PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1801935

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1801935

Spinal Fusion Device Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

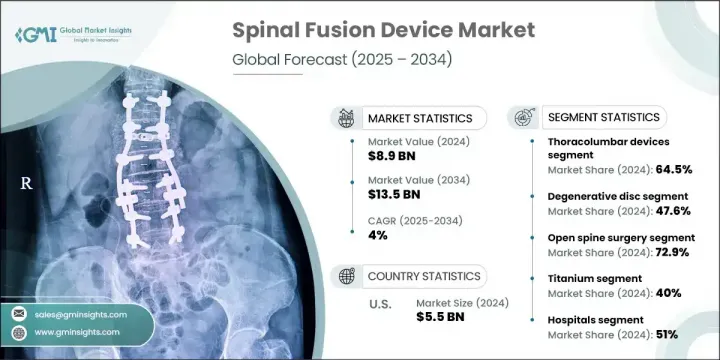

The Global Spinal Fusion Device Market was valued at USD 8.9 billion in 2024 and is estimated to grow at a CAGR of 4% to reach USD 13.5 billion by 2034. The market's upward momentum is fueled by the rising number of spinal disorders, a growing pool of target patients, and ongoing investments in R&D to develop more advanced and minimally invasive fusion procedures. Despite the positive outlook, limited reimbursement options in several emerging countries remain a challenge for full market scalability. Nevertheless, advancements in spinal surgery and the rise in aging populations worldwide continue to elevate demand. Technological evolution, particularly in intraoperative imaging, robotics, and navigation, is helping reduce surgical complications and improve outcomes.

The thoracolumbar devices segment held 64.5% share in 2024, owing to the high frequency of lumbar degenerative disorders and spinal injuries that necessitate surgical stabilization in both the thoracic and lumbar spine. Growth in this segment is largely driven by increasing rates of high-impact trauma and spine degeneration among older adults. Additionally, conditions like spinal fractures and spondylolisthesis are being addressed with precision-engineered devices to improve stability and recovery.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.9 Billion |

| Forecast Value | $13.5 Billion |

| CAGR | 4% |

In 2024, the degenerative disc disorder segment held a 47.6% share. This dominance is attributed to a surge in cases of age-related disc degeneration and the broader adoption of less invasive spinal fusion methods. As more elderly individuals experience disc-related issues, the need for efficient, lower-risk treatment continues to climb. Earlier detection, patient awareness, and growing trust in minimally invasive procedures also play vital roles in boosting the segment's performance.

US Spinal Fusion Device Market generated USD 5.5 billion in 2024. This growth stems from an increasing number of geriatric patients and a high burden of spinal disorders, along with broader acceptance of innovative surgical tools and techniques. The region benefits from a robust healthcare system, advanced surgical infrastructure, and favorable adoption of modern spinal implants and navigation systems. The market was valued at USD 4.2 billion in 2021 and USD 4.7 billion in 2022, showing steady annual increases fueled by clinical demand and technological improvements.

Top companies in the Global Spinal Fusion Device Market include Stryker, Globus Medical, Medtronic, NuVasive, and DePuy Synthes. To strengthen their market presence, leading spinal fusion device manufacturers are investing heavily in robotic-assisted surgery, AI-powered navigation systems, and minimally invasive product development. These firms are expanding their product portfolios through R&D and targeted acquisitions to offer end-to-end spinal solutions. Strategic partnerships with hospitals and surgical centers are also enabling quicker adoption of advanced devices. Several companies are localizing production and strengthening distribution networks to better serve high-growth markets. Continuous surgeon training programs and digital platform integration are further enhancing procedural precision and adoption rates across geographies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Disease type trends

- 2.2.3 Surgery trends

- 2.2.4 Material type trends

- 2.2.5 End use trends

- 2.2.6 Region trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of spinal diseases

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rise in number of trauma and injury cases

- 3.2.1.4 Rising geriatric population coupled with high demand for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory scenario

- 3.2.2.2 High cost of spinal procedures

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of ambulatory surgical centers (ASCs)

- 3.2.3.2 Increasing adoption of robotic and navigation-assisted surgery

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.1.1 Integration of navigation and robotic systems

- 3.5.1.2 Widespread use of PEEK and titanium cages

- 3.5.2 Emerging technologies

- 3.5.2.1 3D Printing, and advances in spinal implants

- 3.5.2.2 Smart implants with sensor integration

- 3.5.1 Current technological trends

- 3.6 Future market trends

- 3.7 Spinal Fusion Device Market, By Region, 2021 - 2034 (Units)

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.7.4 Latin America

- 3.7.5 Middle East and Africa

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Value chain analysis

- 3.12 Reimbursement scenario

- 3.13 Consumer behaviour analysis

- 3.14 Comparative analysis: anterior Vs posterior surgical approach

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 Latin America

- 4.3.6 MEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Thoracolumbar devices

- 5.2.1 Pedicle screws

- 5.2.2 Intervertebral body fusion device (IBFD)

- 5.2.3 Rods

- 5.2.4 Plates

- 5.2.5 Other thoracolumbar devices

- 5.3 Cervical fixation devices

- 5.3.1 Intervertebral body fusion device (IBFD)

- 5.3.2 Plates

- 5.3.3 Rods

- 5.3.4 Hooks

- 5.3.5 Other cervical devices

Chapter 6 Market Estimates and Forecast, By Disease Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Degenerative disc

- 6.3 Spinal deformity

- 6.4 Trauma and fractures

- 6.5 Spinal tumors

- 6.6 Other disease types

Chapter 7 Market Estimates and Forecast, By Surgery, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Open spine surgery

- 7.3 Minimally invasive spine surgery

Chapter 8 Market Estimates and Forecast, By Material Type, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Titanium

- 8.3 Polyether ether ketone (PEEK)

- 8.4 Cobalt chrome

- 8.5 Stainless steel

- 8.6 Other materials

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Ambulatory surgical centers

- 9.4 Orthopedic clinics

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ATEC

- 11.2 B. Braun

- 11.3 Captiva Spine

- 11.4 ChoiceSpine

- 11.5 DePuy Synthes

- 11.6 Globus Medical

- 11.7 K2M

- 11.8 Life Spine

- 11.9 Medtronic

- 11.10 NuVasive

- 11.11 Orthofix

- 11.12 Premia Spine

- 11.13 Stryker

- 11.14 Xtant Medical

- 11.15 Zimmer Biomet