1 Key raw materials for shell formation

- 3.9.2 Core material selection criteria

- 3.9.3 Raw material suppliers landscape

- 3.9.4 Raw material price trends

- 3.10 Future trends and emerging applications

- 3.10.1 Technological advancements

- 3.10.1.1 Smart and programmable release systems

- 3.10.1.2 Multi-functional microcapsules

- 3.10.1.3 Nanotechnology integration

- 3.10.1.4 Green manufacturing processes

- 3.10.2 Material innovations

- 3.10.2.1 Novel biodegradable polymers

- 3.10.2.2 Bio-based and sustainable materials

- 3.10.2.3 Stimuli-responsive materials

- 3.10.2.4 Hybrid and composite materials

- 3.10.3 Emerging applications

- 3.10.3.1 Advanced drug delivery systems

- 3.10.3.2 Self-healing materials

- 3.10.3.3 Smart textiles

- 3.10.3.4 Thermal energy storage

- 3.10.3.5 3d printing applications

- 3.10.3.6 Microbiome encapsulation

- 3.10.4 Industry convergence opportunities

- 3.10.5 Future market scenarios

- 3.10.6 Long-term growth prospects

- 3.10.1 Technological advancements

- 3.11 Growth potential analysis

- 3.12 Pricing analysis (USD/Tons) 2021-2034

- 3.12.1 Factors affecting pricing

- 3.12.1.1 Raw material costs

- 3.12.1.2 Energy costs

- 3.12.1.3 Production scale

- 3.12.1.4 Technology maturity

- 3.12.1.5 Market competition

- 3.12.1.6 Petroleum-based alternatives pricing

- 3.12.1 Factors affecting pricing

- 3.13 Technology landscape and manufacturing processes

- 3.13.1 Microencapsulation techniques

- 3.13.1.1 Physical methods

- 3.13.1.2 Spray drying

- 3.13.1.3 Fluid bed coating

- 3.13.1.4 Centrifugal extrusion

- 3.13.1.5 Freeze drying

- 3.13.2 Chemical methods

- 3.13.2.1 Interfacial polymerization

- 3.13.2.2 In-situ polymerization

- 3.13.2.3 Emulsion polymerization

- 3.13.3 Physicochemical methods

- 3.13.3.1 Complex coacervation

- 3.13.3.2 Simple coacervation

- 3.13.3.3 Solvent evaporation

- 3.13.4 Advanced technologies

- 3.13.4.1 Microfluidic techniques

- 3.13.4.2 Supercritical fluid technology

- 3.13.4.3 Layer-by-layer assembly

- 3.13.4.4 Electrospinning

- 3.13.5 Technological innovations and patent analysis

- 3.13.5.1 Recent technological breakthroughs

- 3.13.5.2 R&D trends and future technological directions

- 3.13.1 Microencapsulation techniques

- 3.14 Porter's analysis

- 3.15 PESTEL analysis

- 3.16 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Company heat map analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.6.1 Expansion

- 4.6.2 Mergers & Acquisition

- 4.6.3 Collaborations

- 4.6.4 New Product Launches

- 4.6.5 Research & Development

- 4.7 Competitive landscape

- 4.7.1 Market concentration analysis

- 4.7.2 Competitive positioning and strategies

- 4.7.3 Mergers, acquisitions, and strategic partnerships

- 4.7.4 New product launches and innovations

- 4.7.5 Marketing and promotional strategies

- 4.8 Recent developments & impact analysis by key players

- 4.8.1 Company categorization

- 4.8.2 Participant’s overview

- 4.8.3 Financial performance

- 4.9 Source benchmarking

Chapter 5 Market Estimates and Forecast, By Polymer Type, 2021–2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Natural polymers

- 5.2.1 Polysaccharide-based polymers

- 5.2.1.1 Cellulose and derivatives

- 5.2.1.2 Starch and derivatives

- 5.2.1.3 Chitosan

- 5.2.1.4 Alginate

- 5.2.1.5 Gums (arabic, xanthan, etc.)

- 5.2.2 Protein-based polymers

- 5.2.2.1 Gelatin

- 5.2.2.2 Albumin

- 5.2.2.3 Collagen

- 5.2.2.4 Other protein-based polymers

- 5.2.3 Other natural polymers

- 5.2.1 Polysaccharide-based polymers

- 5.3 Synthetic polymers

- 5.3.1 Biodegradable synthetic polymers

- 5.3.1.1 PLA

- 5.3.1.2 PLGA

- 5.3.1.3 PCL

- 5.3.1.4 PHA

- 5.3.1.5 Other biodegradable synthetic polymers

- 5.3.2 Non-biodegradable synthetic polymers

- 5.3.2.1 Polyurethane/polyurea

- 5.3.2.2 PMMA

- 5.3.2.3 Polyethylene

- 5.3.2.4 Polystyrene

- 5.3.2.5 Other non-biodegradable synthetic polymers

- 5.3.1 Biodegradable synthetic polymers

- 5.4 Semi-synthetic polymers

- 5.4.1 Cellulose derivatives

- 5.4.2 Modified starches

- 5.4.3 Other semi-synthetic polymers

- 5.5 Hybrid and composite polymers

- 5.5.1 Polymer blends

- 5.5.2 Polymer-inorganic hybrids

- 5.5.3 Multi-layer polymer systems

- 5.6 Emerging polymer materials

- 5.6.1 Smart and stimuli-responsive polymers

- 5.6.2 Bio-inspired polymeric materials

- 5.6.3 Nanocomposite polymers

Chapter 6 Market Estimates and Forecast, By Shell Thickness, 2021–2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Thin-walled microcapsules (1-5µm)

