PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1801861

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1801861

Edible Packaging for Frozen Foods Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

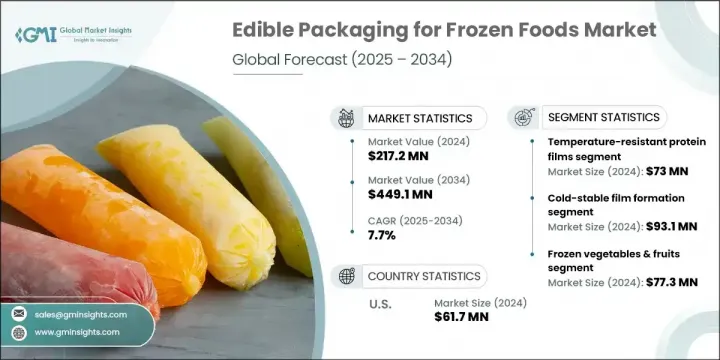

The Global Edible Packaging for Frozen Foods Market was valued at USD 217.2 million in 2024 and is estimated to grow at a CAGR of 7.7% to reach USD 449.1 million by 2034. This growing market is driven by an increasing demand for cold-stable, biodegradable packaging, particularly for individually quick frozen (IQF) fruits, vegetables, microwaveable frozen meals, and ready-to-heat meals. This demand is particularly evident in North America, Europe, and select parts of Asia-Pacific, such as Japan, South Korea, and Australia. The demand for edible packaging has been primarily fueled by the sales of frozen fruits and plant-based meals in North America and Europe, alongside more affordable alternatives like chitosan and starch-based packaging in parts of Asia-Pacific.

Polysaccharide films, due to their affordability and freeze stability, are expected to see the highest growth within the market. Additionally, the need for cold-chain optimization and the integration of flavors into edible coatings is expected to drive growth in premium product categories. The rise of private-label frozen foods in North America and Western Europe is another significant contributor to the increasing adoption of edible packaging.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $217.2 Million |

| Forecast Value | $449.1 Million |

| CAGR | 7.7% |

The polysaccharide films segment will reach 34.9% share by 2034. These films, derived from materials like starch, alginate, and cellulose, are preferred for their low cost, minimal allergen risk, and strong performance in frozen environments. They also offer flexibility, making them suitable for various frozen foods, such as vegetables, seafood, and ready-to-eat meals.

In 2024, the frozen vegetables and fruits segment accounted for 35.6% share driven by their high export volumes and early adoption of edible coatings, which help preserve moisture and enhance eco-friendly branding. The use of edible packaging has gained further momentum due to stricter organic labeling regulations and bans on plastic wraps for frozen produce in various regions, including Europe and parts of Asia.

North America Edible Packaging for Frozen Foods Market held 33% share in 2024, driven by retailer adoption, innovative start-ups in edible packaging, and growing consumer awareness of sustainability. The U.S. alone represented USD 61.7 million. Additionally, the rise of private-label frozen food products featuring edible films as a sustainable differentiation point has fueled further market growth. However, challenges such as the high cost of raw materials and regulatory compliance may slow the market's expansion.

Key players in the Global Edible Packaging for Frozen Foods Market include Ingredion Incorporated, Tate & Lyle PLC, BASF SE, WikiCell Designs Inc., and Amcor Plc. To maintain and expand their market position, companies in the edible packaging sector have employed a variety of strategies. These include ongoing innovation in materials to enhance product performance, such as increasing freeze stability and improving moisture retention for frozen foods. Companies have also focused on sustainability, ensuring their products are biodegradable and aligned with consumer demand for eco-friendly solutions. Strategic partnerships and collaborations with frozen food manufacturers have allowed companies to integrate their edible packaging into a broader range of products, especially in the growing plant-based and organic food sectors.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Technology

- 2.2.4 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain complexity

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2025 - 2034 (USD Million, Units)

- 5.1 Key trends

- 5.2 Temperature-resistant protein films

- 5.3 Polysaccharide films

- 5.4 Lipid-based coatings

- 5.5 Composite & hybrid materials

Chapter 6 Market Estimates and Forecast, By Technology Type, 2025 - 2034 (USD Million, Units)

- 6.1 Key trends

- 6.2 Cold-stable film formation

- 6.3 Barrier enhancements

- 6.4 Cold chain integration

Chapter 7 Market Estimates and Forecast, By Application type, 2025 - 2034 (USD Million, Units)

- 7.1 Key trends

- 7.2 Frozen vegetables & fruits

- 7.3 Frozen meat & seafood

- 7.4 Frozen ready meals

- 7.5 Frozen dairy & desserts

Chapter 8 Market Estimates and Forecast, By Region, 2025 - 2034 (USD Million, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 Tate & Lyle PLC

- 9.2 Kerry Group plc

- 9.3 Ingredion Incorporated

- 9.4 Cargill, Incorporated

- 9.5 Archer-Daniels-Midland Company

- 9.6 DuPont de Nemours, Inc.

- 9.7 BASF SE

- 9.8 Corbion N.V.

- 9.9 Roquette Freres

- 9.10 CP Kelco (J.M. Huber Corporation)

- 9.11 FMC Corporation

- 9.12 Ashland Global Holdings Inc.

- 9.13 Novamont S.p.A.

- 9.14 WikiCell Designs Inc.

- 9.15 MonoSol LLC