PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797808

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797808

Audit Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

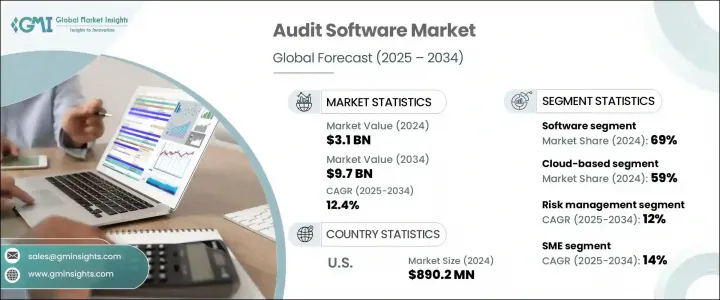

The Global Audit Software Market was valued at USD 3.1 billion in 2024 and is estimated to grow at a CAGR of 12.4% to reach USD 9.7 billion by 2034. With enterprises increasingly digitizing their operations, traditional audit processes are being replaced with modern, technology-driven solutions. The need for accurate, efficient, and scalable auditing practices is becoming more critical. Organizations are investing in audit software to automate workflows, minimize manual effort, and enhance productivity. The capability of such platforms to provide real-time collaboration, remote access, and centralized data storage significantly boosts auditing accuracy and speeds up procedures.

As digital operations become the norm, businesses are embracing audit tools not only to meet compliance standards but also to support strategic decision-making. The ongoing shift toward cloud-based infrastructures and remote work culture has only accelerated the demand for reliable audit solutions that ensure operational continuity without physical presence.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.1 Billion |

| Forecast Value | $9.7 Billion |

| CAGR | 12.4% |

In terms of deployment, cloud-based audit software has become the dominant choice among enterprises. In 2024, this segment accounted for 59% of the overall market share and is expected to grow at a CAGR of over 13% through 2034. This growth is largely attributed to the flexibility and accessibility that cloud platforms offer. Users can seamlessly access, edit, and share data from anywhere, allowing for faster decision-making and more agile audit execution. Cloud technology also reduces dependency on in-person audits and traditional office setups, enabling uninterrupted operations even during unexpected disruptions. The ability to ensure business continuity while reducing physical infrastructure costs makes cloud deployment highly attractive to modern businesses.

By organization size, large enterprises continue to lead the market due to their scale, complexity, and heightened regulatory responsibilities. Their need to standardize auditing practices across global teams, manage multiple regulatory environments, and handle vast volumes of data makes scalable and secure audit software a necessity. These organizations seek customizable platforms that support multilingual functions, diverse compliance frameworks, and large-scale training. With digital security and scalability as top priorities, large enterprises are actively adopting AI-powered and analytics-driven audit tools to optimize governance and ensure comprehensive risk management. In 2024, large enterprises accounted for the largest share of audit software adoption, and this trend is expected to continue as enterprises expand their digital capabilities and regulatory obligations.

On the basis of application, the internal audit segment holds the leading position and is expected to maintain dominance throughout the forecast period. With increased attention to corporate transparency, risk mitigation, and internal control frameworks, businesses are prioritizing tools that streamline internal auditing tasks. Audit software now plays a critical role in aligning audit functions with broader organizational goals. Advanced platforms offer in-depth insights that help internal teams identify potential risks, enhance governance, and ensure compliance with industry standards. This shift toward proactive auditing strategies supported by automation and AI integration continues to drive demand for internal audit solutions.

Regionally, the United States holds a significant position in the audit software landscape. In 2024, the country captured around 86% of the North American market, generating USD 890.2 million in revenue. This leadership is underpinned by the rapid adoption of emerging technologies by American firms, including artificial intelligence, machine learning, and advanced analytics. Businesses across the U.S. are leveraging digital auditing platforms to reduce errors, gain sharper insights, and improve the overall accuracy of audit and compliance operations. These tools also support smarter decision-making, better risk identification, and higher operational efficiency. With innovation at the forefront, the U.S. continues to set the pace for digital audit transformation in the global market.

Key companies actively shaping the audit software industry include AuditBoard, CaseWare International, Galvanize (Diligent), IBM, MetricStream, Oracle, SAP SE, Thomson Reuters, Wolters Kluwer, and Workiva. These players are focusing on offering cloud-enabled, AI-integrated solutions that meet evolving compliance and business intelligence demands. Their strategic investments in product development and partnerships further underscore the competitive nature of this fast-evolving market.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment mode

- 2.2.4 Organization size

- 2.2.5 Application

- 2.2.6 Industry vertical

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factors affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising regulatory compliance requirements

- 3.2.1.2 Growing focus on risk management and internal control

- 3.2.1.3 Increasing digital transformation in enterprises

- 3.2.1.4 Demand for real-time data and analytics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data security and privacy risks

- 3.2.2.2 Integration issues with legacy systems

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of AI and predictive analytics

- 3.2.3.2 Rising demands from SMEs and emerging markets

- 3.2.3.3 Expansion in ESG and sustainability reporting audits

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Case studies

- 3.12 Best case scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 On-premise

- 5.2.2 Cloud-based

- 5.3 Services

- 5.3.1 Implementation & integration

- 5.3.2 Consulting

- 5.3.3 Support & maintenance

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 On-premise

- 6.3 Cloud-based

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 SME

- 7.3 Large enterprises

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Internal audit

- 8.3 External audit

- 8.4 Compliance management

- 8.5 Risk management

- 8.6 Fraud detection

- 8.7 Financial auditing

- 8.8 Operational auditing

Chapter 9 Market Estimates & Forecast, By Industry Vertical, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 BFSI

- 9.3 Healthcare

- 9.4 Manufacturing

- 9.5 IT & telecom

- 9.6 Retail & e-commerce

- 9.7 Government & public sector

- 9.8 Energy & utilities

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 AuditBoard

- 11.1.2 SAP

- 11.1.3 Workiva

- 11.1.4 MetricStream

- 11.1.5 Thomson Reuters

- 11.1.6 Caseware International

- 11.2 Regional players

- 11.2.1 DataSnipper

- 11.2.2 NAVEX Global

- 11.2.3 Onspring

- 11.2.4 CURA Software

- 11.2.5 Insight Software

- 11.2.6 Hyperproof

- 11.3 Emerging players

- 11.3.1 Cerrix

- 11.3.2 Onapsis

- 11.3.3 Inflo Software

- 11.3.4 EasyAudit

- 11.3.5 AD Audit Plus

- 11.3.6 Audimex

- 11.3.7 Gensuite

- 11.3.8 Trintech

- 11.3.9 Wolters Kluwer

- 11.3.10 Workiva