PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1773249

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1773249

Centrifugal Blower Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

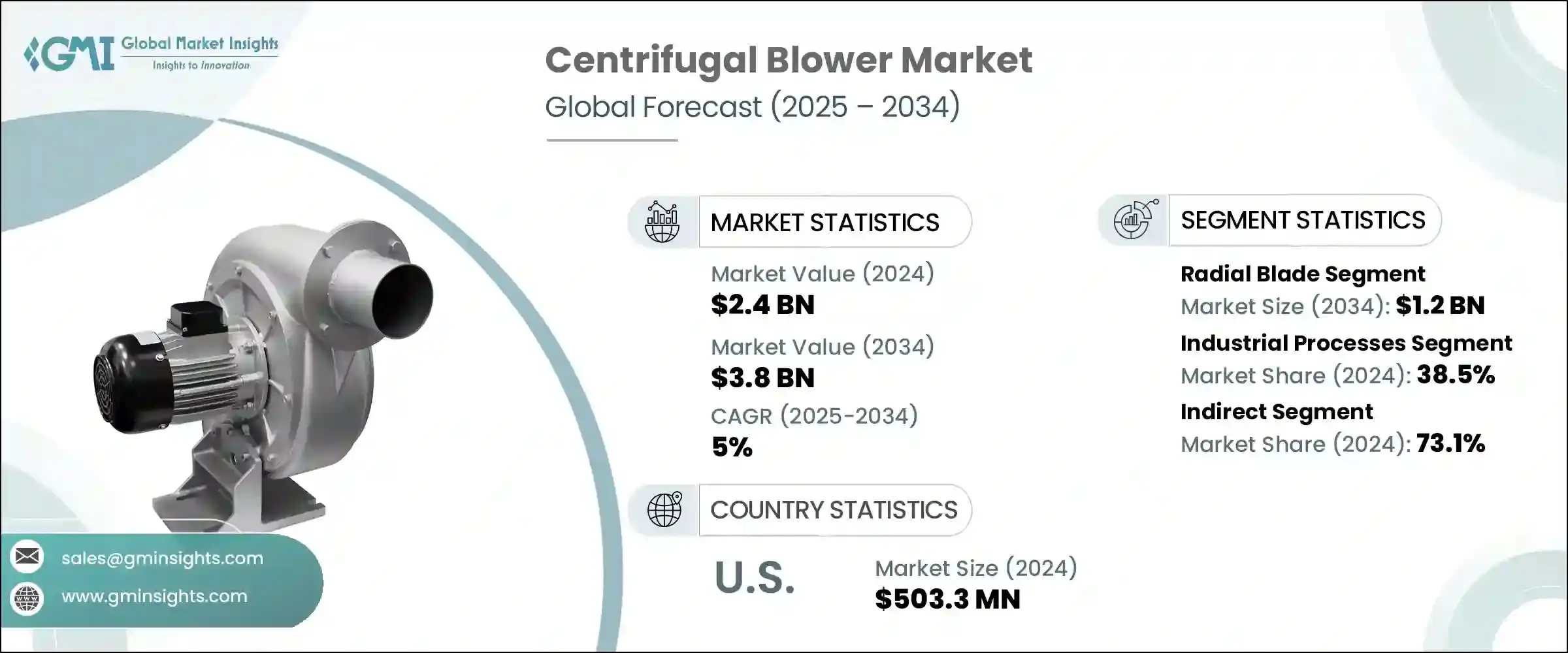

The Global Centrifugal Blower Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 5% to reach USD 3.8 billion by 2034. The market's growth trajectory is closely tied to rising demand from industries such as automotive, HVAC, chemical processing, and power generation. Centrifugal blowers are key components in systems that move air and gas, including ventilation, cooling, and pneumatic conveying systems.

The surge in the adoption of these blowers is largely attributed to innovations that enhance energy efficiency, reduce environmental impact, and extend operational life. The introduction of advanced blower models designed with smart technologies is supporting modern manufacturing initiatives, particularly those aligned with Industry 4.0, which emphasize automation, productivity, and data-driven efficiency. With industries actively seeking solutions to reduce their energy consumption and carbon footprint, energy-efficient blowers have become central to operational strategies. These blowers not only support industrial sustainability goals but also help lower utility expenses in energy-intensive sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $3.8 Billion |

| CAGR | 5% |

In sectors like mining and power generation, the role of centrifugal blowers extends beyond airflow control to include critical safety functions. They help maintain clean air zones in hazardous work environments and ensure the smooth operation of sensitive equipment. With increasing regulatory pressures and rising awareness about workplace safety and environmental standards, the demand for reliable and durable blowers is accelerating. Centrifugal blowers are being increasingly integrated into core operations as companies strive to meet compliance requirements and enhance risk mitigation strategies.

