PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797749

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797749

Battery Binder Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

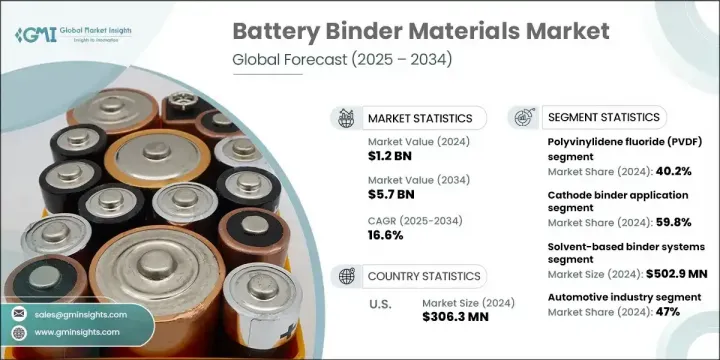

The Global Battery Binder Materials Market was valued at USD 1.2 billion in 2024 and is estimated to grow at a CAGR of 16.6% to reach USD 5.7 billion by 2034. This upward trend is largely influenced by the escalating demand for lithium-ion batteries across a variety of high-growth sectors such as electric vehicles, mobile electronics, and renewable energy storage systems. Battery binders-specialized polymers used to secure active particles to electrode current collectors-are becoming increasingly vital in designing batteries with greater efficiency, higher capacity, and extended lifespans. Their role as structural "adhesives" ensures cohesive binding and durability, directly impacting the battery's mechanical integrity and cycle performance.

The expansion of energy-dense, compact battery designs for modern consumer devices like wearables and smartphones is accelerating innovation in binder material formulations. With the integration of large-scale battery storage systems into renewable energy infrastructure, the need for long-lasting and thermally stable binders has grown sharply. Manufacturers are focusing on producing next-generation acrylic-based binders to boost electrode cohesion, enhance mechanical strength, and improve flexibility. Rising emphasis on lightweight components and environmental compatibility continues to steer product development, while growing adoption of sustainable materials further elevates demand in advanced manufacturing sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.2 Billion |

| Forecast Value | $5.7 Billion |

| CAGR | 16.6% |

The cathode binders segment held 59.8% share in 2024, with projected growth at a CAGR of 16.5% through 2034. These binders are essential in maintaining cathode durability and performance under rigorous charge-discharge cycles. Among the most used materials is PVDF (polyvinylidene fluoride), known for its robust chemical and thermal resistance, reliable adhesion, and compatibility with a wide range of cathode materials. Cathode binders play a critical role in ensuring that the active materials remain effectively connected to the collector surface, thereby contributing to battery stability and output efficiency.

In 2024, the solvent-based binder systems segment was valued at USD 502.9 million and is projected to grow at a CAGR of 16.8% through 2034. Historically, PVDF-based solvent binders using NMP were favored in battery manufacturing due to their ability to offer superior adhesion, chemical resilience, and performance. However, these materials are now facing tighter restrictions due to increasing environmental and safety regulations in key regions like Europe and North America. While solvent-based systems still dominate, the shift toward water-based and more eco-friendly binder technologies is reshaping the landscape, pushing manufacturers toward cleaner and more compliant alternatives without compromising performance.

United States Battery Binder Materials Market generated USD 306.3 million in 2024, with expected growth at a CAGR of 13.7% through 2034. The nation continues to thrive as a central hub for battery binder innovation, propelled by its robust electric vehicle rollout, significant investments in energy storage, and deep-rooted manufacturing ecosystem. Extensive federal support for domestic battery supply chains, combined with financial incentives for advanced adhesive production, has strengthened the U.S. foothold in this fast-evolving market. Strategic capital infusion is also advancing production capabilities for next-gen binder materials like SBR and PVDF, further driving local development.

Key companies leading the Global Battery Binder Materials Market include Zeon Corporation, Solvay S.A., Chemours Company, Sinochem Lantian, Dongyue Group, Arkema S.A., Kureha Corporation, Shanghai 3F New Materials, JSR Corporation, and Shandong Huaxia Shenzhou New Material. They are investing significantly in R&D to develop environmentally friendly and high-performance binder formulations that meet global sustainability goals. Collaborations with battery cell manufacturers and OEMs are enabling faster integration of new materials into next-generation battery systems. Companies are also expanding production capacity and entering joint ventures to strengthen their regional reach. To comply with shifting regulatory landscapes, market leaders are transitioning from traditional solvent-based systems to water-based alternatives while focusing on scalability and energy efficiency during manufacturing.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 Technology

- 2.2.5 End use industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Electric vehicle market expansion

- 3.2.1.2 Energy storage system deployment

- 3.2.1.3 Consumer electronics demand growth

- 3.2.1.4 Battery performance enhancement requirements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High material costs and price volatility

- 3.2.2.2 Environmental and safety regulations

- 3.2.2.3 Technical performance limitations

- 3.2.2.4 Supply chain concentration risks

- 3.2.3 Market opportunities

- 3.2.3.1 Next-generation battery technologies

- 3.2.3.2 Sustainable and bio-based binder development

- 3.2.3.3 Silicon anode technology adoption

- 3.2.3.4 Emerging market penetration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyvinylidene Fluoride (PVDF)

- 5.3 Carboxymethyl Cellulose (CMC)

- 5.4 Styrene-Butadiene Rubber (SBR)

- 5.5 Polyacrylic Acid (PAA)

- 5.6 Other Specialty Binders

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cathode binder applications

- 6.2.1 NCM cathode systems

- 6.2.2 NCA cathode systems

- 6.2.3 LFP cathode systems

- 6.2.4 High-voltage Cathode Materials

- 6.3 Anode binder applications

- 6.3.1 Graphite anode systems

- 6.3.2 Silicon-based anode systems

- 6.3.3 Lithium titanate oxide (LTO) systems

- 6.3.4 Next-generation anode materials

Chapter 7 Market Estimates and Forecast, By Technology, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Solvent-based binder systems

- 7.2.1 Traditional PVDF systems

- 7.3 Water-based binder systems

- 7.3.1 CMC/SBR combinations

- 7.4 Hybrid binder systems

- 7.4.1 Multi-component formulations

- 7.5 Next-generation technologies

- 7.5.1 Solid-state battery binders

- 7.5.2 Conductive binder networks

- 7.5.3 Self-healing materials

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Automotive industry

- 8.2.1 Electric passenger vehicles

- 8.2.2 Electric commercial vehicles

- 8.2.3 Hybrid electric vehicles

- 8.3 Consumer electronics

- 8.3.1 Smartphones and tablets

- 8.3.2 Laptops and portable devices

- 8.3.3 Wearable electronics

- 8.3.4 Gaming and entertainment devices

- 8.4 Energy storage systems

- 8.4.1 Grid-scale energy storage

- 8.4.2 Residential energy storage

- 8.4.3 Commercial and industrial storage

- 8.4.4 Renewable energy integration

- 8.5 Industrial applications

- 8.5.1 Material handling equipment

- 8.5.2 Backup power systems

- 8.5.3 Telecommunications infrastructure

- 8.5.4 Medical and healthcare devices

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Arkema S.A.

- 10.2 Chemours Company

- 10.3 Dongyue Group

- 10.4 JSR Corporation

- 10.5 Kureha Corporation

- 10.6 Shandong Huaxia Shenzhou New Material

- 10.7 Shanghai 3F New Materials

- 10.8 Sinochem Lantian

- 10.9 Solvay S.A.

- 10.10 Zeon Corporation