PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1782131

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1782131

Generative AI solution Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

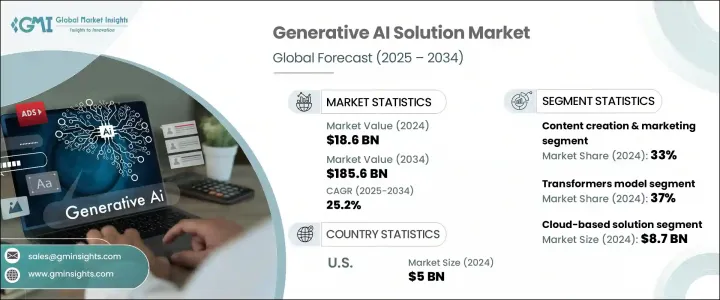

The Global Generative AI solution Market was valued at USD 18.6 billion in 2024 and is estimated to grow at a CAGR of 25.2% to reach USD 185.6 billion by 2034. The expansion is driven by increased demand for hyper-personalization, automation, and creative content generation across industries like media, healthcare, automotive, and enterprise software. Generative models, once confined to labs and creative niches-such as GANs, diffusion networks, and large language models-have become central to corporate innovation efforts. Traditional AI that followed rigid rules is being replaced by generative systems capable of producing human-like text, images, audio, and code. This evolution is driving efficiency, enhancing design processes, and enriching product experiences. Collaborations between application-focused firms and leading AI labs are accelerating adoption.

As a result, vertical-specific solutions tailored to distinct industry challenges are becoming the norm, signaling a shift towards sector-tailored AI implementations. This growing trend reflects a broader industry demand for precision, relevance, and real-world applicability, where one-size-fits-all models no longer meet complex operational needs. Organizations are increasingly prioritizing AI tools that align closely with their regulatory environments, data types, and customer expectations. From finance and healthcare to retail and manufacturing, these domain-optimized AI systems are enabling faster deployment, enhanced decision-making, and better return on investment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.6 Billion |

| Forecast Value | $185.6 Billion |

| CAGR | 25.2% |

The transformer-based models segment held a 37% share in 2024 and is expected to grow at a CAGR of 26% through 2034. These architectures underpin nearly all modern generative solutions, such as GPT, PaLM, LLaMA, and Claude. Their scalability, flexibility, and performance have enabled widespread adoption across industries. Transformers now power AI copilots in office software, code generation tools, and enterprise applications in sectors such as legal, finance, and marketing, cementing their position as the backbone of generative AI.

Content creation and marketing held a 33% share in 2024 and is forecast to grow at a CAGR of 25% from 2025 to 2034. Businesses increasingly rely on generative tools to produce SEO-optimized blog posts, ad campaigns, product descriptions, email content, and promotional multimedia at scale. These systems help marketers automate workflows while maintaining brand tone and delivering tailored messaging based on consumer insights. This shift is helping brands efficiently meet growing content demands, improve engagement, and optimize campaign performance.

U.S. Generative AI Solution Market held 85% share and generated USD 5 billion in 2024. This leadership stems from a rich tech infrastructure, advanced academic and corporate research environments, and substantial public-private investment. With major AI innovators headquartered in the U.S., supported by world-class universities, startups, and research hubs, the country remains at the forefront of generative transformer development and deployment at scale.

Leading firms in this market include Google, NVIDIA, Adobe, Amazon Web Services, Microsoft, IBM, and OpenAI. These companies are driving innovation and setting strategic direction for the industry. To solidify their market dominance, major players in the generative AI space are pursuing several core strategies. First, they are aggressively expanding R&D into next-generation architectures and multimodal models that fuse text, image, audio, and video capabilities. Second, partnerships with industry-specific leaders enable tailored solutions that meet vertical needs, from healthcare diagnostics to automotive design. Third, efforts to democratize AI access, such as offering open APIs, developer platforms, and freemium services, are widening user engagement and accelerating adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Application

- 2.2.4 Deployment

- 2.2.5 End use industry

- 2.2.6 Organization size

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Electronic component suppliers

- 3.1.1.2 Equipment manufacturers

- 3.1.1.3 Service providers

- 3.1.1.4 System integrators

- 3.1.1.5 End use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising enterprise demand for automation and efficiency

- 3.2.1.2 Hyper personalization in marketing and customer experience

- 3.2.1.3 Expansion of AI agents and Copilots across enterprise functions

- 3.2.1.4 Advancements in model capabilities

- 3.2.1.5 Cloud availability and strategic partnerships

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Hallucinations and inaccurate output

- 3.2.2.2 Data privacy and security risks

- 3.2.3 Market Opportunities

- 3.2.3.1 Vertical-specific large language models (LLMs)

- 3.2.3.2 Multimodal Generative AI solution (Text + Image + Audio + Video)

- 3.2.3.3 SaaS-based GenAI adoption among SMEs

- 3.2.3.4 AI-powered code generation & DevOps automation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology & innovation landscape

- 3.6.1 Current technologies

- 3.6.1.1 Transformer-based large language models (LLMs)

- 3.6.1.2 Generative adversarial networks (GANs)

- 3.6.1.3 Diffusion models

- 3.6.1.4 Variational autoencoders (VAEs)