The food and beverage sector is another key contributor to centrifugal blower adoption. These systems support high levels of sanitation and hygiene, which are crucial in food processing environments. As global demand for packaged and processed foods continues to rise, the need for air filtration and odor control systems within processing lines is growing. Centrifugal blowers offer precise airflow control, making them ideal for supporting cleanroom environments and air purification systems required in food manufacturing. The continued expansion of automation and programmable systems within food production is also boosting the market for advanced blower configurations.

By type, radial blade centrifugal blowers dominated the market in 2024 with a valuation of USD 788.5 million and are estimated to reach USD 1.2 billion by 2034. This segment remains the top choice due to its effective airflow performance, adaptability across various sectors, and ongoing improvements in design that optimize energy consumption. As industries increasingly demand solutions that combine operational performance with energy savings, the radial blade configuration continues to gain traction across applications.

In terms of application, centrifugal blowers used in industrial processes accounted for approximately 38.5% of the global market share in 2024 and are projected to register a CAGR of 5.4% from 2025 to 2034. These blowers are vital to several key functions, such as air combustion, material handling, and exhaust systems. Their ability to withstand harsh environments and deliver consistent performance makes them indispensable in manufacturing, refining, and heavy industrial operations. The growing emphasis on improving process efficiency and reducing downtime has led to the wider adoption of centrifugal blowers in industrial systems.

Looking at the distribution landscape, the indirect sales channel held a dominant share of nearly 73.1% in 2024. Distributors play a pivotal role in market expansion, offering manufacturers access to a wider customer base and enabling faster product availability across regions. These intermediaries often provide post-sale support, technical assistance, and product servicing, which enhances customer satisfaction and fosters repeat business. Strategic collaborations between manufacturers and distribution partners continue to shape the market, reinforcing the strength of indirect sales in this sector.

Regionally, the United States recorded a market value of USD 503.3 million in 2024 and is expected to grow at a CAGR of 4.5% over the forecast period. The country's well-established industrial ecosystem, which includes manufacturing, petrochemical, and HVAC sectors, provides a solid foundation for centrifugal blower demand. Access to a mature logistics infrastructure and a broad network of distribution channels ensures that advanced blower systems are readily available nationwide, supporting a steady uptick in domestic consumption.

The centrifugal blower market features a mix of prominent global manufacturers and region-focused suppliers. Key players in the space include Airmake Cooling Systems, Aerotech Equipment, Alfotech Fans, Atlas Copco, Atlantic Blowers LLC, Chuan-Fan Electric Co., Ltd., Colfax Corporation, CLEANTEK, Elektror Airsystems, HIS Blower, Illinois Blower Inc., EVG Engicon Airtech Pvt. Ltd., Kaeser Kompressoren, The New York Blower Company, Shandong Huadong Blower Co., Ltd., The Spencer Turbine Company, Trimech India, and Vishwakarma Air Systems. The competitive landscape remains moderately fragmented, which encourages ongoing innovation and competitive pricing strategies. While some entry barriers exist due to technical requirements and capital investments, the environment remains conducive for new entrants and niche players focusing on custom or region-specific solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Driving mechanism

- 2.2.4 Pressure

- 2.2.5 Application

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory framework

- 3.7.1 Standards and certifications

- 3.7.2 Environmental regulations

- 3.7.3 Import export regulations

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's five forces analysis

- 3.10 PESTEL analysis

- 3.11 Consumer behavior analysis

- 3.11.1 Purchasing patterns

- 3.11.2 Preference analysis

- 3.11.3 Regional variations in consumer behavior

- 3.11.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New Product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Radial blade

- 5.3 Forward-curved

- 5.4 Backwards curved

- 5.5 Mixed flow

- 5.6 Axial flow

- 5.7 Multi-stage

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Drive Mechanism, 2021 - 2034, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Direct drive

- 6.3 Belt drive

Chapter 7 Market Estimates & Forecast, By Pressure, 2021 - 2034, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 High

- 7.3 Medium

- 7.4 Low

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 HVAC

- 8.3 Industrial processes

- 8.4 Power generation

- 8.5 Pharmaceutical

- 8.6 Food processing

- 8.7 Mining

- 8.8 Agriculture

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Malaysia

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 11.1 Aerotech Equipments and Projects Pvt. Ltd

- 11.2 Airmake Cooling Systems

- 11.3 Alfotech Fans

- 11.4 Atlantic Blowers LLC

- 11.5 Atlas Copco

- 11.6 Chuan-Fan Electric Co., Ltd.

- 11.7 CLEANTEK

- 11.8 Colfax Corporation

- 11.9 Elektror Airsystems

- 11.10 EVG Engicon Airtech Pvt. Ltd.

- 11.11 HIS Blower

- 11.12 Illinois Blower Inc.

- 11.13 Kaeser kompressoren

- 11.14 Shandong Huadong Blower Co., Ltd.

- 11.15 The New York Blower Company

- 11.16 The Spencer Turbine Company

- 11.17 Trimech India

- 11.18 Vishwakarma Air Systems