PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1773375

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1773375

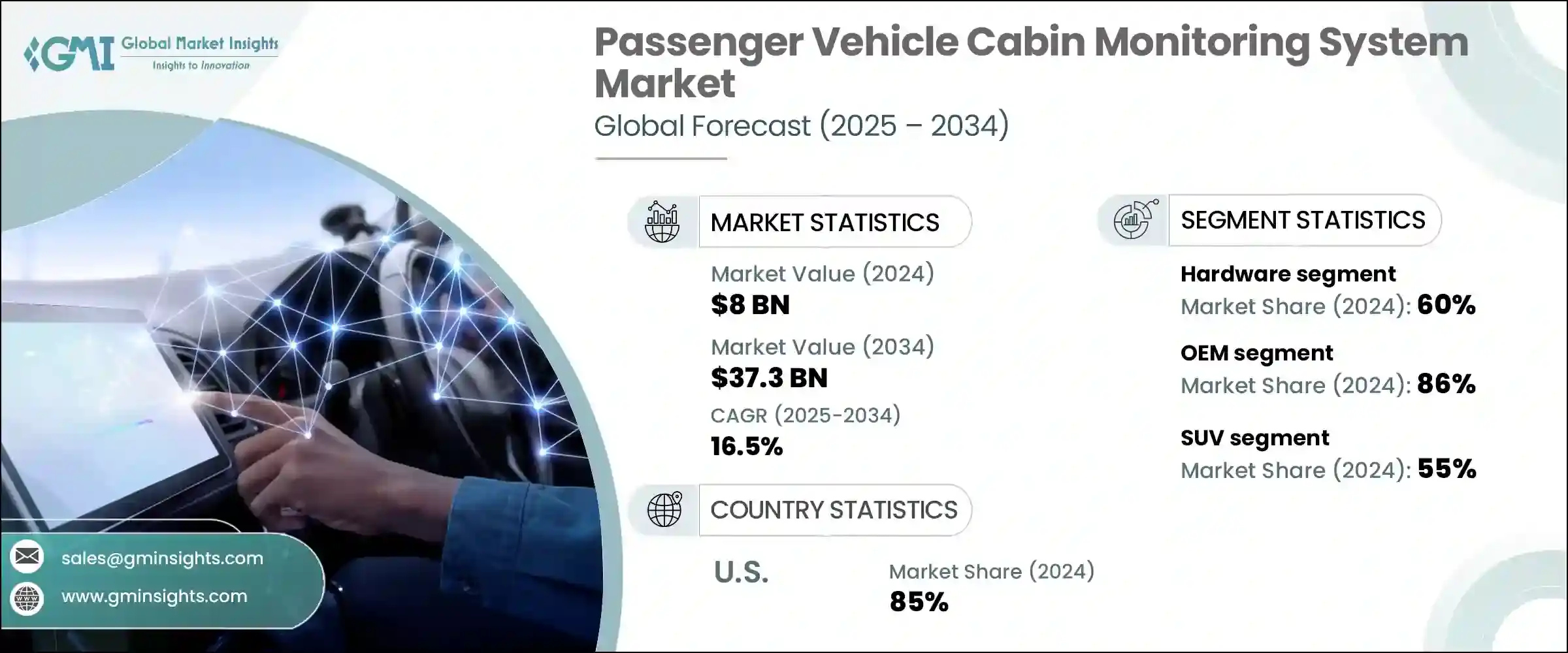

Passenger Vehicle Cabin Monitoring System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

The Global Passenger Vehicle Cabin Monitoring System Market was valued at USD 8 billion in 2024 and is estimated to grow at a CAGR of 16.5% to reach USD 37.3 billion by 2034. The rising focus on occupant safety, comfort, and smart in-cabin technology by both car manufacturers and consumers is a key driver of this growth. As vehicles become increasingly autonomous, the integration of cabin monitoring systems-including vital sign detection, occupant identification, and driver monitoring-is becoming standard in modern car designs.

These systems rely on a mix of sensors and AI-powered algorithms to monitor driver alertness, detect passengers, and even analyze biometric data, supporting functions such as drowsiness alerts, adaptive airbag deployment, and emergency interventions. With regulatory agencies in major automotive markets mandating advanced safety features and buyers showing strong demand for personalized and proactive cabin experiences, the market for intelligent cabin monitoring solutions is poised for rapid growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8 Billion |

| Forecast Value | $37.3 Billion |

| CAGR | 16.5% |

These systems have moved beyond the concept stage to become essential in identifying occupants, assessing driver attention, and ensuring child safety, solidifying their role in everyday vehicles. What was once viewed as a premium or futuristic feature is now becoming a standard requirement, driven by both regulatory mandates and shifting consumer expectations. Advanced cabin monitoring systems are now integrated to detect vital signs, monitor fatigue levels, and respond to emergencies in real-time, enhancing both convenience and in-vehicle security. They also support intelligent functions like automatic climate adjustment based on occupancy and biometric-based personalization.

