PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1773413

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1773413

Automotive Integrated Starter-Generator Units Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

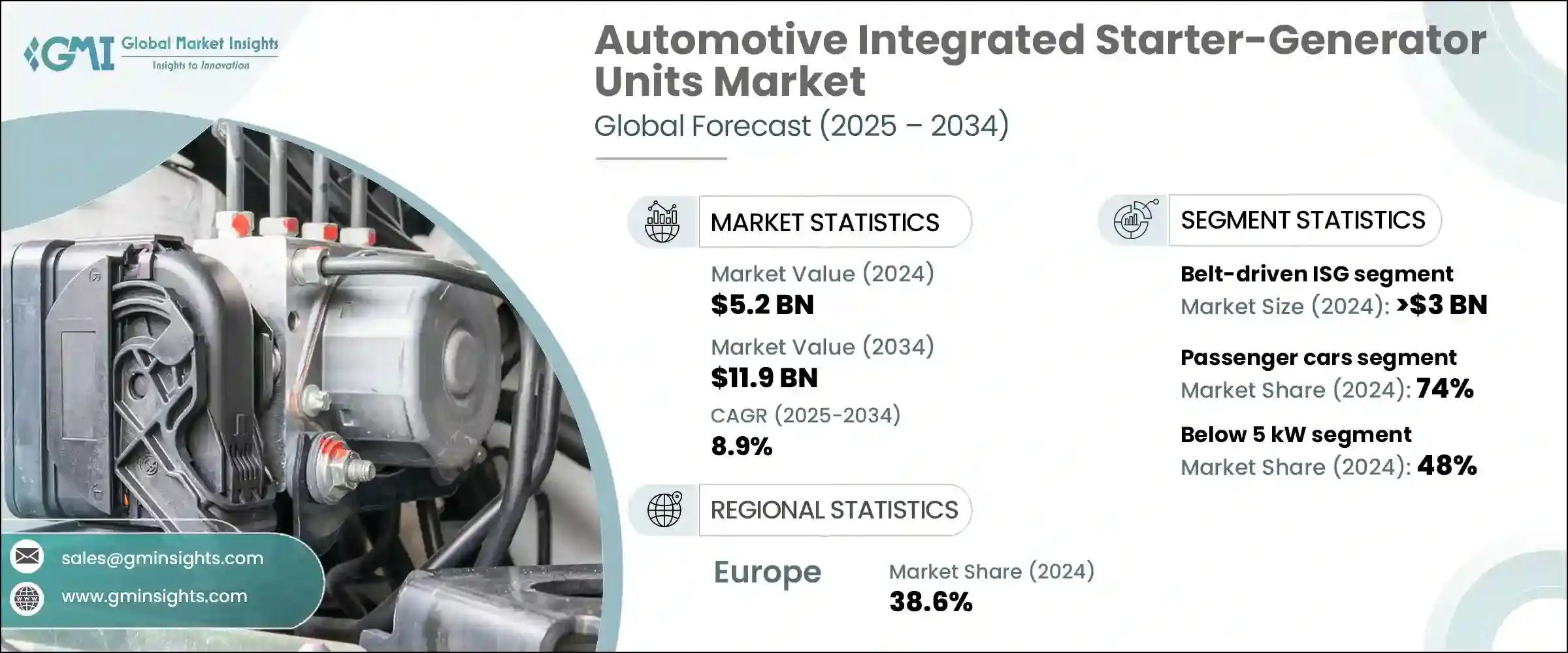

The Global Automotive Integrated Starter-Generator Units Market was valued at USD 5.2 billion in 2024 and is estimated to grow at a CAGR of 8.9% to reach USD 11.9 billion by 2034. This growth is largely fueled by rising demand for vehicles that offer both improved efficiency and reduced environmental impact. As global regulations surrounding emissions become stricter, automakers are ramping up the rollout of mild hybrid models that incorporate ISG technology. These systems are attractive to consumers seeking better fuel economy without the steep price tag associated with full or plug-in hybrids. ISG-equipped powertrains provide a middle ground-delivering noticeable fuel savings with minimal disruption to conventional vehicle designs.

