PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1773341

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1773341

Industrial Inkjet Printers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

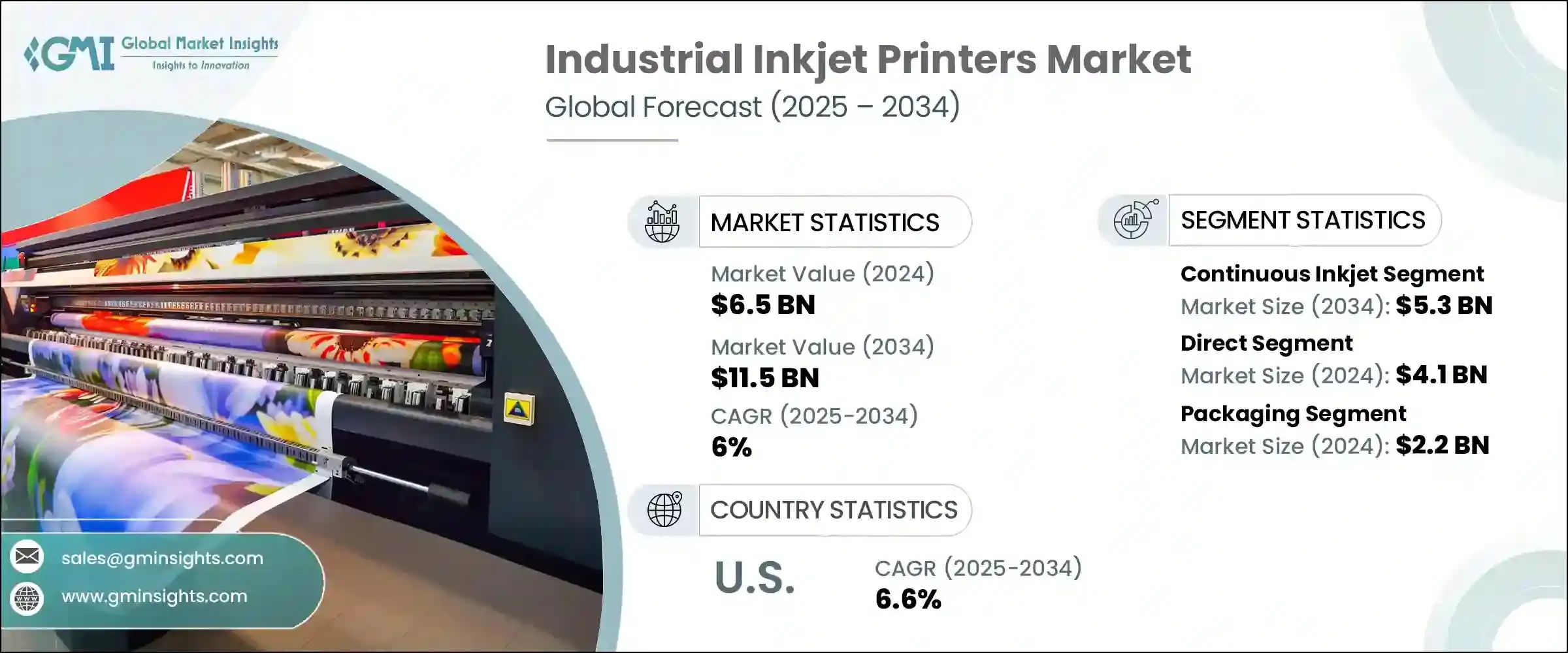

The Global Industrial Inkjet Printers Market was valued at USD 6.5 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 11.5 billion by 2034. Industries such as pharmaceuticals, textiles, and packaging are significantly boosting the demand for variable data printing, particularly for real-time labeling with barcodes, dates, serial numbers, and batch codes across diverse materials. This growth is fueled by consumer expectations for product personalization, stricter regulatory standards, and brand differentiation in competitive markets.

