PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1801900

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1801900

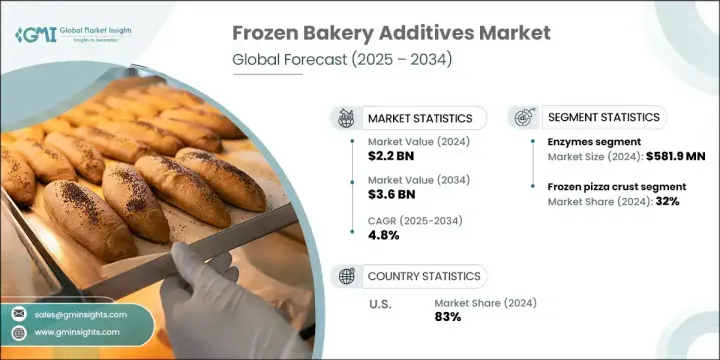

Frozen Bakery Additives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

The Global Frozen Bakery Additives Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 3.6 billion by 2034. The growing influence of urban lifestyles and the shift toward quick, ready-to-bake food solutions are major factors driving this market forward. As consumers continue to prioritize convenience without compromising on quality or flavor, frozen bakery products have become more prominent in both home kitchens and commercial foodservice sectors. These offerings provide the comfort of freshly baked goods with minimal preparation, aligning well with the fast-paced routines of modern consumers. The need for innovation, variety, and indulgence in baked goods has elevated demand for advanced additive solutions to maintain product appeal.

The increased interest in high-end, health-conscious, and specialty baked items has significantly fueled the frozen bakery additives segment. From gluten-free breads to gourmet pastries, these products require specific additives to maintain flavor, structure, and shelf stability. Additives are essential in delivering a uniform experience, ensuring the end product retains its desired texture and taste even after freezing and baking. Manufacturers are using these ingredients to address growing expectations for consistency and premium quality in every bite.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $3.6 Billion |

| CAGR | 4.8% |

In 2024, the enzymes were valued at USD 581.9 million due to their functional benefits in enhancing dough flexibility, improving product softness, and extending shelf life. Enzyme innovations tailored to specific baked goods are helping manufacturers achieve better consistency. However, the cost factor and sensitivity to processing conditions may limit their adoption in some applications.

The frozen pizza crusts segment held the largest share at 32% in 2024 and is set to grow at a CAGR of 4.8% through 2034. Additives used in this segment focus on achieving the ideal crust texture, flavor retention, and enhanced freshness. Developments that improve crispiness and storage performance are contributing to continued growth in this category.

U.S. Frozen Bakery Additives Market held 83% share and generated USD 720.5 million in 2024. The presence of a highly organized bakery sector, large-scale food production facilities, and an established logistics network supports strong additive adoption across the country. Manufacturers rely on advanced frozen bakery solutions to meet evolving consumer demands, and the availability of cutting-edge ingredients further accelerates market growth in the region.

Key companies in the Global Frozen Bakery Additives Market include Corbion, Tate Lyle PLC, Puratos, Archer Daniels Midland Company (ADM), Lesaffre, Palsgaard, Kerry Group, Novozymes, Cargill, DowDuPont, Ingredients, Lonza Group, and Ashland. Top players in the frozen bakery additives market are strengthening their global presence through strategic product development, mergers, and geographic expansion. Companies are investing in R&D to create additives that enhance shelf life, texture, and nutritional content without compromising on flavor or safety. Partnerships with large-scale bakery manufacturers allow these firms to integrate innovations directly into product pipelines. Customization and clean-label trends have also pushed companies to develop solutions with fewer artificial ingredients while maintaining performance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Impact forces

- 3.2.1 Growth driver

- 3.2.1.1 New product launches in the frozen bakery segment are expected to expand the industry.

- 3.2.1.2 Rising health awareness is boosting demand for gluten-free products.

- 3.2.1.3 Increasing disposable income is driving the demand for convenient food options.

- 3.2.2 Pitfalls/challenge

- 3.2.2.1 Strict food safety regulations can pose challenges.

- 3.2.2.2 High production costs may limit profitability.

- 3.2.2.3 Limited shelf life of some additives can affect quality.

- 3.2.3 Opportunities

- 3.2.3.1 Growing demand for convenience foods.

- 3.2.3.2 Rising popularity of gluten-free and health-focused products.

- 3.2.3.3 Expansion into emerging markets.

- 3.2.1 Growth driver

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key) countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Flavors & enhancers

- 5.2.1 Natural

- 5.2.2 Artificial

- 5.3 Oxidising agents

- 5.4 Colorants

- 5.4.1 Natural

- 5.4.2 Synthetic

- 5.5 Enzymes

- 5.6 Preservatives

- 5.7 Reducing agents

- 5.7.1 Ascorbic acid

- 5.7.2 L-cysteine

- 5.7.3 Sorbic acid

- 5.8 Leavening agents

- 5.8.1 Ascorbic acid

- 5.8.2 L-cysteine

- 5.9 Emulsifier

- 5.9.1 Mono, di-glycerides & derivatives

- 5.9.2 Lecithin

- 5.9.3 Stearoyl lactylates

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Frozen bread

- 6.3 Frozen biscuits & cookies

- 6.4 Frozen cake & pastry

- 6.5 Frozen pizza crust

- 6.6 Frozen dough

Chapter 7 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 MEA

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 Cargill, Inc.

- 8.2 Corbion

- 8.3 Kerry Group

- 8.4 Archer Daniels Midland Company (ADM)

- 8.5 Novozymes

- 8.6 DowDuPont

- 8.7 Palsgaard

- 8.8 Lonza Group

- 8.9 Lesaffre

- 8.10 Puratos

- 8.11 Ingredients

- 8.12 Ashland

- 8.13 Tate Lyle PLC