The growing appetite for premium and performance vehicles is also accelerating the adoption of ISG units, as they contribute to smoother engine start-stop operations and deliver low-end torque improvements that enhance driving feel. This aligns perfectly with what high-end buyers want-efficiency without sacrificing power or luxury. As congestion increases in urban areas, demand for systems that reduce fuel use during idling and frequent stops has surged. ISG units help manage these challenges while also reducing emissions, making them a favored option in the push for smarter, greener urban transportation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.2 Billion |

| Forecast Value | $11.9 Billion |

| CAGR | 8.9% |

In 2024, the belt-driven ISG systems segment generated USD 3 billion, dominating the market by offering automakers a practical and cost-effective route to electrification. These units are mounted on the engine's front and connected via a belt to the crankshaft, allowing manufacturers to integrate them without redesigning major components. This streamlined integration is a major advantage for brands looking to electrify existing vehicle platforms quickly, saving both time and capital.

Mild hybrid-electric vehicles represented the largest market share in 2024 and are projected to remain a key growth area. These vehicles incorporate a compact battery and deliver performance benefits that drivers can immediately notice-from quiet operation during coasting to seamless engine restarts. The low-end torque boost improves drivability, particularly in stop-and-go traffic. Additionally, mild hybrids do not rely on external charging, making them ideal for consumers who want eco-friendly options without changing their driving habits. As a result, these systems are becoming more common across both commercial fleets and personal vehicles.

Germany Automotive Integrated Starter-Generator Units Market generated USD 496.7 million in 2024. The country's dominant position is supported by a mature automotive manufacturing base and early adoption of 48-volt systems across various vehicle classes. Leading manufacturers have aggressively implemented belt-driven ISG technology across their lineups to meet both regulatory demands and consumer expectations. Germany's robust supply chain, with major contributors such as Bosch, Continental, and ZF Friedrichshafen, further supports local production and innovation, helping the country maintain a competitive edge in the global ISG market.

Key players active in the Global Automotive Integrated Starter-Generator Units Market include Bosch, Mitsubishi Electric, Denso, BorgWarner, Magna International, ZF Friedrichshafen, SEG Automotive, Continental, Hitachi Astemo, and Valeo. To secure a leading position in the automotive ISG market, companies are focusing on several strategic areas. One core strategy involves investment in R&D to enhance performance, reduce weight, and improve the energy efficiency of ISG systems. Manufacturers are also targeting platform scalability to allow ISG integration across various vehicle categories. Collaborations with OEMs play a key role in customizing solutions for specific drivetrains. In addition, firms are strengthening their production capabilities through localized manufacturing to reduce lead times and comply with regional sourcing policies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Vehicle

- 2.2.4 Power rating

- 2.2.5 Propulsion type

- 2.2.6 Sales channel

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in demand for fuel efficiency

- 3.2.1.2 Stricter emission regulations worldwide

- 3.2.1.3 Cost-effective electrification solution

- 3.2.1.4 Growing demand in the luxury and mid-premium segment

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial integration cost for entry-level vehicles

- 3.2.2.2 Limited consumer awareness and perceived value

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of 48V mild hybrids in emerging markets

- 3.2.3.2 Commercial vehicle electrification

- 3.2.3.3 High-performance ISGs for premium/luxury vehicles

- 3.2.3.4 Aftermarket & retrofits for legacy fleets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Belt-driven ISG (B-ISG)

- 5.3 Crankshaft-mounted ISG

- 5.4 Dual-clutch transmission ISG

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedan

- 6.2.2 SUV

- 6.2.3 Hatchback

- 6.3 Commercial vehicles

- 6.3.1 LCVs (light commercial vehicles)

- 6.3.2 MCVs (medium commercial vehicles)

- 6.3.3 HCVs (heavy commercial vehicles)

Chapter 7 Market Estimates & Forecast, By Power rating, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Below 5 kW

- 7.3 5–10 kW

- 7.4 Above 10 kW

Chapter 8 Market Estimates & Forecast, By Propulsion type, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Mild hybrid electric vehicles (MHEVs)

- 8.3 Internal combustion engine (ICE) vehicles

Chapter 9 Market Estimates & Forecast, By Sales channel, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Malaysia

- 10.4.7 Singapore

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Aisin Corporation

- 11.2 BorgWarner

- 11.3 Bosch

- 11.4 Continental

- 11.5 Denso Corporation

- 11.6 Hitachi Astemo

- 11.7 Hyundai Mobis Co

- 11.8 Johnson Electric Holdings

- 11.9 Magna International

- 11.10 MAHLE Group

- 11.11 Mando Corporation

- 11.12 Mitsubishi Electric Corporation

- 11.13 Nidec Corporation

- 11.14 Prestolite Electric Incorporated

- 11.15 Schaeffler AG

- 11.16 SEG Automotive

- 11.17 Toyota Industries

- 11.18 Woory Industrial Co

- 11.19 Valeo

- 11.20 ZF Friedrichshafen