PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1773264

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1773264

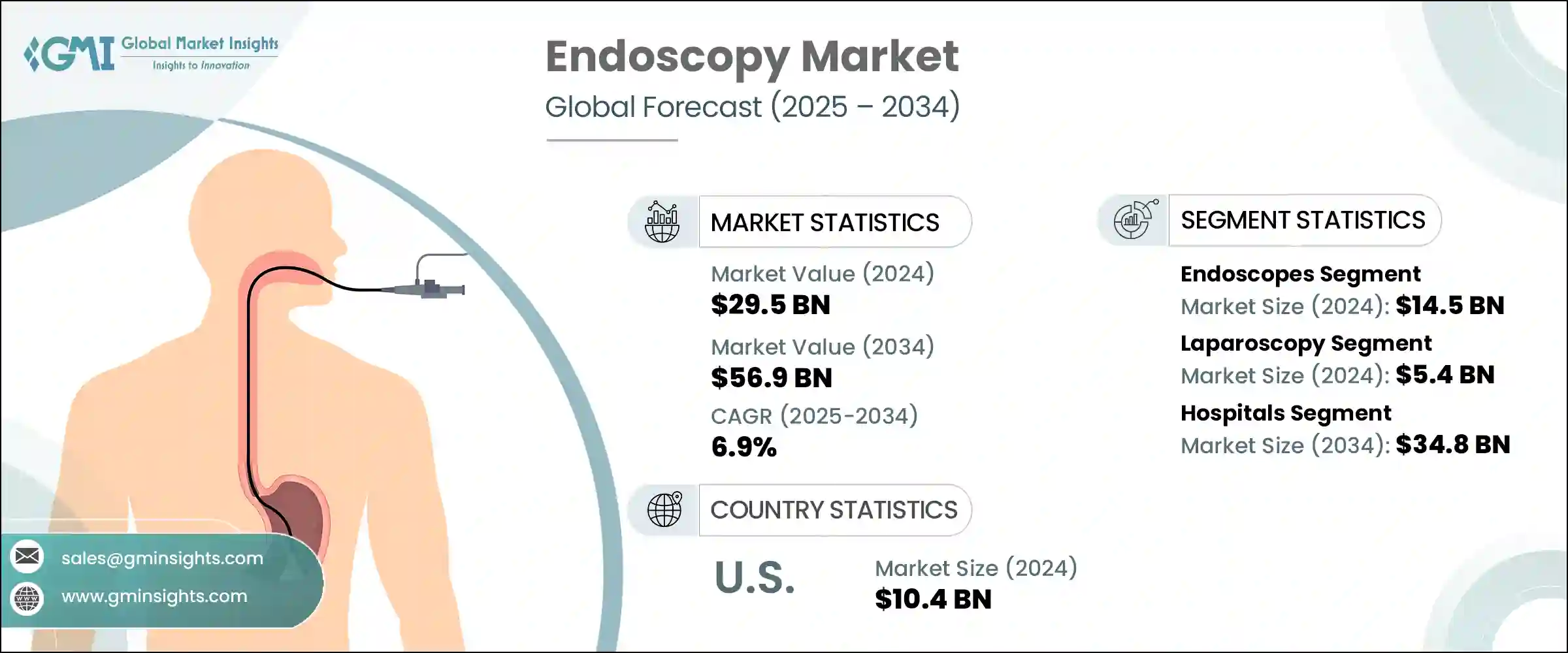

Endoscopy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

The Global Endoscopy Market was valued at USD 29.5 billion in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 56.9 billion by 2034. Market growth is being shaped by a combination of medical advancements, changing healthcare priorities, and rising disease burdens across the globe. The rising demand for less invasive treatment options and increased utilization of endoscopy for both diagnostic and therapeutic purposes are contributing significantly to market expansion. The market is witnessing consistent momentum due to growing healthcare spending, aging populations, and the rising incidence of chronic and gastrointestinal illnesses worldwide. Moreover, a shift toward early diagnosis and the growing focus on preventive care have led to higher adoption of endoscopic procedures in both public and private healthcare settings. Healthcare systems across the globe are investing in advanced endoscopic technologies that support accurate diagnostics, faster patient recovery, and lower hospitalization costs.

In 2024, the endoscopes segment accounted for the highest market share, generating USD 14.5 billion in revenue. The demand for high-performance imaging and procedural tools continues to accelerate, driven by improvements in visual clarity, maneuverability, and integration of smart features like robotics and AI. These technological advancements are transforming how physicians perform internal examinations, enabling quicker and more precise diagnoses. Compact, flexible, and lightweight endoscopes are now preferred by specialists for reaching anatomical areas that were previously inaccessible. Enhanced usability, reduced patient discomfort, and superior clinical outcomes are strengthening the position of endoscopes in routine practice.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $29.5 Billion |

| Forecast Value | $56.9 Billion |

| CAGR | 6.9% |

Another contributing factor is the growing preference for single-use and disposable endoscopic tools, which are becoming popular in outpatient and ambulatory settings. These devices help limit the risk of infection and eliminate the need for complex sterilization processes. Single-use endoscopes, in particular, are gaining traction in bronchoscopy and urology due to their cost-efficiency and ability to improve safety for both patients and practitioners.

