PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797698

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797698

Condensed Canned Soups Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

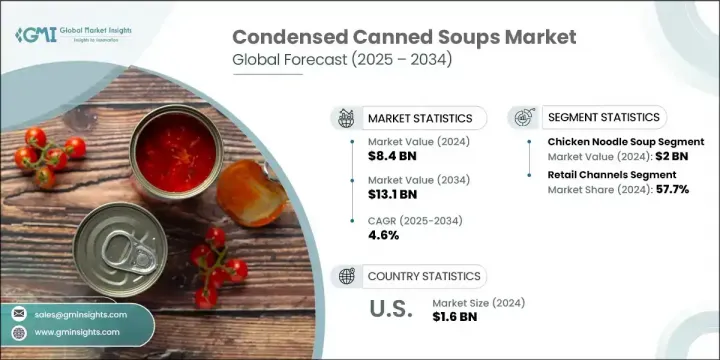

The Global Condensed Canned Soups Market was valued at USD 8.4 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 13.1 billion by 2034. These soups remain a staple in the packaged food space due to their affordability, ease of preparation, and extended shelf stability. However, consumer preferences have evolved significantly, pushing brands to reimagine their offerings. A growing number of consumers are opting for cleaner labels, natural ingredients, and health-focused variants, leading to product reformulations that emphasize low-sodium content, organic certification, and plant-based ingredients. Food manufacturers are increasingly innovating with nutrient-rich, protein-enhanced condensed soups that offer more than just convenience.

These products are now positioned not only as ready-to-eat meals but also as versatile bases for home-cooked recipes. As more consumers shift toward health-conscious eating, the demand for enriched, customizable meal components has accelerated. This trend is particularly prominent in rapidly urbanizing areas, especially across the Asia-Pacific region, where a growing middle class and fast-paced lifestyles are fueling increased demand for nutritious, time-saving meals. Countries in the region are witnessing a strong uptake in condensed soup consumption as part of the broader shift toward convenient food options that align with evolving dietary habits.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.4 Billion |

| Forecast Value | $13.1 Billion |

| CAGR | 4.6% |

The chicken noodle soup segment generated USD 2 billion in 2024. Other popular varieties include tomato-based, cream of mushroom, and cream of chicken soups, which have proven to be reliable both as standalone meals and as ingredients in broader meal preparation. Rising interest in better-for-you options is also driving growth in vegetable and beef-based soups, while plant-forward and high-protein selections are gaining traction. To align with modern consumer expectations, brands are revisiting traditional formulations to introduce organic, allergen-friendly, and reduced-sodium recipes, expanding their appeal to health-conscious audiences without compromising flavor or texture.

The retail outlets segment held a 57.7% share in 2024. Supermarkets, hypermarkets, and neighborhood grocery stores remain the dominant distribution channels, offering consumers access to various brands, prices, and flavors. These stores benefit from prominent product placement, seasonal promotions, and strong private-label competition, which influence purchasing behavior and keep this channel highly relevant for mainstream buyers.

North American Condensed Canned Soups Market generated USD 1.6 billion in 2024, driven by strong cultural familiarity with canned soups. With changing eating habits and increasing health awareness, the U.S. market shows a solid appetite for clean-label, organic, and plant-based soups. A well-established retail network, along with investments in advanced food processing and technology, allows American companies to respond quickly to emerging trends, keeping the U.S. at the forefront of innovation in this sector.

Key players contributing to the Global Condensed Canned Soups Market include Nestle S.A., Amy's Kitchen Inc., BCI Foods Inc., The Kraft Heinz Company, Unilever (Knorr), Campbell Soup Company, General Mills Inc., ConAgra Brands Inc., Baxters Food Group, and Vanee Foods Company. Leading brands in the condensed canned soups market are prioritizing product diversification through reformulation, introducing low-sodium, organic, gluten-free, and plant-based varieties. Many companies are investing in sustainable packaging and enhancing flavor profiles to meet evolving consumer preferences. Innovation is also fueled by R&D to integrate superfoods, plant proteins, and allergen-friendly ingredients. In addition, brands are optimizing supply chains and expanding retail partnerships for better shelf visibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Distribution channel trends

- 2.2.3 Packaging format trends

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By product type trends

- 3.8.2 By distribution channel trends

- 3.8.3 By packaging format trends

- 3.8.4 By region

- 3.9 Future market trends

- 3.10 Technology and Innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent Landscape

- 3.12 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Billion) (Units)

- 5.1 Key trends

- 5.2 Condensed soup varieties

- 5.2.1 Chicken noodle soup

- 5.2.2 Tomato soup

- 5.2.3 Cream of mushroom soup

- 5.2.4 Cream of chicken soup

- 5.2.5 Vegetable soup

- 5.2.6 Beef-based soups

- 5.2.7 Cream-based specialty soups

Chapter 6 Market Estimates and Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Units)

- 6.1 Key trends

- 6.2 Retail channels

- 6.2.1 Supermarkets and hypermarkets

- 6.2.2 Convenience stores

- 6.2.3 Discount retailers

- 6.2.4 Specialty food stores

- 6.2.5 Online retail and e-commerce

- 6.3 Foodservice channels

- 6.3.1 Restaurants and quick service

- 6.3.2 Institutional foodservice

- 6.3.3 Healthcare and educational facilities

- 6.4 Direct-to-consumer channels

Chapter 7 Market Estimates and Forecast, By Packaging Format, 2021-2034 (USD Billion) (Units)

- 7.1 Key trends

- 7.2 Traditional metal cans

- 7.2.1 Standard size cans (10.5-11 oz)

- 7.2.2 Family size cans (18-23 oz)

- 7.2.3 Institutional size cans

- 7.3 Alternative packaging formats

- 7.3.1 Flexible pouches and stand-up pouches

- 7.3.2 Aseptic cartons and tetra packs

- 7.3.3 Microwaveable containers

- 7.3.4 Single-serve cups and bowls

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Campbell Soup Company

- 9.2 General Mills Inc. (Progresso)

- 9.3 The Kraft Heinz Company

- 9.4 Nestle S.A.

- 9.5 Unilever (Knorr)

- 9.6 ConAgra Brands Inc.

- 9.7 Baxters Food Group

- 9.8 BCI Foods Inc.

- 9.9 Vanee Foods Company

- 9.10 Amy’s Kitchen Inc