In 2024, the hardware segment held a 60% share and is forecasted to grow at a CAGR of 16% during 2025-2034. Hardware remains the cornerstone of cabin monitoring systems in passenger vehicles, consisting of cameras, radar sensors, infrared modules, and embedded electronics. As automakers focus on smarter interiors, the need for robust and responsive hardware is critical. These components provide the real-time data necessary to fuel AI algorithms that track driver vigilance, passenger presence, and biometric indicators, making them indispensable for system performance.

The OEM segment held an 86% share in 2024, driven by the automotive industry's push toward sensor-enabled, factory-installed safety solutions. Vehicle manufacturers increasingly opt to integrate cabin and driver monitoring systems directly during production, ensuring seamless compatibility with other in-car technologies like climate control, ADAS, and infotainment systems. OEM installation enhances system accuracy, reliability, and consumer trust, making it the preferred method of delivery in this market.

North America Passenger Vehicle Cabin Monitoring System Market held an 85% share and generated USD 2.4 billion in 2024. The country leads adoption due to a mature automotive sector, stringent safety standards, and a strong appetite for innovation. Automakers are proactively incorporating features such as biometric tracking, occupant detection, and fatigue monitoring as standard across new vehicle models. This demand, combined with regulatory support, positions the U.S. as a dominant force in this segment.

Prominent companies in the Passenger Vehicle Cabin Monitoring System Industry include Magna International Inc., Panasonic Corporation, Robert Bosch GmbH, Continental AG, Valeo S.A., Denso Corporation, and Visteon Corporation. To strengthen their foothold in the passenger vehicle cabin monitoring system market, companies are adopting several key strategies. Innovation is at the forefront, with significant investment in research and development to advance sensor accuracy, AI capabilities, and system integration with vehicle architectures. Collaborations and strategic partnerships with automakers accelerate the adoption of new technologies and help tailor solutions to specific OEM needs. Companies are also focusing on expanding their global reach through localized production and customer support to serve diverse markets. Enhancing cybersecurity features and improving system reliability are prioritized to build consumer confidence in safety systems.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Technology

- 2.2.5 Sales channel

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing global adoption of electric vehicles supported by government incentives

- 3.2.1.2 Advancements in lightweight and smart bearing technologies improve efficiency and durability

- 3.2.1.3 Expansion of EV manufacturing in emerging markets

- 3.2.1.4 Integration of predictive maintenance through sensor-enabled bearings

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial costs

- 3.2.2.2 Complex installation and maintenance

- 3.2.3 Market opportunities

- 3.2.3.1 Surging global EV production

- 3.2.3.2 R&D and co-development with OEMs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By component

- 3.10 Production statistics

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.10.3 Export and import

- 3.11 Cost breakdown analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Cameras

- 5.2.2 Sensors

- 5.2.3 Display Units

- 5.2.4 Control Units

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Hatchback

- 6.3 Sedan

- 6.4 SUV

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Driver monitoring system

- 7.2.1 Eye-Tracking

- 7.2.2 Facial recognition

- 7.2.3 Head position monitoring

- 7.2.4 Drowsiness detection

- 7.2.5 Distraction detection

- 7.3 Occupant Monitoring System (OMS)

- 7.3.1 Occupant presence detection

- 7.3.2 Seat belt monitoring

- 7.3.3 Child detection

- 7.3.4 Passenger behavior analysis

- 7.4 Others

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEMs

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Camera based

- 9.3 Sensor based

- 9.4 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aptiv

- 11.2 Autoliv

- 11.3 Caaresys

- 11.4 Continental

- 11.5 Denso

- 11.6 Faurecia S.A.

- 11.7 Gentex

- 11.8 Harman International Industries, Inc.

- 11.9 Hyundai Mobis

- 11.10 Magna International

- 11.11 Omron

- 11.12 Panasonic

- 11.13 Robert Bosch

- 11.14 Seeing Machines

- 11.15 Smart Eye AB

- 11.16 Tobii

- 11.17 Valeo S.A.

- 11.18 Vayyar Imaging

- 11.19 Visteon

- 11.20 ZF Friedrichshafen