PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1782156

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1782156

Enteric Disease Testing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

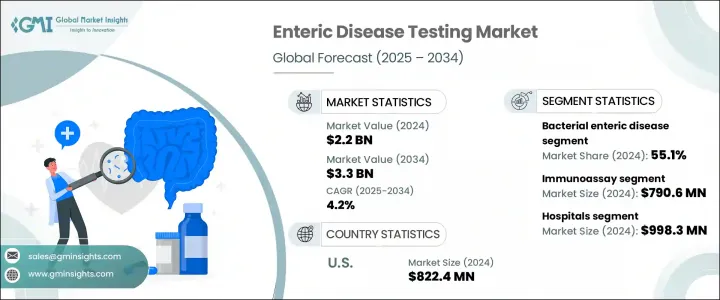

The Global Enteric Disease Testing Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 4.2% to reach USD 3.3 billion by 2034. This growth is driven by the increasing prevalence of enteric infections, greater awareness, surveillance initiatives, and technological advancements in diagnostic testing. Enteric diseases, often occurring in low- and middle-income countries, are commonly linked to inadequate sanitation and contaminated water. These infections are recurrent, with endemic persistence, highlighting the need for timely, accurate diagnostics. Early detection is crucial in facilitating effective interventions that improve patient outcomes and support better disease control efforts.

Additionally, the rise in demand for capsule endoscopy, ingestible sensors, and drug delivery systems has spurred the need for accurate testing of enteric devices. This includes evaluating factors like dissolution, transit time, and localized release within gastrointestinal structures, further driving market expansion. Enteric disease testing refers to diagnostic methods used to identify infections caused by bacteria, viruses, or parasites that affect the digestive tract. Tests are used to detect conditions like diarrhea, cholera, typhoid, and dysentery.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $3.3 Billion |

| CAGR | 4.2% |

The immunoassay segment dominated the market, generating USD 790.6 million in 2024, and is projected to grow at a CAGR of 4.3% through 2034. Immunoassays are widely used for detecting enteric pathogens and are particularly prevalent in low-resource settings, including point-of-care environments. They are the primary method for surveillance and outbreak response, especially for bacterial toxins and viral infections like rotavirus and norovirus.

The hospitals segment led the market in 2024 with a revenue of USD 998.3 million and is expected to grow at a CAGR of 4.4% during 2025-2034. As major centers for acute care and emergency interventions, hospitals handle many severe gastrointestinal cases, especially those related to foodborne diseases. Most urgent cases are processed in hospital-based labs, reflecting the crucial role of these institutions in enteric disease testing.

U.S. Enteric Disease Testing Market was valued at USD 822.4 million in 2024. The country sees millions of foodborne illness cases annually, driven by pathogens like Salmonella, E. coli, and Norovirus. Addressing this public health challenge requires regular, accurate enteric disease testing. Programs from organizations like the CDC and FDA, such as FoodNet and PulseNet, play a vital role in outbreak detection and the development of advanced diagnostic tests. These agencies drive the innovation necessary to improve diagnostic speed and accuracy.

Key players in the Enteric Disease Testing Market include Abbott Laboratories, Becton, Dickinson and Company, Biomerica, bioMerieux, Bio-Rad Laboratories, Coris BioConcept, Danaher, DiaSorin, Merck KGaA, Meridian Bioscience, Techlab, and Thermo Fisher Scientific. To strengthen their position in the enteric disease testing market, companies are focusing on continuous innovation and the development of advanced diagnostic technologies. This includes investing heavily in research and development (R&D) to improve the accuracy, speed, and ease of use of testing kits, particularly for point-of-care settings. Strategic collaborations with government agencies, research institutions, and healthcare providers are also key to expanding their market footprint. Companies are also increasing their presence in emerging markets where the incidence of enteric diseases is high by providing affordable, easy-to-use diagnostic solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Disease trends

- 2.2.3 Test type trends

- 2.2.4 End use trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of enteric diseases

- 3.2.1.2 Technological advancements in diagnostic technologies

- 3.2.1.3 Growing demand for preventive healthcare services

- 3.2.1.4 Rising healthcare expenditure and investments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with enteric disease testing

- 3.2.2.2 Complexity of testing procedures

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Disease, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Bacterial enteric disease

- 5.2.1 Salmonella

- 5.2.2 E. coli

- 5.2.3 Campylobacter

- 5.2.4 C. difficile

- 5.2.5 Shigellosis

- 5.2.6 Listeria

- 5.3 Viral enteric disease

- 5.3.1 Rotavirus infection

- 5.3.2 Norovirus infection

- 5.4 Parasitic enteric disease

- 5.4.1 Giardiasis

- 5.4.2 Amebiasis

- 5.4.3 Cryptosporidiosis

Chapter 6 Market Estimates and Forecast, By Test Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Immunoassay

- 6.3 Molecular

- 6.4 Conventional

- 6.5 Chromatography & spectrometry

- 6.6 Other test types

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Diagnostic laboratories

- 7.4 Research & academic institutes

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Becton, Dickinson and Company

- 9.3 Biomerica

- 9.4 bioMerieux

- 9.5 Bio-Rad Laboratories

- 9.6 Coris BioConcept

- 9.7 Danaher

- 9.8 DiaSorin

- 9.9 Merck KGaA

- 9.10 Meridian Bioscience

- 9.11 Techlab

- 9.12 Thermo Fisher Scientific