PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797776

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797776

Predictive Airplane Maintenance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

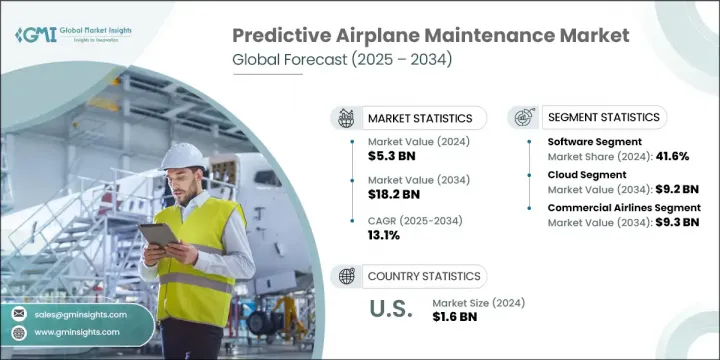

The Global Predictive Airplane Maintenance Market was valued at USD 5.3 billion in 2024 and is estimated to grow at a CAGR of 13.1% to reach USD 18.2 billion by 2034. This growth is driven primarily by the rising volume of air traffic and continuous fleet expansion worldwide. The aviation sector is increasingly adopting advanced Internet of Things (IoT) solutions and sophisticated analytics to enhance maintenance operations. Predictive maintenance is becoming critical for ensuring aircraft safety, boosting reliability, and maximizing operational efficiency amid growing demand for air travel. Airlines and maintenance, repair, and overhaul (MRO) providers are leveraging artificial intelligence and machine learning to enhance fault detection and predict failures, enabling proactive maintenance schedules and minimizing unexpected downtime. This evolution improves fleet uptime and optimizes resource deployment globally. However, as these platforms depend on interconnected data systems, cybersecurity measures have become vital to protect sensitive information from emerging threats.

In 2024, the software segment commanded the largest market share of 41.6%. Predictive airplane maintenance software is integral for real-time data processing, fault identification, and failure forecasting. The market is witnessing increased investment in AI-driven, automated solutions tailored for scalability and customization, allowing seamless integration with existing airline operations and adaptability to shifting demands.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.3 Billion |

| Forecast Value | $18.2 Billion |

| CAGR | 13.1% |

Meanwhile, the cloud segment is projected to reach USD 9.2 billion by 2034. Cloud platforms facilitate remote access, flexibility, and real-time data streaming, enhancing collaboration and decision-making. Adoption is rising due to lower upfront costs and streamlined system upgrades, though concerns around data security and latency persist. Providers are responding by offering robust cybersecurity and hybrid cloud architectures.

North America Predictive Airplane Maintenance Market held a 36.5% share in 2024 and is expected to grow at a CAGR of 12.1% through 2034. The region benefits from extensive aviation infrastructure, proactive adoption of predictive technologies, and strong regulatory frameworks that support digital innovation in aviation maintenance. Major players driving this market include IBM, Lufthansa Technik, The Boeing Company, Airbus SE, and General Electric Company.

To strengthen their market position, companies in the Predictive Airplane Maintenance Market focus on several strategic approaches. These include investing heavily in research and development to enhance AI and machine learning capabilities, enabling more accurate and automated diagnostics. They also pursue strategic partnerships and collaborations with airlines and MRO providers to deepen market penetration and tailor solutions to client needs. Offering modular, scalable software platforms with seamless integration capabilities is key to addressing diverse operational environments. Additionally, providers emphasize enhancing cybersecurity and hybrid cloud solutions to build trust and meet stringent regulatory requirements, thereby ensuring secure, reliable service delivery and sustained competitive advantage.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Component trends

- 2.2.2 Aircraft type trends

- 2.2.3 Maintenance type trends

- 2.2.4 Deployment mode trends

- 2.2.5 Technology trends

- 2.2.6 End user trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising air traffic and fleet expansion

- 3.2.1.2 Growing adoption of IoT and advanced analytics in aviation

- 3.2.1.3 Regulatory push for real-time aircraft health monitoring

- 3.2.1.4 Increasing demand for next-generation aircraft

- 3.2.1.5 Infrastructure development and construction sector growth

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial implementation and integration costs

- 3.2.2.2 Data security and privacy concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for cloud-based predictive maintenance platforms

- 3.2.3.2 Rising investments in digital transformation by airlines and mros

- 3.2.3.3 Emerging markets driving commercial fleet growth

- 3.2.3.4 Application of predictive maintenance in military and defense aviation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Defense budget analysis

- 3.11 Global defense spending trends

- 3.12 Regional defense budget allocation

- 3.12.1 North America

- 3.12.2 Europe

- 3.12.3 Asia Pacific

- 3.12.4 Middle East and Africa

- 3.12.5 Latin America

- 3.13 Key defense modernization programs

- 3.14 Budget forecast (2025-2034)

- 3.14.1 Impact on industry growth

- 3.14.2 Defense budgets by country

- 3.15 Supply chain resilience

- 3.16 Geopolitical analysis

- 3.17 Workforce analysis

- 3.18 Digital transformation

- 3.19 Mergers, acquisitions, and strategic partnerships landscape

- 3.20 Risk assessment and management

- 3.21 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Component, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Edge devices

- 5.2.2 Data acquisition units (DAU)

- 5.2.3 Flight data recorders / health monitoring units

- 5.2.4 Communication modules

- 5.2.5 Others

- 5.3 Software

- 5.3.1 Predictive analytics software

- 5.3.2 Condition-based monitoring platforms

- 5.3.3 Machine learning & AI engines

- 5.3.4 Others

- 5.4 Services

- 5.4.1 System integration services

- 5.4.2 Data processing & model training services

- 5.4.3 Maintenance & technical support

- 5.4.4 Others

Chapter 6 Market Estimates and Forecast, By Aircraft Type, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Commercial aircraft

- 6.3 Military aircraft

- 6.4 Private aircraft

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Maintenance Type, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Airframe maintenance

- 7.3 Engine maintenance

- 7.4 Components maintenance

- 7.5 Ground equipment maintenance

Chapter 8 Market Estimates and Forecast, By Deployment Mode, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 On premise

- 8.3 Cloud

- 8.4 Hybrid

Chapter 9 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Billion)

- 9.1 Key trends

- 9.2 Condition-based maintenance (CBM)

- 9.3 Predictive maintenance tools

- 9.4 Machine learning algorithms

- 9.5 Internet of things (IoT)

- 9.6 Big data analytics

Chapter 10 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion)

- 10.1 Key trends

- 10.2 Commercial airlines

- 10.3 Military & defense organization

- 10.4 Aircraft OEMs

- 10.5 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 IMB

- 12.1.2 Lufthansa Technik

- 12.1.3 Boeing

- 12.1.4 Airbus

- 12.1.5 General Electric

- 12.2 Regional Key Players

- 12.2.1 North America

- 12.2.1.1 Delta TechOps

- 12.2.1.2 Honeywell

- 12.2.1.3 Microsoft

- 12.2.1.4 Pratt & Whitney

- 12.2.2 Europe

- 12.2.2.1 Air France KLM

- 12.2.2.2 Rolls-Royce

- 12.2.2.3 Safran

- 12.2.2.4 SAP

- 12.2.2.5 Thales

- 12.2.3 APAC

- 12.2.3.1 ST Engineering

- 12.2.3.2 GMF AeroAsia

- 12.2.1 North America

- 12.3 Niche Players / Disruptors

- 12.3.1 AeroSoft Systems

- 12.3.2 Aviation Intertec

- 12.3.3 CAMP Systems

- 12.3.4 Swiss Aviation Software