- 3.6.2 Emerging technologies

- 3.6.2.1 Multimodal Generative AI solution

- 3.6.2.2 Retrieval-Augmented Generation (RAG) Systems

- 3.6.2.3 Low-Code/No-Code GenAI Development Platforms

- 3.6.2.4 Safety, Alignment & Evaluation Toolkits

- 3.6.1 Current technologies

- 3.7 Patent analysis

- 3.8 Regulatory landscape

- 3.8.1 North America

- 3.8.2 Europe

- 3.8.3 Asia Pacific

- 3.8.4 Latin America

- 3.8.5 Middle East & Africa

- 3.9 Cost breakdown analysis

- 3.10 Sustainability analysis

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Technology evolution and innovation roadmap

- 3.11.1 Foundation models and large language models (LLMs)

- 3.11.2 Multimodal AI systems

- 3.11.3 Specialized GENAI applications

- 3.11.4 Emerging technologies and future developments

- 3.12 Pricing models and monetization strategies

- 3.12.1 GenAI pricing model evolution

- 3.12.2 Subscription-based pricing analysis

- 3.12.3 Freemium and free tier strategies

- 3.12.4 Enterprise licensing and custom pricing

- 3.12.5 Revenue optimization and monetization trends

- 3.12.6 Pricing competitive analysis

- 3.12.7 Future pricing model evolution

- 3.13 Enterprise adoption and implementation

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Transformers model

- 5.2.1 Text generation

- 5.2.2 Code generation

- 5.2.3 Summarization

- 5.2.4 Question answering (Q&A)

- 5.2.5 Multimodal transformers (text+ image/video)

- 5.3 Generative adversarial networks (GAN)

- 5.3.1 Image generation

- 5.3.2 Video generation

- 5.3.3 Conditional

- 5.3.4 Super resolution

- 5.3.5 Style transfer

- 5.4 Diffusion models

- 5.4.1 Image synthesis

- 5.4.2 Video synthesis

- 5.4.3 Text-to-image diffusion

- 5.4.4 Inpainting/ editing tools

- 5.4.5 Creative design models

- 5.5 Variational autoencoders (VAEs)

- 5.5.1 Latent space generation

- 5.5.2 Semantic data modelling

- 5.5.3 Anomaly detection generation

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Content creation and marketing

- 6.2.1 Digital marketing and advertising

- 6.2.2 Social media content generation

- 6.2.3 Blog and article writing

- 6.2.4 Creative design and media production

- 6.3 Customer service and support

- 6.3.1 AI chatbots and virtual assistants

- 6.3.2 Automated response systems

- 6.3.3 Customer query resolution

- 6.3.4 Multilingual support solutions

- 6.4 Software development and IT

- 6.4.1 Code Generation and Completion

- 6.4.2 Bug Detection and Resolution

- 6.4.3 Documentation Generation

- 6.4.4 API development and testing

- 6.5 Research and analytics

- 6.5.1 Data analytics and insights generation

- 6.5.2 Scientific research assistance

- 6.5.3 Market research and competitive intelligence

- 6.5.4 Financial analysis and reporting

- 6.6 Education and training

- 6.6.1 Assessment and evaluation tools

- 6.6.2 Professional skills development

- 6.6.3 Others

Chapter 7 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Cloud-based

- 7.3 On-premises

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Healthcare and life sciences

- 8.2.1 Drug discovery and development

- 8.2.2 Medical imaging and diagnostics

- 8.2.3 Clinical documentation and records

- 8.2.4 Patient care and telemedicine

- 8.3 Financial services and banking

- 8.3.1 Risk assessment and management

- 8.3.2 Fraud detection and prevention

- 8.3.3 Investment research and analysis

- 8.3.4 Customer service automation

- 8.4 Education and E-learning

- 8.4.1 Personalized learning platforms

- 8.4.2 Content creation and curriculum development

- 8.4.3 Student assessment and evaluation

- 8.4.4 Administrative process automation

- 8.5 Media and entertainment

- 8.5.1 Content creation and production

- 8.5.2 Gaming and interactive media

- 8.5.3 Music and audio generation

- 8.5.4 Visual effects and animation

- 8.6 Legal and professional services

- 8.6.1 Contract generation and management

- 8.6.2 Compliance and regulatory support

- 8.7 Retail and E-commerce

- 8.7.1 Customer experience personalization

- 8.7.2 Marketing and advertising optimization

- 8.8 Manufacturing and Industrial

- 8.8.1 Quality control and inspection

- 8.8.2 Predictive maintenance solutions

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Large Enterprises

- 9.3 Small and Medium Enterprises (SMEs)

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Russia

- 10.2.7 Nordics

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 South Korea

- 10.3.5 Australia

- 10.3.6 Singapore

- 10.3.7 Malaysia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Adobe

- 11.2 Amazon Web Services (AWS)

- 11.3 Apple

- 11.4 Anthropic

- 11.5 Baidu

- 11.6 DeepMind

- 11.7 Genie AI

- 11.8 Google

- 11.9 IBM

- 11.10 Intel

- 11.11 Meta

- 11.12 Microsoft

- 11.13 MOSTLY AI

- 11.14 NVIDIA

- 11.15 OpenAI

- 11.16 Oracle

- 11.17 Salesforce

- 11.18 SAP

- 11.19 Synthesia

- 11.20 UiPath

- 11.21 Unity Technologies