Inkjet systems offer a flexible and cost-effective solution for high-resolution printing on short-run jobs without the need for costly retooling, which is attracting growing adoption among end-users. Furthermore, sustainability is gaining momentum, especially with the emphasis from the U.S. Environmental Protection Agency (EPA) on reducing waste and improving energy efficiency. As a result, more companies are turning to inkjet printing as an environmentally responsible and productive alternative.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.5 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 6% |

Technological advancements, especially in printhead design, digital ink formulations, and integration with Industry 4.0 platforms, are significantly enhancing the performance of inkjet printers. These improvements allow for ultra-high-resolution outputs, benefiting specialized applications like decorative packaging, film labeling, and custom materials by leveraging features such as micro-droplet control and increased pixel accuracy. Additionally, industrial inkjet technology has found a place in additive manufacturing, particularly binder jetting, which is proving to be a viable method in 3D printing across various sectors, including biomedical, aerospace, and automotive. The potential return on investment continues to increase as these machines evolve, solidifying their role in modern production environments.

The continuous inkjet (CIJ) segment accounted for USD 2.9 billion in 2024 and is expected to rise to USD 5.3 billion by 2034. This segment leads the market due to its ability to perform high-speed, non-contact printing with minimal maintenance requirements. Its durability and ability to deliver consistent output in demanding settings make it a popular choice for businesses that rely on printing variable information such as expiration dates and tracking codes on a variety of substrates. With strong adhesion properties and seamless operation even under challenging industrial conditions, CIJ systems continue to maintain a strong market position.

The direct sales segment accounted for USD 4.1 billion in 2024 and is anticipated to grow at a CAGR of 6.1% during 2025-2034. Industrial applications that demand a high degree of customization and technical complexity primarily drive this segment. Leading manufacturers such as Epson, Markem-Imaje, Domino Printing Sciences, and Videojet have strengthened their market approach by building direct relationships with clients. These companies provide personalized services, including system setup, real-time technical support, maintenance agreements, and full integration with existing workflows, ensuring long-term client retention and satisfaction.

North America Industrial Inkjet Printers Market was valued at USD 900 million in 2024 and is projected to grow at a CAGR of 6.6% between 2025 and 2034. The dominance of the U.S. stems from its well-established and technologically advanced manufacturing ecosystem. Inkjet systems are widely adopted for marking, coding, and labeling processes within various sectors such as electronics, food production, and pharmaceuticals. These systems integrate efficiently into existing automation setups, significantly boosting throughput while minimizing downtime. Ongoing research and development efforts by industry leaders continue to enhance the performance, durability, and operational efficiency of industrial inkjet technologies.

Key players shaping the competitive landscape of the Industrial Inkjet Printer Industry include Canon, Fujifilm, Durst Phototechnik, HP, Brother Industries, Konica Minolta, Epson, Hitachi Industrial Equipment Systems, Mitsubishi Heavy Industries Printing & Packaging Machinery, Electronics For Imaging, Keyence, Leibinger Group, and Domino Printing Sciences.

To strengthen their market position, leading companies in the industrial inkjet printers industry are focusing on direct client engagement, enabling tailored solutions, and offering full-service packages including maintenance, training, and integration. Many are investing heavily in R&D to advance printhead technology, ink chemistry, and sustainable practices to align with regulatory requirements and customer expectations. Strategic collaborations and acquisitions are also common, helping to expand product portfolios and access new regional markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 End use industry

- 2.2.4 Distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory framework

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's five forces analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 MEA

- 4.2.1.5 LATAM

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Technology, 2021-2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Continuous inkjet

- 5.3 Drop on demand

- 5.4 UV inkjet

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By End Use Industry, 2021-2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Food & beverage

- 6.3 Chemical

- 6.4 Pharmaceutical

- 6.5 Packaging

- 6.6 Personal care & cosmetics

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021-2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Direct sales

- 7.3 Indirect sales

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034, ($Bn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 The U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 South Africa

Chapter 9 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 9.1 Brother Industries

- 9.2 Canon

- 9.3 Domino Printing Sciences

- 9.4 Durst Phototechnik

- 9.5 Electronics For Imaging

- 9.6 Epson

- 9.7 Fujifilm

- 9.8 Hitachi Industrial Equipment Systems

- 9.9 HP

- 9.10 Keyence

- 9.11 Konica Minolta

- 9.12 Leibinger Group

- 9.13 Markem-Imaje

- 9.14 Mitsubishi Heavy Industries Printing & Packaging Machinery

- 9.15 Videojet