PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1773399

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1773399

Commercial Vehicle Diesel Engine Exhaust Valve Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

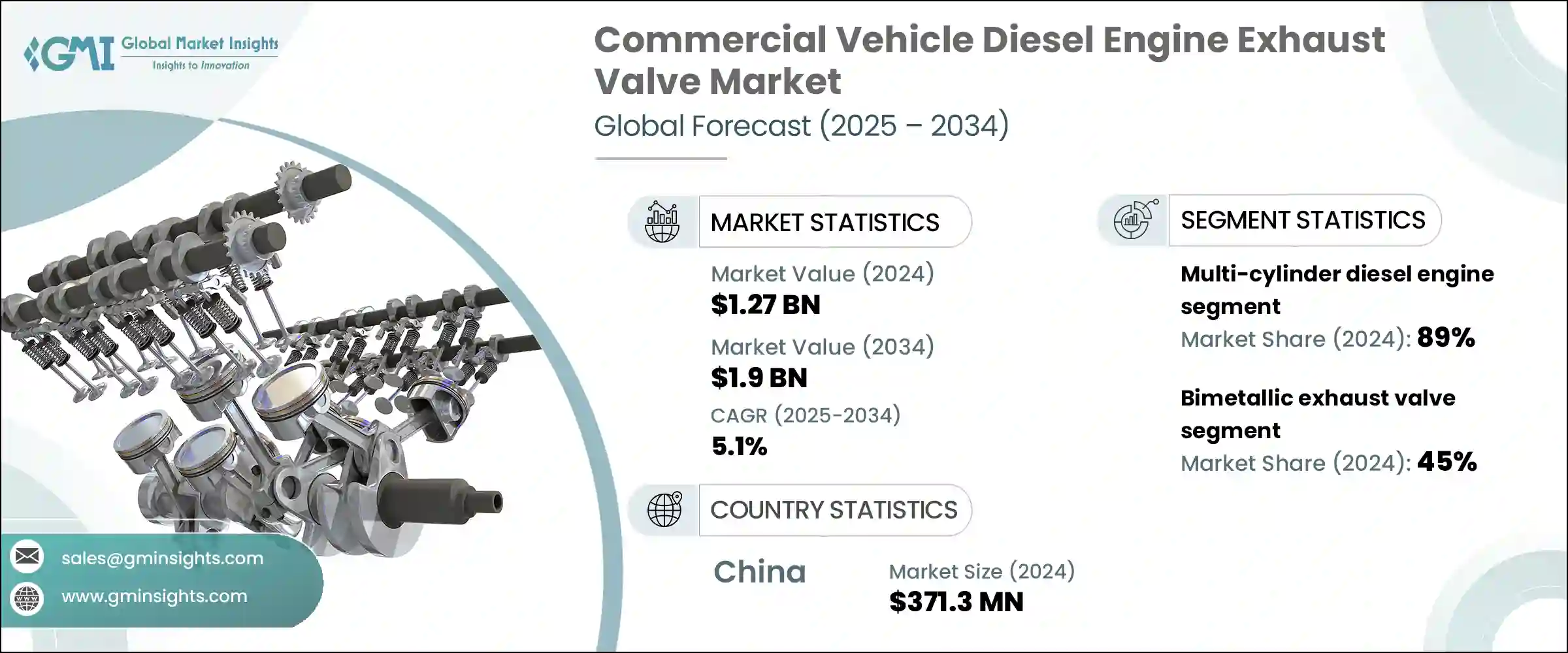

The Global Commercial Vehicle Diesel Engine Exhaust Valve Market was valued at USD 1.27 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 1.9 billion by 2034. The steady rise in commercial vehicle manufacturing and extended diesel engine lifespans are two of the most significant factors driving this market's growth. Diesel-powered trucks and buses remain the cornerstone of freight and construction operations, and exhaust valves are critical for maintaining efficient engine performance and emissions compliance. As these vehicles endure intense operational loads, robust exhaust valve systems are essential to ensure long-term durability, reduce engine wear, and uphold regulatory standards. With emission regulations tightening and uptime becoming more critical than ever, OEMs and fleet operators are turning to technologically advanced, heat-resistant valve solutions to meet evolving demands.

One of the key forces behind this market's expansion is the rapid increase in production of commercial vehicles globally. From delivery trucks to construction equipment, OEMs across North America, Asia, and parts of Europe are ramping up output to keep pace with rising logistics demand. These vehicles rely on exhaust valves that can withstand intense operating temperatures, pressure cycles, and mechanical stress over long distances. Manufacturers are now focused on developing high-durability valve components using advanced materials and design techniques that minimize failure rates and boost overall system efficiency. Dependable exhaust valve performance is directly tied to diesel engine health, which in turn affects downtime, fuel consumption, and emission output.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.27 Billion |

| Forecast Value | $1.9 Billion |

| CAGR | 5.1% |

In 2024, the multi-cylinder diesel engines segment accounted for 89% share and is forecast to grow at a CAGR of 5.2% from 2025 through 2034. Multi-cylinder engines dominate this space due to their prominent use in medium and heavy commercial vehicles, where durability, consistent power delivery, and engine balance are essential. These engines are built to manage extended operating hours and variable terrain conditions, and their performance heavily depends on precise exhaust valve feedback mechanisms. Proper valve control helps maintain combustion efficiency, improve emissions profiles, and reduce the risk of mechanical failure. These outcomes are vital for both OEMs developing next-gen trucks and fleet operators managing performance across thousands of vehicles.

