PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1782162

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1782162

Inflammatory Bowel Disease Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

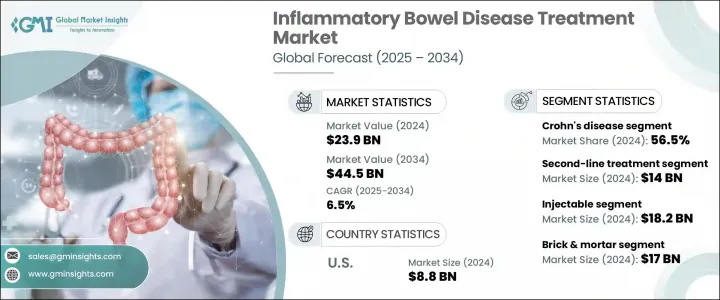

The Global Inflammatory Bowel Disease Treatment Market was valued at USD 23.9 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 44.5 billion by 2034. This growth is primarily driven by a rising global prevalence of IBD, including Crohn's disease and ulcerative colitis, as well as expanding access to early diagnosis and treatment. Changing diets, sedentary lifestyles, and environmental factors are contributing to the increasing number of IBD cases, especially in developed nations. Enhanced awareness campaigns and more favorable reimbursement structures are improving diagnosis rates and patient adherence.

Innovation in treatment approaches-such as targeted biologics and small molecules-has significantly advanced therapeutic outcomes and reduced treatment-related complications. Government support in the form of public funding and faster regulatory reviews is also encouraging the development and uptake of next-generation therapies. With the patient population growing steadily, demand continues to rise for long-term, effective solutions that improve quality of life and reduce disease flare-ups. Collectively, these factors are shaping a robust and dynamic market environment for IBD therapies over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $23.9 Billion |

| Forecast Value | $44.5 Billion |

| CAGR | 6.5% |

In 2024, the Crohn's disease segment held a 56.5% share and is forecasted to grow at a CAGR of 6.3% during 2025-2034. This expansion is largely attributed to an uptick in newly diagnosed cases among younger individuals, particularly across North America and Europe. Crohn's disease tends to require more complex and long-term treatment approaches than ulcerative colitis, given that it can affect any part of the gastrointestinal tract and penetrate deeper layers of tissue. As a result, healthcare providers are increasingly utilizing high-value therapies such as immunosuppressants and biologics. The growing adoption of advanced treatment classes, including Janus kinase inhibitors and anti-integrin agents, has redefined how the disease is managed and significantly contributed to segment growth.

The injectable therapies segment generated the highest revenue in 2024, valued at USD 18.2 billion, and is expected to maintain a CAGR of 6.4% through 2034. This category is led by the widespread use of biologics, particularly monoclonal antibodies, which are generally delivered via injection. These therapies have become the cornerstone for treating moderate to severe IBD by offering precision targeting of inflammation pathways. Agents that modulate immune activity at the molecular level are proving highly effective in maintaining remission and minimizing disease recurrence, especially for patients unresponsive to traditional medications. Long-acting injectables also contribute to higher compliance rates and improved patient satisfaction.

U.S. Inflammatory Bowel Disease Treatment Market was valued at USD 8.8 billion in 2024. Growth in this market is driven by a rising incidence of both Crohn's disease and ulcerative colitis across diverse demographics. Improved diagnostic capabilities, enhanced access to specialists, and expanding use of targeted therapies are all accelerating market development. The availability of innovative drug delivery technologies, such as long-acting subcutaneous injectables and sustained-release formulations, has improved treatment adherence. These advancements are making it easier for patients to manage their conditions and maintain long-term remission, further boosting demand for advanced therapeutics.

Key players operating in the Global Inflammatory Bowel Disease Treatment Market include Pfizer, Biogen, Takeda, Dr Falk, Johnson & Johnson, CELLTRION, AbbVie, Ferring, Merck, UCB, Novartis, Tillotts Pharma, Lilly, and Amgen. These companies continue to influence market direction through strategic investments and innovative drug development. To strengthen their presence in the IBD treatment space, leading pharmaceutical firms are advancing a multi-pronged approach that includes research-driven innovation, regulatory engagement, and collaborative partnerships.

Companies are investing significantly in clinical trials to develop novel biologics and small molecules with improved efficacy and fewer side effects. Expanding product pipelines through licensing deals, mergers, and acquisitions has also become a common strategy. Many are working closely with health authorities to secure accelerated approvals and ensure broad reimbursement access.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Treatment type trends

- 2.2.3 Drug class trends

- 2.2.4 Route of administration trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of IBD

- 3.2.1.2 Technological advancements

- 3.2.1.3 Favorable reimbursement policies

- 3.2.1.4 Growing awareness and early diagnosis of IBD symptoms

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory scenario

- 3.2.2.2 High cost of treatment

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of biologics and targeted therapies

- 3.2.3.2 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Reimbursement scenario

- 3.5 Regulatory landscape

- 3.6 Pipeline analysis

- 3.7 Investment scenarios outlook

- 3.8 Treatment switching patterns or sequencing trends

- 3.9 Epidemiological scenario

- 3.10 Future market trends/ Key marketed therapies

- 3.11 Brand analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Company matrix analysis

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Crohn's disease

- 5.3 Ulcerative colitis

Chapter 6 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 First-line treatment

- 6.2.1 Aminosalicylates

- 6.2.2 Corticosteroids

- 6.3 Second-line treatment

- 6.3.1 TNF inhibitors

- 6.3.2 IL inhibitors

- 6.3.3 JAK inhibitors

- 6.3.4 Anti-integrin

- 6.4 Combination therapy

- 6.4.1 TNF inhibitors + thiopurines

- 6.4.2 Other combination therapies

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Injectable

- 7.3 Oral

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Brick & mortar

- 8.3 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 Amgen

- 10.3 Biogen

- 10.4 CELLTRION

- 10.5 Dr Falk

- 10.6 Ferring

- 10.7 Johnson & Johnson

- 10.8 Lilly

- 10.9 Merck

- 10.10 Novartis

- 10.11 Pfizer

- 10.12 Takeda

- 10.13 Tillotts Pharma

- 10.14 UCB