PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1766322

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1766322

Animal Artificial Insemination Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

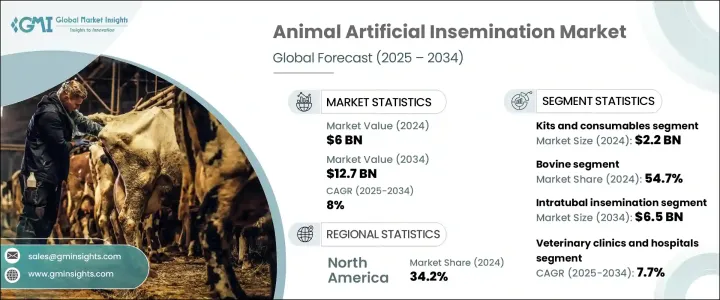

The Global Animal Artificial Insemination Market was valued at USD 6 billion in 2024 and is estimated to grow at a CAGR of 8% to reach USD 12.7 billion by 2034. This growth is being driven by a rising focus on genetic improvement, increased demand for higher quality livestock, and the widespread adoption of advanced reproductive solutions across developing regions. As the global population continues to grow, so does the need for efficient livestock production to meet escalating demands for meat and dairy products. Artificial insemination (AI), as a method of assisted reproduction, is becoming increasingly important in meeting these needs by enhancing the reproductive performance and productivity of animals.

In many parts of the world, livestock breeders are turning to AI not only to improve herd quality but also to reduce breeding-related costs and boost productivity. By enabling selective breeding, AI helps increase desirable genetic traits such as disease resistance, milk yield, and meat quality, which makes it a vital component of modern livestock management practices. Market expansion is further influenced by the rising investments in the veterinary healthcare industry and the growing awareness among farmers about the long-term benefits of controlled breeding techniques. Additionally, the integration of AI with veterinary services, along with the continuous development of precision breeding tools, is enhancing the effectiveness and reliability of artificial insemination procedures, encouraging its widespread use across species and regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6 Billion |

| Forecast Value | $12.7 Billion |

| CAGR | 8% |

In terms of product type, in 2024, the kits and consumables segment led the market with a valuation of USD 2.2 billion. The frequent use of consumables like insemination pipettes, straws, gloves, and catheters makes them essential components in every AI cycle, driving strong demand. Unlike capital-intensive equipment, these products require consistent replenishment, thereby contributing significantly to overall market revenue. Their high turnover rate and necessity in both clinical and farm settings further reinforce their dominant position in the market.

By animal type, the bovine segment emerged as the top contributor, accounting for 54.7% of the total market share in 2024. This segment benefits from the substantial global demand for dairy and beef products, which has led to the large-scale adoption of artificial insemination techniques in cattle breeding. The consistent emphasis on improving herd genetics and enhancing traits like milk production and disease resistance has made AI a preferred method in this segment. Large cattle populations and organized dairy operations further contribute to the segment's leading share.

Based on technique, the intratubal insemination segment is projected to witness strong growth, reaching USD 6.5 billion by 2034. This technique involves placing semen directly into the fallopian tubes, allowing for improved fertilization success, especially in cases where conventional approaches may not be as effective. Advances in catheter design and insemination tools are enhancing the accessibility and precision of this method, increasing its adoption among breeders aiming for high reproductive efficiency.

When analyzed by end use, in 2024, veterinary clinics and hospitals held the largest share and are expected to grow at a 7.7% CAGR through 2034. These facilities provide specialized reproductive services, and their ability to handle complex procedures, aided by modern medical equipment and skilled veterinary staff, makes them an essential part of the AI ecosystem. Increased awareness of fertility management and the rising preference for professional care also contribute to their strong market presence.

Regionally, North America led the global market in 2024 with a 34.2% share. The United States alone accounted for USD 1.87 billion in 2024, growing from USD 1.79 billion in 2023. This growth reflects the country's advanced veterinary infrastructure and its strong adoption of modern breeding technologies, which support high livestock productivity.

The competitive landscape of the animal artificial insemination market is characterized by the presence of a mix of established global companies and smaller regional firms. Four leading players- IMV Technologies,Genus Plc, URUS Group, and CRV Holdings B.V.-collectively held around 48% of the global market in 2024. These companies are heavily investing in product innovation, technological upgrades, and strategic collaborations to maintain their competitive edge. Meanwhile, local manufacturers continue to intensify competition by offering cost-effective solutions and expanding their geographic presence through mergers and product launches.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Animal type

- 2.2.4 Technique

- 2.2.5 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for higher reproductive efficiency compared to natural mating

- 3.2.1.2 Increasing demand for enhanced genetics in both livestock and companion animals

- 3.2.1.3 Technological advancements in semen collection and preservation techniques

- 3.2.1.4 Rising prevalence of sexually transmitted diseases among animals

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risk of procedural failures and complications

- 3.2.2.2 Lack of skilled technicians

- 3.2.2.3 Regulatory and ethical concerns

- 3.2.2.4 High set-up and equipment cost

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for genetic improvement in livestock

- 3.2.3.2 Growing adoption of artificial intelligence in developing countries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Services

- 5.3 Semen

- 5.3.1 Normal semen

- 5.3.2 Sexed semen

- 5.4 Instruments

- 5.5 Kits and consumables

Chapter 6 Market Estimates and Forecast, By Animal Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Bovine

- 6.3 Swine

- 6.4 Ovine

- 6.5 Caprine

- 6.6 Equine

- 6.7 Other animal types

Chapter 7 Market Estimates and Forecast, By Technique, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Intratubal insemination

- 7.3 Intrauterine insemination

- 7.4 Intracervical insemination

- 7.5 Intrauterine tuboperitoneal insemination

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary clinics and hospitals

- 8.3 Animal breeding centers

- 8.4 Research institutes and universities

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Bovine Elite

- 10.2 CRV Holdings

- 10.3 Geno SA

- 10.4 Genus Plc

- 10.5 IMV Technologies

- 10.6 Minitube Group

- 10.7 SEMEX

- 10.8 Select Sires

- 10.9 Swine Genetics International

- 10.10 Shipley Swine Genetics

- 10.11 Stallion AI Services

- 10.12 STgenetics

- 10.13 URUS Group

- 10.14 VikingGenetics