The bimetallic exhaust valves segment held a 45% share in 2024 and is projected to register a CAGR of 6.7% during 2025-2034. These valves use two different metals-typically a heat-resistant alloy for the valve head and corrosion-resistant steel for the stem-to balance cost-efficiency and durability. They are especially suitable for commercial diesel engines due to their ability to endure both high temperatures and aggressive chemical exposure without compromising structural strength. Bimetallic valves offer superior resistance to oxidation, enable better thermal conductivity, and support prolonged engine cycles in the face of intensive work conditions. For fleets that prioritize operational efficiency and minimal unplanned maintenance, these valves deliver both performance and longevity.

China Commercial Vehicle Diesel Engine Exhaust Valve Market generated USD 371.3 million in 2024, representing a 57% share. China's dominance in the regional landscape stems from its massive commercial fleet, the enforcement of strict diesel emission standards, and the increased integration of digital technologies within powertrains. Leading Chinese OEMs are embedding sensor-enabled exhaust valves into diesel platforms to facilitate predictive maintenance, reduce emissions, and maintain compliance across high-volume operations. These technologies also enable better diagnostics and support cleaner combustion processes. The ongoing development of commercial transport infrastructure and regulatory enforcement further amplifies demand in this market.

Key players in the Global Commercial Vehicle Diesel Engine Exhaust Valve Market include Hitachi, Continental, Denso Corporation, Eaton Corporation, Knorr-Bremse AG, Mahle Group, and Sinotruck Engine Valve. These companies are adopting diverse approaches to strengthen their market position and adapt to evolving industry needs. To expand their market footprint, leading companies in this sector are investing heavily in R&D to engineer high-efficiency exhaust valves using advanced alloys and coating technologies. They are also forming long-term supply contracts with major OEMs to ensure consistent volume sales across global markets. A key strategic focus includes localizing production facilities near key demand zones, which allows for faster delivery and cost efficiency. Additionally, players are enhancing product portfolios with digital and sensor-integrated valve systems to meet the rising demand for predictive maintenance and emission monitoring.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 – 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Engine

- 2.2.3 Valve

- 2.2.4 Material Type

- 2.2.5 Sales Channel

- 2.2.6 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising commercial vehicle production

- 3.2.1.2 Growing diesel vehicle lifespan

- 3.2.1.3 Technological advancements in valve materials

- 3.2.1.4 Expansion of freight & logistics industry

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Shift toward electric and alternative fuel vehicles

- 3.2.2.2 High cost of advanced valve materials

- 3.2.3 Market opportunities

- 3.2.3.1 Aftermarket expansion in aging vehicle fleets

- 3.2.3.2 Surge in off-highway vehicle demand

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.8.1 Software development & licensing cost

- 3.8.2 Deployment & integration cost

- 3.8.3 Maintenance & support cost

- 3.8.4 Cybersecurity & compliance cost

- 3.8.5 Training & change management cost

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Use cases

- 3.12 Best-case scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Engine, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Single cylinder diesel engine

- 5.3 Multi-cylinder diesel engine

Chapter 6 Market Estimates & Forecast, By Valve, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Mono-metallic exhaust valve

- 6.3 Bimetallic exhaust valve

- 6.4 Hollow stem valve

- 6.5 Sodium-filled valve

Chapter 7 Market Estimates & Forecast, By Material Type, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Steel

- 7.3 Titanium

- 7.4 Nickel-based alloys

- 7.5 Other high-temperature alloys

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Transportation & logistics

- 9.3 Construction & mining

- 9.4 Agriculture

- 9.5 Public transportation

- 9.6 Emergency & utility services

- 9.7 Military & defense

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Anhui Yuxi Industrial

- 11.2 AVR Valves

- 11.3 Continental AG

- 11.4 Delphi Automotive AG

- 11.5 Denso Corporation

- 11.6 Eaton Corporation

- 11.7 Federal-Mogul Holding Corp

- 11.8 FTE Automotive

- 11.9 FUJI OOZX

- 11.10 Hitachi

- 11.11 Knorr-Bremse

- 11.12 Mahle Group

- 11.13 MS Motorservice International

- 11.14 Nanjing Shengpai Auto Parts

- 11.15 Riken Corporation

- 11.16 Shijiazhuang Advanced Valve

- 11.17 Sinotruck Engine Valve

- 11.18 Tenneco

- 11.19 TRW Automotive

- 11.20 Wuxi Volex Auto Parts