The rising global burden of cancer, particularly gastrointestinal and colorectal cancers, is driving the need for endoscopic procedures as a frontline solution for detection, monitoring, and treatment. Endoscopic techniques are widely used for tumor removal, biopsy collection, and condition tracking. As awareness about the benefits of early cancer diagnosis grows, the demand for advanced endoscopy solutions continues to surge.

Among the various applications, laparoscopy held a market value of USD 5.4 billion in 2024 and is projected to grow at a CAGR of 6.5% between 2025 and 2034. Minimally invasive techniques like laparoscopy are gaining broader acceptance due to their association with shorter hospital stays, lower surgical trauma, and faster recovery periods. Patients and surgeons alike are showing a clear preference for these approaches in procedures ranging from gallbladder removal to bariatric surgeries. With the increasing rate of obesity worldwide, the number of weight-loss surgeries is rising, further supporting the demand for laparoscopic instruments. As more practitioners receive training in laparoscopy through simulation programs and partnerships with device manufacturers, the availability of skilled professionals is improving, which further drives adoption on a global scale.

In terms of end users, hospitals held the dominant position in 2024 and are projected to reach USD 34.8 billion by 2034. Hospitals are increasingly equipped with state-of-the-art endoscopic systems to meet the rising demand for diagnostics and surgical procedures. These institutions benefit from policy incentives and insurance coverage that promote the adoption of endoscopy for early disease detection, especially in cases of gastrointestinal and cancer screenings. Hospitals are continuously upgrading their infrastructure to enhance patient outcomes while optimizing operational costs. Endoscopy procedures, which reduce the need for extended hospital stays, align well with this objective. Investments in staff training and technology updates ensure that hospitals maintain high standards of care while adapting to the latest developments in endoscopic procedures.

The endoscopy market in the United States has shown consistent growth, rising from USD 9.2 billion in 2021 to USD 10.4 billion in 2024. It is expected to grow at a CAGR of 6.1% from 2025 to 2034. The high prevalence of chronic diseases and the need for precise diagnostic tools are major drivers behind this growth. An increasing number of patients are being diagnosed with gastrointestinal disorders, prompting the need for more advanced and less invasive solutions. The U.S. market continues to evolve as healthcare providers seek to improve procedural outcomes while maintaining cost efficiency.

The competitive landscape is defined by innovation, partnerships, and product diversification. Companies like Stryker Corporation, Olympus Corporation, Boston Scientific, Karl Storz, and Medtronic command approximately 42%-45% of the market share. These industry leaders are actively investing in next-gen endoscopic platforms that integrate AI, robotics, and advanced imaging to elevate clinical performance. Strategic collaborations and acquisitions remain key tactics for broadening global reach and strengthening their position in the evolving medical device landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing geriatric population globally

- 3.2.1.2 Introduction of technologically advanced endoscopes

- 3.2.1.3 Rising incidences of gastrointestinal disorders, cancer and other chronic conditions

- 3.2.1.4 Increasing demand for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Dearth of skilled physicians and endoscopists in developing countries

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for disposable or single-use endoscopes

- 3.2.3.2 Surge in integrated AI and data analytics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Reimbursement scenario

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Gap analysis

- 3.9 Value chain analysis

- 3.10 Future market trends

- 3.11 Technology and innovation landscape

- 3.11.1 Current technological trends

- 3.11.2 Emerging technologies

- 3.12 Patent Landscape

- 3.13 Consumer behaviour analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 By Region

- 4.3.1.1 North America

- 4.3.1.2 Europe

- 4.3.1.3 Asia Pacific

- 4.3.1 By Region

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers and acquisitions

- 4.7.2 Partnerships and collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Endoscopes

- 5.2.1 Rigid endoscopes

- 5.2.2 Flexible endoscopes

- 5.2.3 Capsule endoscopes

- 5.3 Visualization systems

- 5.4 Endoscopic ultrasound

- 5.5 Insufflator

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Laparoscopy

- 6.3 GI endoscopy

- 6.3.1 Gastroscopy

- 6.3.2 Colonoscopy

- 6.3.3 Sigmoidoscopy

- 6.3.4 Duodenoscopy

- 6.3.5 Other GI endoscopies

- 6.4 Arthroscopy

- 6.5 ENT endoscopy

- 6.6 Pulmonary endoscopy

- 6.7 Obstetrics/Gynecology

- 6.8 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 B Braun

- 9.2 Boston Scientific

- 9.3 CONMED

- 9.4 COOK MEDICAL

- 9.5 FUJIFILM

- 9.6 HOYA

- 9.7 INTUITIVE

- 9.8 Johnson & Johnson

- 9.9 KARL STORZ

- 9.10 Medtronic

- 9.11 OLYMPUS

- 9.12 RICHARD WOLF

- 9.13 Smith & Nephew

- 9.14 Stryker