PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797823

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797823

Residential Building Automation Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

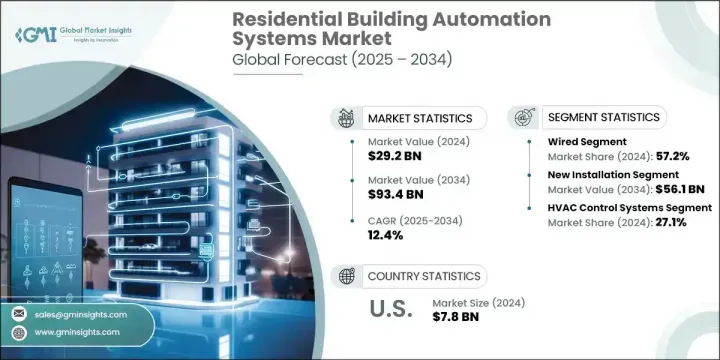

The Global Residential Building Automation Systems Market was valued at USD 29.2 billion in 2024 and is estimated to grow at a CAGR of 12.4% to reach USD 93.4 billion by 2034. This growth is being driven by rising demand for energy efficiency, the expansion of smart home devices, the rapid evolution of the Internet of Things, and stricter environmental and building regulations. Consumers are placing higher priority on intuitive, integrated systems that simplify the control of lighting, HVAC, and security within their homes. Advancements in IoT protocols and wireless connectivity have improved the reliability and compatibility of devices, accelerating adoption in both new construction and renovations.

There is also a growing trend in retrofit automation and sustainable solutions, particularly in developed economies where smart living is becoming the norm. With increasing awareness about energy conservation, developers and manufacturers are shifting their focus to sustainable, intelligent systems that support eco-friendly residential environments. Governments are pushing for green living through regulatory backing, further encouraging smart home adoption. These factors contribute to the accelerated momentum of this expanding market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $29.2 Billion |

| Forecast Value | $93.4 Billion |

| CAGR | 12.4% |

The wireless segment is forecasted to grow at a CAGR of 15.6% from 2025 to 2034, due to the increased use of IoT-enabled technologies and the convenience of installation without structural changes. As urbanization continues, there is growing interest in flexible, easily scalable systems suitable for apartments and compact residential layouts. Upgrades in secure, low-energy wireless communication protocols have made it easier to integrate air conditioning, lighting, and home security systems across diverse living environments, adding value to both small and large-scale smart home setups.

The new installation segment is projected to reach USD 56.1 billion by 2034, driven by the surge in demand for smart residential buildings equipped with fully integrated automation from the ground up. As smart technologies become part of standard home design, automation systems are increasingly being built into the construction process. Partnerships between automation providers and construction firms are essential to meet this demand, especially when turnkey solutions are designed to meet the specific needs of modern homes from the beginning of a project.

U.S. Residential Building Automation Systems Market was valued at USD 7.8 billion in 2024, supported by a high rate of smart technology adoption and growing consumer awareness about energy-efficient living. Many certified energy-efficient homes in the region reflect this momentum. Strong regulatory focus on sustainability and favorable policies continue to encourage the use of intelligent building systems. This makes the U.S. one of the most promising markets for companies to invest in developing solutions that prioritize interoperability, regulatory compliance, and reduced energy consumption. Collaborations with builders and compliance experts allow companies to fast-track integration and broaden their footprint in this competitive space.

Key Residential Building Automation Systems Market participants include Schneider Electric, ABB, Johnson Controls, Siemens AG, and Honeywell International. To strengthen their market presence, leading players in the residential building automation systems space are focusing on creating integrated ecosystems that combine HVAC, lighting, security, and energy management into unified platforms. Investments are being made in AI-powered automation and voice-enabled technologies to enhance user experience and adaptability. Strategic partnerships with property developers and builders enable early-stage integration in construction projects, while cloud connectivity and mobile applications ensure remote access and control. Companies are also expanding product lines tailored for both retrofitting and new builds, offering scalable solutions across housing types.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 -2034

- 2.2 Key market trends

- 2.2.1 System type trends

- 2.2.2 Communication technology trends

- 2.2.3 Automation level trends

- 2.2.4 Installation trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for energy efficiency

- 3.2.1.2 Rapid growth of smart home devices and IoT adoption

- 3.2.1.3 Government policies and green building codes

- 3.2.1.4 Advancements in AI and machine learning

- 3.2.1.5 Integration with voice assistants and AI platforms

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial installation cost and ROI concerns

- 3.2.2.2 Cybersecurity and privacy risks

- 3.2.3 Market opportunities

- 3.2.3.1 Retrofit market in existing residential buildings

- 3.2.3.2 Integration with renewable energy and storage

- 3.2.3.3 Rising demand for assisted living and aging-in-place solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By System Type, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Energy management systems (EMS)

- 5.3 Lighting control systems

- 5.4 HVAC control systems

- 5.5 Security & access control systems

- 5.6 Fire & safety systems

- 5.7 Smart appliances

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Communication Technology, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Wired

- 6.3 Wireless

- 6.3.1 ZigBee

- 6.3.2 Z-Wave

- 6.3.3 Wi-Fi

- 6.3.4 Bluetooth

- 6.3.5 Others

Chapter 7 Market Estimates and Forecast, By Automation Level, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Semi-automation system

- 7.3 Fully-automation system

Chapter 8 Market Estimates and Forecast, By Installation, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 New installation

- 8.3 Retrofit/upgrade

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Honeywell International Inc.

- 10.1.2 Siemens AG

- 10.1.3 Schneider Electric

- 10.1.4 Johnson Controls International Plc

- 10.1.5 ABB Ltd.

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 Carrier

- 10.2.1.2 Crestron Electronics, Inc.

- 10.2.1.3 Lutron Electronics Co., Inc

- 10.2.1.4 Trane Technologies

- 10.2.1.5 Rockwell Automation

- 10.2.1.6 Eaton Corporation

- 10.2.1.7 Cisco Systems, Inc.

- 10.2.1.8 Emerson Electric Co.

- 10.2.2 Europe

- 10.2.2.1 Legrand SA

- 10.2.2.2 Bosch Sicherheitssysteme GmbH

- 10.2.2.3 Beckhoff Automation

- 10.2.3 Asia Pacific

- 10.2.3.1 Mitsubishi Electric Corporation

- 10.2.3.2 Hitachi, Ltd.

- 10.2.3.3 Azbil Corporation

- 10.2.3.4 Hangzhou Hikvision Digital Technology Co., Ltd.

- 10.2.3.5 SAMSUNG

- 10.2.1 North America

- 10.3 Niche Players / Disruptors

- 10.3.1 Delta Controls Inc.

- 10.3.2 Distech Controls