PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1766292

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1766292

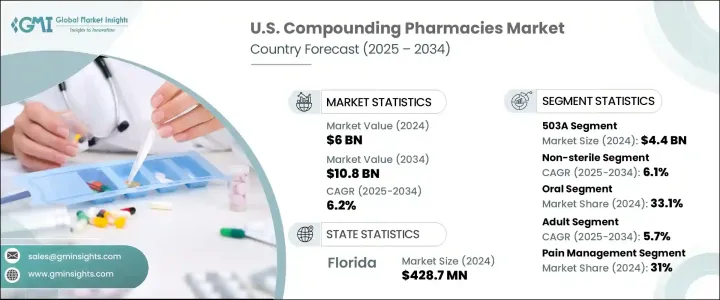

U.S. Compounding Pharmacies Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

U.S. Compounding Pharmacies Market was valued at USD 6 billion in 2024 and is estimated to grow at a CAGR of 6.2% to reach USD 10.8 billion by 2034. This growth is driven by the increasing demand for personalized medications, particularly among pediatric and geriatric populations who may require allergen-free or tailored formulations. Additionally, the rising prevalence of chronic diseases such as diabetes, cancer, and endocrine disorders is contributing to the need for customized treatment options. Compounding pharmacies play a crucial role in addressing drug shortages by providing alternative formulations of medications that are in limited supply. Their ability to create products that are not commercially available or customizable is shifting them from the background to the forefront of healthcare services. The growing recognition of these pharmacies is further supported by the increasing prevalence of chronic diseases, expanding the market as they demand long-term adherence to treatment protocols with precise dosages, making compounded medications a suitable solution.

The non-sterile segment led the market in 2024 and is anticipated to grow at a CAGR of 6.1% between 2025 and 2034. Non-sterile dosage forms include medicines taken orally, such as pills and liquids, or topical applications like creams and ointments. The rising demand for such dosage forms will boost the compounding pharmacies market and propel segmental growth. Additionally, non-sterile formulations are subject to less strict regulatory requirements, making them more accessible for 503A pharmacies operating under state pharmacy boards. As the incidence of chronic conditions, geriatric care needs, and lifestyle-related conditions continues to rise, the non-sterile segment is well-positioned to sustain its leading role in the U.S. compounding pharmacy landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6 Billion |

| Forecast Value | $10.8 Billion |

| CAGR | 6.2% |

The oral segment dominated the market in 2024 with a market share of 33.1%. Increasing demand for oral compounded medications can be attributed to several benefits associated with the oral dosage form, such as self-administration, convenience, and pain-free. The availability of several medications in oral form, such as solid preparations that include capsules, tablets, powders, and liquid preparations like syrups and suspensions, compared to other dosage forms, fuels the segmental growth. Moreover, a higher preference for oral compounded medications in children and the geriatric population further drives the oral segment market growth.

Major players operating in the U.S. Compounding Pharmacies Industry include Triangle Compounding Pharmacies, Pavilion Compounding Pharmacy, Nephron Pharmaceuticals, McGuff Outsourcing Solutions, Institutional Pharmacy Solutions, Fagron, Dougherty's Pharmacy, Baxter International, Village Compounding Pharmacy, Wedgewood Pharmacy, Pencol Compounding Pharmacy, QuVa Pharma, Rx3 Compounding Pharmacy, B. Braun, and Harrow. These companies are adopting various strategies to strengthen their market position. They are investing in research and development to innovate and customize formulations effectively. Additionally, they are expanding their product portfolios to include a broader range of compounded medications. Strategic partnerships and collaborations are also being pursued to enhance distribution networks and improve market reach. Furthermore, these companies are focusing on compliance with regulatory standards to ensure the safety and efficacy of their compounded products. By implementing these strategies, they aim to meet the growing demand for personalized medications and address the challenges posed by drug shortages.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Zonal

- 2.2.2 Pharmacy type

- 2.2.3 Sterility

- 2.2.4 Product

- 2.2.5 Compounding type

- 2.2.6 Therapeutic area

- 2.2.7 Application

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing geriatric population and improved longevity

- 3.2.1.2 Growing acceptance of personalized medicines in the U.S.

