PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797717

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797717

Lysosomal Storage Disease Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

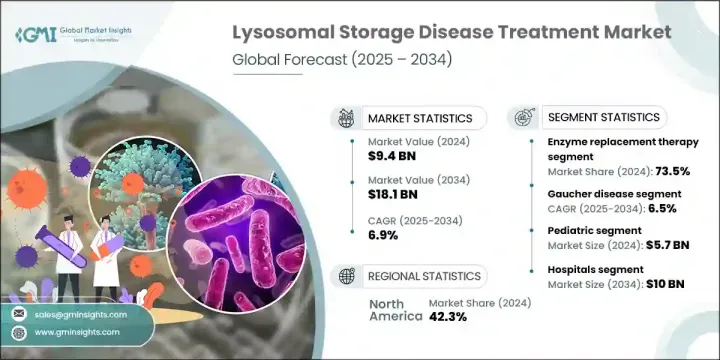

The Global Lysosomal Storage Disease Treatment Market was valued at USD 9.4 billion in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 18.1 billion by 2034. The growing incidence of rare genetic disorders such as Fabry, Gaucher, and Pompe disease is a significant driver of market growth. Advances in enzyme replacement therapies and gene therapies-coupled with regulatory frameworks that grant orphan drug designation-are accelerating therapeutic development for these conditions. The treatment landscape now includes enzyme replacement, small molecule drugs, and gene-based interventions, all aimed at improving patient quality of life and clinical outcomes.

Leading companies like Sanofi, Amicus Therapeutics, BioMarin, Takeda Pharmaceutical, and Orchard Therapeutics are actively involved in global distribution expansion and innovation in novel treatment modalities. Expanding newborn-screening programs and broader awareness initiatives are enabling earlier diagnosis and intervention, which is critical for optimal treatment response and long-term prognosis. Increased early detection is boosting demand for both diagnostics and therapeutics, reshaping market dynamics and driving pipeline growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.4 Billion |

| Forecast Value | $18.1 Billion |

| CAGR | 6.9% |

The enzyme replacement therapy segment held a 73.5% share in 2024. Its prevalence is due to widespread adoption through enhanced diagnostic programs and better disease awareness. The high efficacy of these treatments in managing enzyme-deficient lysosomal diseases has led to substantial patient improvement, prompting pharmaceutical companies to invest in expanding and enhancing these therapies through collaborations and in-house development.

The mucopolysaccharidoses therapies segment held a 27.4% share in 2024. Market expansion for MPS treatment is supported by regulatory incentives, including expedited approval pathways and tax credits offered under orphan drug provisions. Investment from pharmaceutical and biotech companies in cell therapy, engineered B-cell treatments, and gene editing approaches is growing rapidly, necessitating enhanced laboratory infrastructure, assay development, and extensive clinical trial support.

North America Lysosomal Storage Disease Treatment Market held a 42.3% share in 2024. The U.S. and Canada lead due to robust insurance coverage for high-cost rare disease treatments and substantial public funding for LSD research. Institutes such as the NIH and Canadian health research agencies provide significant grants to support research, enabling therapeutic innovation and growth of future treatment pipelines.

Key companies active in the Lysosomal Storage Disease Treatment Market include Sigilon Therapeutics, Pfizer, Orphazyme, Alexion Pharmaceuticals, Sangamo Therapeutics, JCR Pharmaceuticals, Avrobio, Genzyme (Sanofi), Orchard Therapeutics, Takeda Pharmaceutical Company, BioMarin, and Amicus Therapeutics. Leading players are strengthening their position by investing in innovative therapies like gene editing platforms and next-generation enzyme replacement treatments. Strategic collaborations with academic institutions and biotech firms are expanding research capabilities. Companies are also developing robust global distribution networks to ensure market access, while engaging in targeted awareness and screening initiatives to boost early diagnosis rates. Through public-private partnerships and registry-based research, firms are accelerating clinical trials and enhancing patient recruitment.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Treatment type trends

- 2.2.3 Disease type trends

- 2.2.4 Age group trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing diagnosis due to newborn-screening programs

- 3.2.1.2 Growing pipeline of gene and enzyme therapies

- 3.2.1.3 Advancement in molecular and biomarker-based diagnosis

- 3.2.1.4 Increasing shift towards disease-modifying and curative therapies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Limited penetration in low-and middle-income countries (LMICs)

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand of gene therapy and genome editing

- 3.2.3.2 Rise in specialized rare disease treatment centers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Pricing analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Enzyme replacement therapy

- 5.3 Stem cell transplants

- 5.4 Substrate reduction therapy

- 5.5 Other treatment types

Chapter 6 Market Estimates and Forecast, By Disease Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Gaucher disease

- 6.3 Mucopolysaccharidoses

- 6.4 Pompe disease

- 6.5 Fabry disease

- 6.6 Other disease types

Chapter 7 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pediatric

- 7.3 Adult

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Specialty clinics

- 8.4 Homecare settings

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Alexion Pharmaceuticals

- 10.2 Amicus Therapeutics

- 10.3 Avrobio

- 10.4 BioMarin

- 10.5 JCR Pharmaceuticals

- 10.6 Johnson & Johnson (Actelion Pharmaceuticals)

- 10.7 Orchard Therapeutics

- 10.8 Orphazyme

- 10.9 Pfizer

- 10.10 Sanofi (Genzyme Corporation)

- 10.11 Sigilon Therapeutics

- 10.12 Sangamo therapeutics

- 10.13 Takeda Pharmaceutical Company (Shire)