PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797708

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797708

Polymer Filaments for Construction-Scale 3D Printing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

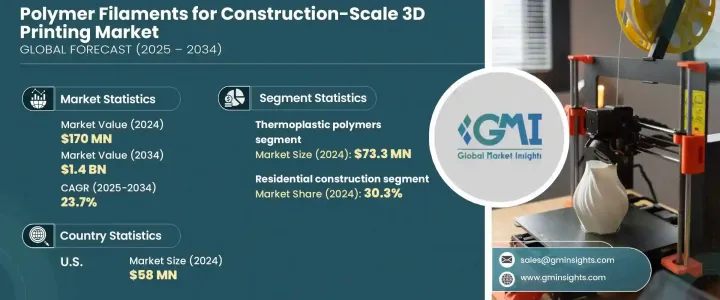

The Global Polymer Filaments for Construction-Scale 3D Printing Market was valued at USD 170 million in 2024 and is estimated to grow at a CAGR of 23.7% to reach USD 1.4 billion by 2034. This rapid growth is driven by the increasing demand for innovative and sustainable building methods. Engineered thermoplastics such as ABS, PLA, and PET are being optimized for large-format additive manufacturing applications, from structural parts to entire buildings. The versatility of 3D printing enables architects and engineers to create lightweight, complex structures that traditional methods cannot support. This capability is fostering rapid adoption of advanced polymer filaments.

Government-backed infrastructure development initiatives and sustainability standards are accelerating interest in this technology. The automation capabilities of 3D printing also reduce material waste and manual labor, making it a more cost-efficient solution for construction. Global emphasis on smart infrastructure, especially across rapidly urbanizing regions in Asia-Pacific, is positioning countries like India, China, and Japan as leaders in the adoption of high-performance 3D printing materials for building and development projects.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $170 million |

| Forecast Value | $1.4 billion |

| CAGR | 23.7% |

The residential construction segment held a 30.3% share in 2024. This application is gaining traction for its role in addressing housing shortages and affordability. Using polymer filaments, components can be produced quickly, cutting down both construction timelines and labor costs. These materials also support renovation and modular builds, making them ideal for a wide range of housing solutions that respond to immediate market needs.

The large-scale fused deposition modeling (FDM) technology segment held a notable share in 2024 due to its operational simplicity and relatively low setup costs. Its scalable nature makes it an ideal solution for different levels of construction - from foundational components to full-scale residential or commercial buildings. The accessibility of extrusion-based equipment has contributed to its widespread adoption and performance reliability.

U.S. Polymer Filaments for Construction-Scale 3D Printing Market generated USD 58 million in 2024. This strong market presence is driven by a robust innovation ecosystem, increasing R&D efforts, and the demand for sustainable construction methods. Companies in the U.S. are accelerating development of advanced filament materials that meet the technical needs of large-scale construction while aligning with environmental and cost-efficiency objectives. This focus continues to strengthen the country's leadership in the sector.

Key players in Polymer Filaments for Construction-Scale 3D Printing Market include Coex 3D, Arkema, BASF SE, Sika AG, Skanska AB, Covestro, MudBots, Mighty Buildings, Tvasta Manufacturing Solutions, and Manlon Polymers. Companies in the polymer filaments for construction-scale 3D printing market are focusing on developing high-performance, recyclable, and climate-resilient materials to meet the evolving needs of the construction sector. Investments in R&D help improve the strength, durability, and thermal resistance of filament compositions. Many manufacturers are forming collaborations with construction tech firms and academic institutions to speed up innovation and commercial readiness. Expanding global distribution and localized production capabilities also allows companies to serve infrastructure projects in fast-developing regions. Strategic mergers and technology licensing are used to gain access to proprietary additive manufacturing platforms.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Application trends

- 2.2.3 Technology trends

- 2.2.4 End use trends

- 2.2.5 Equipment scale trends

- 2.2.6 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By material type

- 3.9 Future market trends

- 3.10 Technology and Innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent Landscape

- 3.12 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2021-2034 (USD Million) (Units)

- 5.1 Key trends

- 5.2 Thermoplastic polymers

- 5.2.1 PLA (polylactic acid) and bio-based thermoplastics

- 5.2.2 ABS (acrylonitrile butadiene styrene) and engineering plastics

- 5.2.3 PETG (polyethylene terephthalate glycol) and specialty polymers

- 5.2.4 High-performance engineering plastics (PEEK, PEI, PEKK)

- 5.3 Fiber-reinforced composites

- 5.3.1 Carbon fiber reinforced polymers (CFRP)

- 5.3.2 Glass fiber reinforced polymers (GFRP)

- 5.3.3 Natural fiber reinforced composites

- 5.3.4 Continuous fiber reinforcement systems

- 5.4 Sustainable and bio-based materials

- 5.4.1 Bio-based polymer formulations

- 5.4.2 Recycled content and post-consumer materials

- 5.4.3 Biodegradable and compostable polymers

- 5.4.4 Waste-derived and circular economy materials

- 5.5 Specialty and functional materials

- 5.5.1 Fire-resistant and flame-retardant polymers

- 5.5.2 Thermal insulation and energy-efficient materials

- 5.5.3 Conductive and smart material systems

- 5.5.4 Multi-functional and hybrid material solutions

- 5.6 Emerging and advanced materials

- 5.6.1 Nanocomposite and enhanced performance materials

- 5.6.2 Shape memory and responsive polymer systems

- 5.6.3 Self-healing and adaptive material technologies

- 5.6.4 Biomimetic and nature-inspired material solutions

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million) (Units)

- 6.1 Key trends

- 6.2 Residential construction

- 6.3 Commercial construction

- 6.4 Infrastructure and civil engineering

- 6.5 Architectural and decorative elements

- 6.6 Specialty and niche applications

Chapter 7 Market Estimates and Forecast, By Technology, 2021-2034 (USD Million) (Units)

- 7.1 Key trends

- 7.2 Large-scale fused deposition modelling (FDM)

- 7.3 Robotic construction systems

- 7.4 Continuous manufacturing technologies

- 7.5 Emerging and advanced technologies

Chapter 8 Market Estimates and Forecast, By End Use, 2021-2034 (USD Million) (Units)

- 8.1 Key trends

- 8.2 Construction companies and general contractors

- 8.3 Architects and design professionals

- 8.4 Real estate developers and building owners

- 8.5 Research and educational institutions

- 8.6 Government and public sector

Chapter 9 Market Estimates and Forecast, By Equipment Scale, 2021-2034 (USD Million) (Units)

- 9.1 Key trends

- 9.2 Large-scale industrial systems

- 9.3 Medium- scale industrial systems

- 9.4 Compact and portable systems

- 9.5 Hybrid and multi-technology systems

Chapter 10 Market Estimates and Forecast, By Region, 2021-2034 (USD Million) (Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Arkema

- 11.2 BASF SE

- 11.3 Coex 3D

- 11.4 Covestro

- 11.5 Manlon Polymers

- 11.6 Mighty Buildings

- 11.7 MudBots

- 11.8 Sika AG

- 11.9 Skanska AB

- 11.10 Tvasta Manufacturing Solutions