PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797714

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797714

Food Fibers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

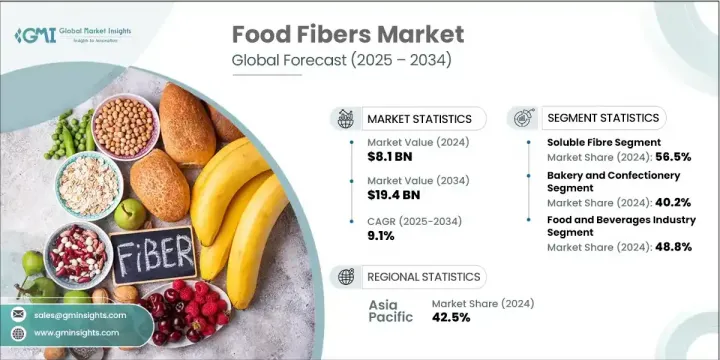

The Global Food Fibers Market was valued at USD 8.1 billion in 2024 and is estimated to grow at a CAGR of 9.1% to reach USD 19.4 billion by 2034. Food fibers, commonly known as dietary fibers, are indigestible plant-based carbohydrates that offer a variety of health benefits, particularly in digestive wellness, blood sugar regulation, and appetite control. These fibers are naturally present in fruits, legumes, vegetables, and grains, and are increasingly included in a wide range of consumables like dairy alternatives, fortified drinks, and bakery products. As global consumer preferences shift toward functional and health-forward eating, the market continues to gain momentum.

The trend is further amplified by the push for plant-based living, growing awareness of gut microbiome health, and supportive policies encouraging fiber-enhanced labeling and formulation. New innovations in fiber extraction and incorporation-such as microencapsulation and high-efficiency extrusion-are opening the door for more advanced and appealing food products. Manufacturers are strategically aligning with these developments to meet the growing demand for natural, prebiotic-rich, clean-label solutions. The rapid adoption of functional fibers globally, backed by evolving consumer lifestyles and nutritional awareness, is paving the way for robust growth in this industry.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.1 Billion |

| Forecast Value | $19.4 Billion |

| CAGR | 9.1% |

The soluble fibers held a 56.5% share in 2024, contributing USD 4.6 billion. These types of fibers, which include inulin, gums, and pectins, are widely used in foods and beverages because of their ability to support gut health by feeding beneficial microbes. Their use extends to plant-based milks and fermented beverages, where they enhance both texture and nutritional density. In the food manufacturing process, soluble fibers also improve product stability and mouthfeel, especially in reduced-sugar or dairy-free options. These fibers serve dual purposes, acting as both functional nutrients and sensory enhancers in various formulations across the food sector. Their rising inclusion in daily diets reflects how consumer interest in digestive and metabolic health is transforming formulation strategies within food production.

The bakery and confectionery segment held a 40.2% share, reaching USD 3.3 billion in 2024. This segment remains a dominant application area for food fibers, thanks to their growing use in items like baked snacks, whole grain breads, and cereals. Dietary fibers in baked goods improve texture, increase satiety, and align with the clean-label movement that avoids artificial additives. Confectionery manufacturers also integrate functional fibers to lower sugar and calorie content without compromising taste or texture. The surge in demand for high-fiber snack options and whole-grain bakery products continues to push innovation, especially across regions like Asia-Pacific and North America where consumer demand for wellness-oriented products is soaring.

Asia Pacific Food Fibers Market held a 42.5% share in 2024. This region's leadership is driven by increasing consumer education on digestive health, a swelling middle-class population, and rapid growth in functional food and beverage categories. Countries such as Japan, China, South Korea, and India are witnessing a transformation in dietary habits toward more fiber-rich, plant-centric foods. Ongoing support from health-conscious policies and national wellness initiatives is further driving growth. As plant-based and fiber-enhanced products gain popularity, especially in categories like baked goods and nutraceuticals, online commerce and digital retail infrastructure are playing a significant role in improving product access across diverse population groups in Asia Pacific.

Key companies shaping this Global Food Fibers Market include Archer Daniels Midland Company (ADM), Cargill, Incorporated, Roquette Freres SA, Tate & Lyle PLC, and Ingredion Incorporated. To stay competitive and expand their market share, leading companies in the food fibers sector are emphasizing innovation in fiber extraction and formulation. They are heavily investing in research to develop novel blends that are functional, easy to integrate, and have enhanced sensory properties. Businesses are also prioritizing sustainability by sourcing plant materials responsibly and improving processing efficiencies. Collaborations with food tech firms and nutrition-focused startups allow access to new markets and technologies. Moreover, brands are working to expand their clean-label offerings to align with evolving consumer expectations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Fiber type

- 2.2.3 Application

- 2.2.4 End use industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By fiber type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Fiber Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Soluble fibres

- 5.2.1 Inulin and oligofructose segment

- 5.2.2 Pectin and gums segment

- 5.2.3 Beta-glucan and specialty fibres

- 5.3 Insoluble fibres

- 5.3.1 Cellulose and modified cellulose

- 5.3.2 Wheat bran and cereal fibres

- 5.3.3 Fruit and vegetable fibres

- 5.4 Functional and prebiotic fibres

- 5.4.1 Resistant starch technologies

- 5.4.2 Galacto-oligosaccharides (GOS) and fructo-oligosaccharides (FOS)

- 5.4.3 Novel and emerging fibres

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Bakery and confectionery

- 6.2.1 Bread and baked goods

- 6.2.2 Breakfast cereals and snack foods

- 6.2.3 Confectionery and sweet goods

- 6.3 Beverages

- 6.3.1 Functional and sports beverages

- 6.3.2 Dairy and plant-based alternatives

- 6.3.3 Juice and enhanced water

- 6.4 Dairy and dairy alternatives

- 6.4.1 Yogurt and fermented products

- 6.4.2 Cheese and processed dairy

- 6.4.3 Plant-based dairy alternatives

- 6.5 Dietary supplements

- 6.5.1 Powder and capsule formats

- 6.5.2 Prebiotic and gut health supplements

- 6.5.3 Weight management and metabolic health

Chapter 7 Market Estimates and Forecast, By End use Industry, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food and beverage manufacturing

- 7.2.1 Large-scale food manufacturers

- 7.2.2 Regional and specialty food companies

- 7.2.3 Technology and equipment suppliers

- 7.3 Dietary supplement industry

- 7.3.1 Supplement manufacturers and brands

- 7.3.2 Contract manufacturers and private label

- 7.3.3 Distribution and retail channels

- 7.4 Functional foods and nutraceuticals

- 7.4.1 Functional food development

- 7.4.2 Medical foods and clinical nutrition

- 7.4.3 Sports and performance nutrition

- 7.5 Animal feed and pet food

- 7.5.1 Premium pet food applications

- 7.5.2 Livestock and aquaculture

- 7.5.3 Market development and innovation

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.3.7 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Cargill, Incorporated

- 9.2 Tate & Lyle PLC

- 9.3 Archer Daniels Midland Company

- 9.4 Ingredion Incorporated

- 9.5 Roquette Freres SA

- 9.6 Kerry Group PLC

- 9.7 International Flavors & Fragrances Inc

- 9.8 J Rettenmaier & Sohne GmbH + Co KG

- 9.9 Nexira Inc