- 6.3 Medium- walled microcapsules (5-20µm)

- 6.4 Thick- walled microcapsules (20-1000µm)

Chapter 7 Market Estimates and Forecast, By Core Material, 2021–2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Solid core materials

- 7.2.1 Diffusion-controlled release

- 7.2.1.1 Mononuclear (core-shell) microcapsules

- 7.2.1.2 Matrix encapsulation systems

- 7.2.1.3 Multi-wall microcapsules

- 7.2.2 Pressure-triggered release

- 7.2.2.1 Mononuclear (core-shell) microcapsules

- 7.2.2.2 Polynuclear microcapsules

- 7.2.3 Enzyme-triggered release

- 7.2.3.1 Mononuclear (core-shell) microcapsules

- 7.2.3.2 Matrix encapsulation systems

- 7.2.1 Diffusion-controlled release

- 7.3 Liquid core materials

- 7.3.1 Dissolution-controlled release

- 7.3.1.1 Mononuclear (core-shell) microcapsules

- 7.3.1.2 Multi-wall microcapsules

- 7.3.1.3 Temperature-responsive release

- 7.3.2 Multi-wall microcapsules

- 7.3.2.1 Matrix encapsulation systems

- 7.3.2.2 Janus and complex morphologies

- 7.3.3 p H-responsive release

- 7.3.3.1 Mononuclear (core-shell) microcapsules

- 7.3.3.2 Multi-wall microcapsules

- 7.3.1 Dissolution-controlled release

- 7.4 Gas core materials

- 7.4.1 Pressure-triggered release

- 7.4.1.1 Mononuclear (core-shell) microcapsules

- 7.4.1.2 Janus and complex morphologies

- 7.4.2 Other stimuli-responsive release mechanisms

- 7.4.2.1 Polynuclear microcapsules

- 7.4.2.2 Janus and complex morphologies

- 7.4.1 Pressure-triggered release

- 7.5 Multiple core materials

- 7.5.1 Diffusion-controlled release

- 7.5.1.1 Polynuclear microcapsules

- 7.5.1.2 Multi-wall microcapsules

- 7.5.2 Temperature-responsive release

- 7.5.2.1 Janus and complex morphologies

- 7.5.2.2 Matrix encapsulation systems

- 7.5.3 pH-responsive release

- 7.5.3.1 Janus and complex morphologies

- 7.5.3.2 Matrix encapsulation systems

- 7.5.4 Other stimuli-responsive release mechanisms

- 7.5.4.1 Janus and complex morphologies

- 7.5.1 Diffusion-controlled release

Chapter 8 Market Estimates and Forecast, By End Use, 2021–2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Pharmaceutical and healthcare

- 8.2.1 Controlled drug delivery systems

- 8.2.2 Taste masking

- 8.2.3 Protein and peptide delivery

- 8.2.4 Targeted therapy

- 8.2.5 Cell encapsulation

- 8.2.6 Vaccine delivery

- 8.2.7 Other pharmaceutical applications

- 8.3 Food and beverage

- 8.3.1 Flavor encapsulation

- 8.3.2 Nutrient preservation

- 8.3.3 Probiotics encapsulation

- 8.3.4 Functional food ingredients

- 8.3.5 Shelf-life extension

- 8.3.6 Other food and beverage applications

- 8.4 Cosmetics and personal care

- 8.4.1 Fragrance encapsulation

- 8.4.2 Active ingredient delivery

- 8.4.3 UV protection

- 8.4.4 Anti-aging formulations

- 8.4.5 Color cosmetics

- 8.4.6 Other cosmetic applications

- 8.5 Agriculture

- 8.5.1 Controlled release fertilizers

- 8.5.2 Pesticide and herbicide delivery

- 8.5.3 Seed coating

- 8.5.4 Soil enhancement

- 8.5.5 Other agricultural applications

- 8.6 Textile

- 8.6.1 Fragrance-releasing textiles

- 8.6.2 Antimicrobial textiles

- 8.6.3 Phase change materials for thermal regulation

- 8.6.4 UV-protective textiles

- 8.6.5 Other textile applications

- 8.7 Construction and building materials

- 8.7.1 Self-healing concrete

- 8.7.2 Thermal energy storage

- 8.7.3 Corrosion protection

- 8.7.4 Fire retardant systems

- 8.7.5 Other construction applications

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021–2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Balchem Corporation

- 10.2 BASF SE

- 10.3 Calyxia

- 10.4 Evonik Industries AG

- 10.5 Givaudan SA

- 10.6 IFF

- 10.7 Lonza Group

- 10.8 Microtek Laboratories

- 10.9 Mikrocaps

- 10.10 Milliken

- 10.11 Tagra Biotechnologies