- 3.2.1.3 Increasing drug shortage

- 3.2.1.4 Convenience of using compounded drugs

- 3.2.1.5 Growing demand for compounded bioidentical menopausal hormone therapy (BMHT) among women

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Issues related to safety standards of compounded drugs

- 3.2.2.2 Changing regulatory scenario

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding veterinary compounding

- 3.2.3.2 Advancements in delivery technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement landscape

- 3.6 Innovative compounding technologies

- 3.6.1 Web-based quality management system

- 3.6.2 Digital tools

- 3.7 Future market trends

- 3.8 Consumer behaviour analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Pharmacy Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 503A

- 5.3 503B

Chapter 6 Market Estimates and Forecast, By Sterility, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Sterile

- 6.3 Non-sterile

Chapter 7 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.2.1 Solid preparations

- 7.2.1.1 Tablets

- 7.2.1.2 Capsules

- 7.2.1.3 Granules

- 7.2.1.4 Powder

- 7.2.1.5 Other solid preparations

- 7.2.2 Liquid preparations

- 7.2.2.1 Solutions

- 7.2.2.2 Suspension

- 7.2.2.3 Emulsion

- 7.2.2.4 Syrup

- 7.2.2.5 Other liquid preparations

- 7.2.1 Solid preparations

- 7.3 Topical

- 7.3.1 Ointments

- 7.3.2 Creams

- 7.3.3 Gels

- 7.3.4 Pastes

- 7.3.5 Other topical products

- 7.4 Rectal

- 7.4.1 Suppositories

- 7.4.2 Enema

- 7.4.3 Other rectal products

- 7.5 Parenteral

- 7.5.1 Large volume parenterals (LVPs)

- 7.5.2 Small volume parenterals (LVPs)

- 7.6 Nasal

- 7.7 Ophthalmic

- 7.8 Otic

Chapter 8 Market Estimates and Forecast, By Compounding Type, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Pharmaceutical ingredient alteration (PIA)

- 8.3 Currently unavailable pharmaceutical manufacturing (CUPM)

- 8.4 Pharmaceutical dosage alteration (PDA)

- 8.5 Other compounding types

Chapter 9 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Adult

- 9.3 Geriatric

- 9.4 Veterinary

- 9.5 Pediatric

Chapter 10 Market Estimates and Forecast, By Therapeutic Area, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Pain management

- 10.3 Hormone replacement

- 10.4 Dermatology

- 10.5 Specialty drugs

- 10.6 Nutritional supplements

- 10.7 Other therapeutic areas

Chapter 11 Market Estimates and Forecast, By Zone, 2021 – 2034 ($ Mn)

- 11.1 Key trends

- 11.2 Northeast

- 11.2.1 Connecticut

- 11.2.2 Maine

- 11.2.3 Massachusetts

- 11.2.4 New Hampshire

- 11.2.5 Rhode Island

- 11.2.6 Vermont

- 11.2.7 New Jersey

- 11.2.8 New York

- 11.2.9 Pennsylvania

- 11.3 East North Central

- 11.3.1 Wisconsin

- 11.3.2 Michigan

- 11.3.3 Illinois

- 11.3.4 Indiana

- 11.3.5 Ohio

- 11.4 West North Central

- 11.4.1 North Dakota

- 11.4.2 South Dakota

- 11.4.3 Nebraska

- 11.4.4 Kansas

- 11.4.5 Minnesota

- 11.4.6 Iowa

- 11.4.7 Missouri

- 11.5 South Atlantic

- 11.5.1 Delaware

- 11.5.2 Maryland

- 11.5.3 District of Columbia

- 11.5.4 Virginia

- 11.5.5 West Virginia

- 11.5.6 North Carolina

- 11.5.7 South Carolina

- 11.5.8 Georgia

- 11.5.9 Florida

- 11.6 East South Central

- 11.6.1 Kentucky

- 11.6.2 Tennessee

- 11.6.3 Mississippi

- 11.6.4 Alabama

- 11.7 West South Central

- 11.7.1 Oklahoma

- 11.7.2 Texas

- 11.7.3 Arkansas

- 11.7.4 Louisiana

- 11.8 Mountain States

- 11.8.1 Idaho

- 11.8.2 Montana

- 11.8.3 Wyoming

- 11.8.4 Nevada

- 11.8.5 Utah

- 11.8.6 Colorado

- 11.8.7 Arizona

- 11.8.8 New Mexico

- 11.9 Pacific Central

- 11.9.1 California

- 11.9.2 Alaska

- 11.9.3 Hawaii

- 11.9.4 Oregon

- 11.9.5 Washington

Chapter 12 Company Profiles

- 12.1 Baxter International

- 12.2 B. Braun

- 12.3 Dougherty's Pharmacy

- 12.4 Fagron

- 12.5 Fresenius Kabi

- 12.6 Harrow

- 12.7 Institutional Pharmacy Solutions

- 12.8 ITC Compounding Pharmacy

- 12.9 McGuff Outsourcing Solutions

- 12.10 Nephron Pharmaceuticals

- 12.11 Pavilion Compounding Pharmacy

- 12.12 Pencol Compounding Pharmacy

- 12.13 QuVa Pharma

- 12.14 Rx3 Compounding Pharmacy

- 12.15 Triangle Compounding Pharmacies

- 12.16 Village Compounding Pharmacy

- 12.17 Wedgewood Pharmacy